Port, Blend or Break? Choosing the Cheapest Way to Move Your Mortgage in 2025

Why This Decision Matters More in 2025

Roughly 1.2 million Canadian households are renewing this year, and many are also upsizing, downsizing, or relocating for work. The Bank of Canada is holding its policy rate at 2.75 per cent for now, but five-year fixed rates remain in the 4.9 – 5.4 per cent band—well above the sub-3 per cent deals many borrowers locked in before the 2022 tightening cycle. Bank of Canada

That gap creates a tough question when you move: should you carry your existing low-rate mortgage with you (“port”), blend it with new money at today’s rates, or pay the penalty to break it and start fresh? The cheapest path isn’t obvious, because each option carries its own fees, timelines, and long-term interest costs. This guide breaks down all three strategies so you can make an evidence-based choice.

1. What Does “Porting” a Mortgage Mean?

Porting a mortgage lets you transfer both the balance and the interest rate/term of your existing loan to a new property. Most Canadian lenders allow it, but the rules vary:

| Factor | Typical requirement |

|---|---|

| Timing window | 30–120 days from sale close to purchase close |

| Maximum extra funds | 0 – 25 % “top-up” without requalifying |

| Appraisal needed? | Yes, on the new home |

| Credit re-check? | Often, especially if borrowing more |

Pros

-

Avoids pre-payment penalties that can hit $10–30 k on large balances.

-

Keeps your low coupon rate for the remainder of the term.

-

Simplifies budgeting—no new amortization schedule to learn.

Cons

-

Rate holds are short. If your purchase closes after the portability window, you lose the privilege.

-

If you need extra money to buy a pricier home, that top-up portion is advanced at today’s market rates.

-

Not all lenders permit portability between provinces, new-builds, or modular homes.

Reality check: Some lenders market “portable” mortgages but require you to complete both transactions on the same day—an impossible hurdle for most buyers. Always confirm the exact timeline in writing. Winnipeg Regional Real Estate News

2. Blend-and-Extend (a.k.a. “Blend and Extend Canada”)

A blended mortgage merges your current balance/rate with new money at today’s rate. There are two flavours:

-

Blend-to-term – new weighted-average rate, but the original maturity date stays the same.

-

Blend-and-extend – lender tacks on extra years, giving you a full new five-year term at the blended rate.

How the math works

If you owe $500,000 at 3.00 % (three years left) and need $100,000 more at 5.10 %, the weighted rate is roughly:

Your real payment may be slightly higher because lenders often add a premium (e.g., +0.10 %) for the convenience. NerdWallet

Pros

-

No penalty because you aren’t breaking the contract.

-

Easier qualifying—often no full re-underwrite if the total loan-to-value (LTV) stays under 80 %.

-

Extending the term can lower the payment shock in a higher-rate environment.

Cons

-

You’re usually locked to the same lender until the blended term expires.

-

The added premium means the math isn’t always cheaper than paying the penalty and switching to a new lender.

-

If rates fall sharply next year, you’re stuck unless you pay a hefty IRD to break again.

