The Hidden Risk: How Falling Home Values Can Jeopardize Your Refinance Plans

As a Canadian homeowner, refinancing your mortgage can be a powerful tool to reduce monthly payments, access equity for renovations, or consolidate high-interest debt. But what happens when home values begin to drop? A declining property market can drastically affect your ability to refinance—even if you have good credit and a steady income.

In this blog, we’ll explore how falling home prices impact your refinancing options, what factors lenders consider when evaluating refinance applications, and what you can do if your home’s value has taken a hit.

Understanding Refinancing: The Basics

Refinancing a mortgage means replacing your existing home loan with a new one, typically with different terms. Homeowners in Canada refinance for several reasons, such as:

-

Securing a lower interest rate

-

Accessing equity for major expenses

-

Consolidating debt into one manageable payment

-

Switching from a variable to a fixed-rate mortgage

But refinancing isn’t guaranteed. Your home must meet certain valuation and equity requirements to qualify.

Why Home Value Matters When Refinancing

Your home’s current market value plays a major role in a lender’s decision to approve your refinance application. The loan-to-value ratio (LTV)—which compares your mortgage balance to your home’s appraised value—is a key metric used by lenders.

For example:

If your home is valued at $500,000 and your mortgage balance is $400,000, your LTV is 80%. That’s generally acceptable to many Canadian lenders. But if your home’s value falls to $450,000, your LTV jumps to 88.8%, which may exceed the lender’s maximum threshold.

Most traditional lenders in Canada prefer an LTV of 80% or lower to approve a refinance without requiring mortgage default insurance or other risk mitigations.