3. Breaking Your Mortgage Early

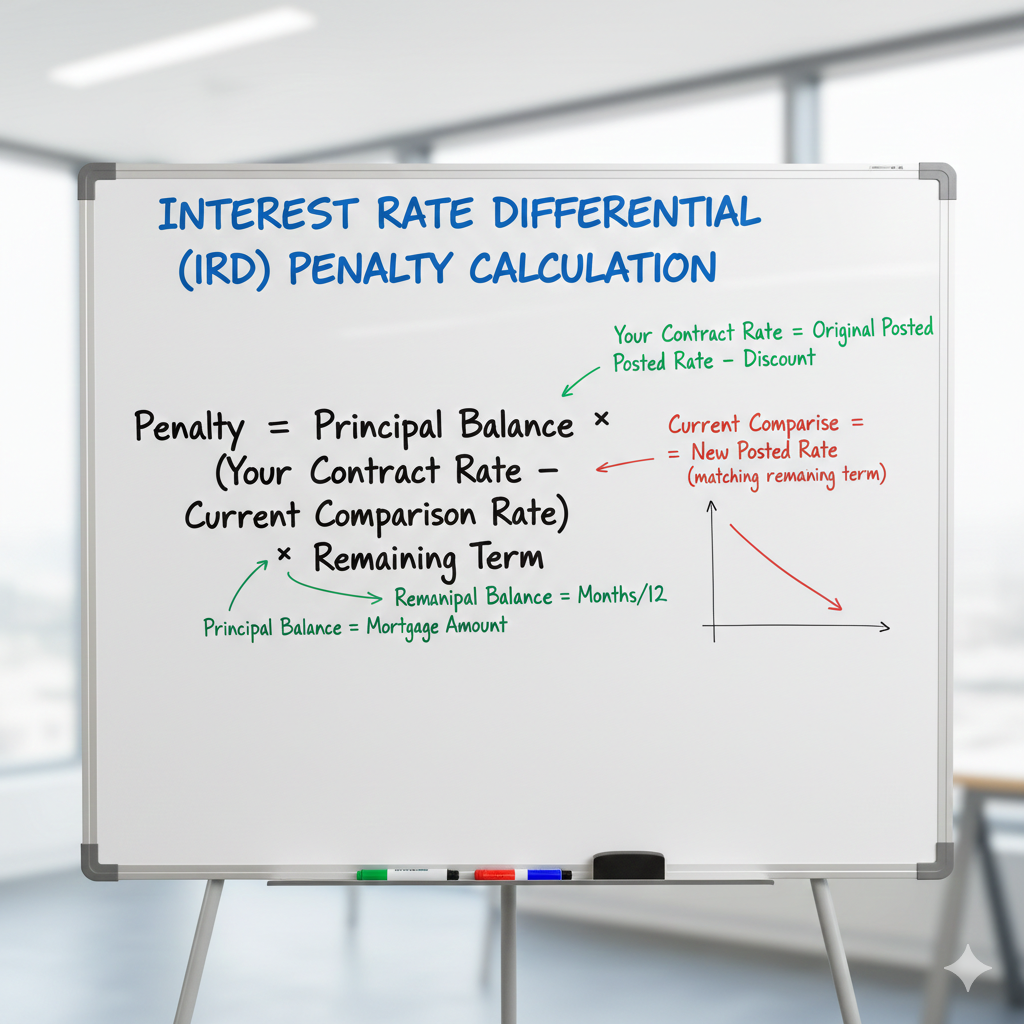

The third path is to pay the pre-payment penalty, discharge the loan, and start fresh with a new lender (or even your current lender at a new rate). Penalties fall into two camps:

| Lender type | Penalty formula |

|---|---|

| Variable-rate | 3 months’ interest (≈0.5 % of balance) |

| Big-Six fixed-rate | Greater of 3 months’ interest or the Interest Rate Differential (IRD) |

For a fixed-rate borrower with $500,000 outstanding at 2.89 % and 36 months left, the IRD could exceed $18,000 if posted rates have fallen since origination. Conversely, if rates rose—or you hold a variable—the cost might be closer to $6,000.

Pros

-

Full rate reset lets you shop the entire market for features like 30-year amortizations or flexible pre-payment privileges.

-

Potential to refinance above your current balance and consolidate high-interest debts at the same time.

-

Freedom to switch to a shorter term or variable if you expect rate cuts later in 2025. The Wall Street Journal

Cons

-

The penalty is real money out of pocket (or rolled into the new mortgage, extending amortization).

-

A new stress-test at BoC rate + 2 % applies; if your income hasn’t kept pace with the qualifying rate, approval may be tighter than it was five years ago.

-

You restart the amortization clock if you opt for a new 25- or 30-year schedule—adding long-term interest costs.

4. Case Study: Sarah & Alex Move from Ottawa to Kingston

| Detail | Current | New Purchase |

|---|---|---|

| Balance | $500,000 @ 3.00 % (36 mos left) | Add $100,000 |

| New rate (market) | – | 5.10 % (5-yr fixed) |

| Top-up funds needed | – | $100,000 |

| Closing gap between sale & purchase | 45 days |

Option A – Port

No penalty. They port $500k at 3 %, borrow an extra $100k at 5.10 % for the same 36 months.

Effective blended rate = 3.35 %.

Cost: $0 penalty + $700 appraisal/legal.

Option B – Blend-and-Extend

Lender offers new 5-yr term at 3.45 % (blended + 0.10 %).

Cost: $0 penalty + $400 admin fee.

Payment drop from 36 mo remaining to new 60 mo amortized term partially offsets higher rate.

Option C – Break & Re-finance

Penalty: $18,200 IRD. New 5-yr fixed at 4.85 %.

Cost: $18,200 penalty + $1,200 legal/appraisal, but no rate premium and full 5-yr term.

Net-present-value snapshot (simplified)

| Choice | 5-yr total interest + fees | Cash flow flexibility |

|---|---|---|

| Port | $86,900 | Rigid—term ends in 3 yrs |

| Blend | $91,300 | Medium—term resets to 5 yrs |

| Break | $94,500 | High—new features, longer amortization |

5. Decision Checklist for 2025 Movers

-

Confirm your lender’s porting window (30, 60, 90 days?) and whether bridge financing is available.

-

Request a written penalty quote valid for at least ten business days.

-

Calculate the true blended rate—include any lender “administration premium”.

-

Stress-test your affordability under the greater of 5.25 % or BoC 5-yr posted + 2 %.

-

Match the term to your outlook:

-

Expect rates to drop? Favour shorter terms after breaking.

-

Expect rates to rise or plateau? Port or blend to lock sub-3 % coupon for as long as possible.

-

-

Factor in life plans—future moves, renovations, or job changes can trigger another penalty.

6. Tax & Regulatory Nuances

-

Ported or blended mortgages keep their original CMHC insurance certificate if the LTV stays below 90 %. That can save thousands on insurance premiums compared with breaking and taking a brand-new insured loan.

-

Under OSFI’s Guideline B-20, lenders must re-qualify borrowers when new funds are advanced (top-up or blend), but some credit unions outside federal regulation may offer more flexibility.

-

The Home Buyers’ Plan (HBP) and FHSA don’t impact portability decisions directly, but if you’re moving to a first home as common-law partners, be mindful of withdrawal timing.

7. FAQs

Q. Can I port from a fixed to a variable rate?

A. Rarely. Most lenders require you to maintain the same interest-rate type until maturity.

Q. What if my new home is cheaper?

A. You can port and decrease the balance, but some lenders charge a partial IRD on the amount you pay down.

Q. Do credit unions offer better blending terms?

A. Often yes—fewer “blend premiums” and longer portability windows—yet their penalties on fixed rates can still rival the banks’.

8. The Bottom Line

In 2025’s mixed-rate landscape, there is no one-size-fits-all answer. The cheapest choice depends on:

-

Rate gap between your existing coupon and new-money rates.

-

Penalty size relative to potential interest savings.

-

Timeline between selling and buying.

-

Lifestyle plans for the next five years.

Start with the least disruptive option—porting—and only move up the cost ladder if the numbers (or your future plans) demand it. A licensed mortgage broker can model each scenario in detail, including tax-deductible interest if you’re turning your old property into a rental.

Ready to run the numbers?

The LendToday.ca team offers complimentary port-vs-break calculators and personalized advice for Canadian movers. Book a 15-minute call and learn which strategy will save you the most in 2025 and beyond.

Disclaimer: Information is for educational purposes and subject to change. Always review your mortgage contract and consult a qualified professional before making decisions.

- Can a Mortgage Company Evict You in Ontario? (2026 Power of Sale Guide) - February 23, 2026

- Crucial Ways to Survive the Redemption Period During Foreclosure: A Guide - February 21, 2026

- Painful Realities of the Interest Rate Differential Penalty You Must Know - February 15, 2026