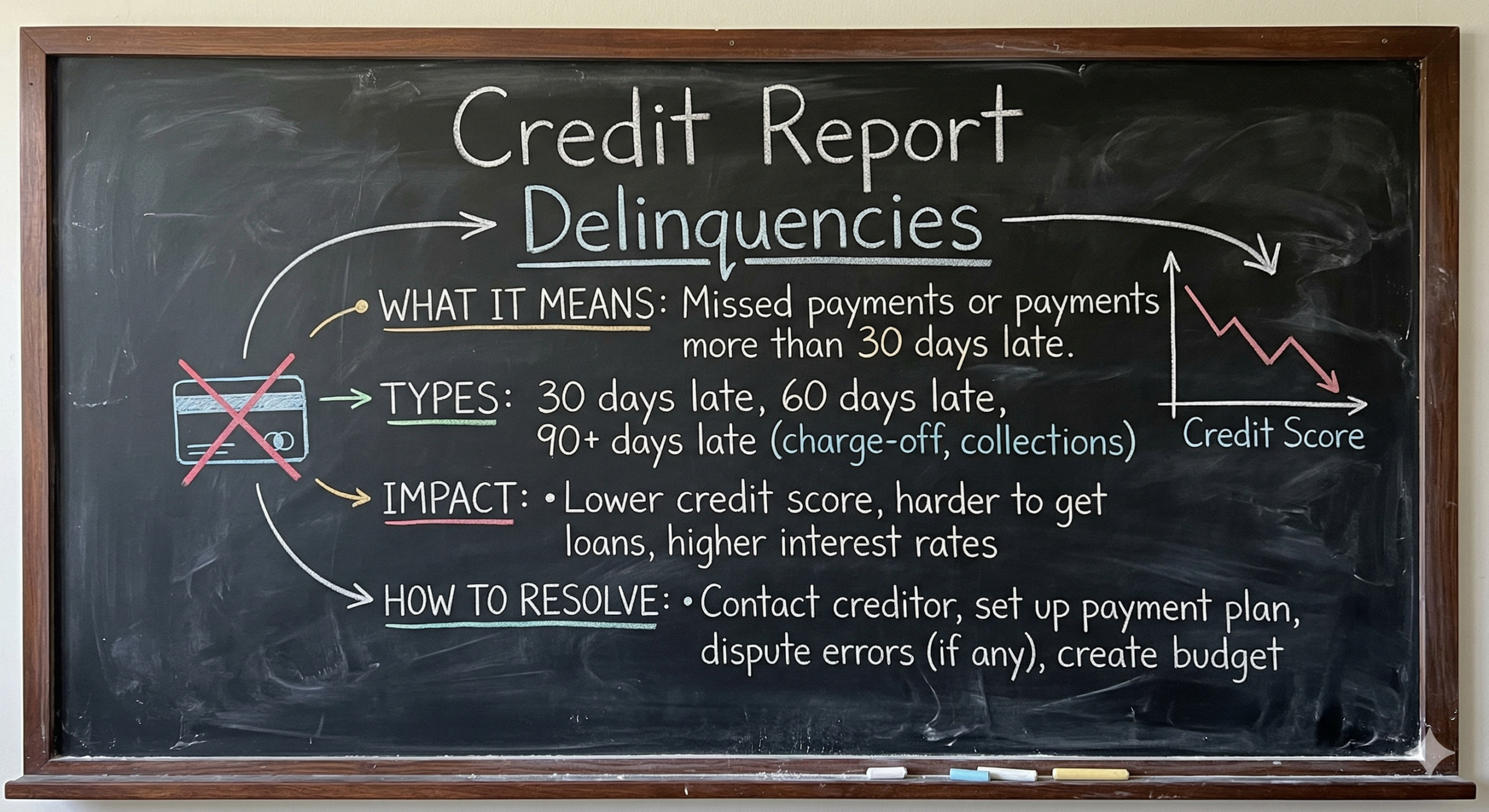

How Decreasing Home Values Create Refinancing Challenges

1. Reduced Home Equity

Your equity is the difference between your home’s value and what you owe. When home values fall, your equity shrinks—even if you’ve been making regular payments.

A homeowner who once had $150,000 in equity may now only have $100,000 or less, depending on how much the property value declined. Less equity means fewer options for cash-out refinancing or debt consolidation.

2. Higher LTV Ratios

As mentioned earlier, a lower home value increases your loan-to-value ratio. Most lenders in Canada have LTV maximums, and exceeding them means:

-

You may be denied a refinance outright

-

You could be forced to pay for mortgage default insurance

-

You might need to bring in extra funds to reduce the balance

3. Increased Risk Perception by Lenders

A declining housing market creates uncertainty for banks and mortgage lenders. Even if your finances are strong, lenders may tighten their criteria to protect themselves from potential losses. This often means:

-

Stricter appraisal reviews

-

Lower maximum LTV allowances

-

Reduced cash-out refinance availability

What Happens If You Can’t Refinance?

If your refinance application is denied due to a drop in home value, you may feel stuck—especially if you’re trying to lower monthly payments or avoid foreclosure.

Here are some consequences:

-

Continued High-Interest Payments: If your current mortgage has a high rate, being unable to refinance means you’ll keep paying more than necessary.

-

Missed Debt Consolidation Opportunity: Without access to home equity, consolidating high-interest credit cards or loans becomes difficult.

-

Limited Access to Emergency Funds: Many homeowners refinance to fund medical expenses, education, or home repairs. A denied application could halt those plans.

Canadian Housing Market: Why Home Values Are Falling

The Canadian real estate market has seen significant shifts in recent years. Rising interest rates, changing buyer demand, and economic uncertainty have led to home price corrections in several cities. Areas that once experienced record growth are now seeing flat or declining property values.

This trend affects urban centers like Toronto and Vancouver as well as smaller communities where affordability and employment conditions are under pressure.

What You Can Do if Your Home Value Has Dropped

If your home’s value has declined and refinancing seems out of reach, you still have options:

1. Work with a Mortgage Broker

Independent mortgage brokers have access to a wider range of lenders—including alternative and B-lenders—who may be more flexible with LTV requirements and declining home values. They can help you structure a refinance that suits your financial situation, even if your home has lost value.

2. Request a Professional Appraisal

Sometimes real estate platforms or automated valuation tools understate your home’s value. A certified appraiser may provide a more accurate—and potentially higher—valuation, improving your refinance prospects.

3. Wait and Rebuild Equity

If refinancing isn’t urgent, consider waiting until you’ve paid down more of your mortgage or the housing market rebounds. During this time, avoid taking on additional debt and focus on improving your credit profile to enhance your approval odds later.

4. Explore Second Mortgage or Home Equity Loans

If a full refinance isn’t possible, a second mortgage or home equity loan from a private lender might be an option. These tools allow you to tap into some of your equity without replacing your primary mortgage.

Strategies to Protect Against Home Value Drops

-

Avoid Overleveraging: Borrowing too close to your home’s market value puts you at risk in a declining market. Keep LTVs under control to leave room for flexibility.

-

Diversify Debt Solutions: Don’t rely solely on home equity for debt consolidation. Look at personal loans or budgeting strategies if equity is at risk.

-

Stay Informed About Market Trends: Watch real estate trends in your area. Understanding local market movements can help you time refinancing decisions more effectively.

Final Thoughts: Be Proactive, Not Reactive

Falling home values can seriously impact your ability to refinance in Canada. But with the right approach—whether that’s working with a mortgage broker, seeking a proper appraisal, or exploring alternative lending—you can navigate this challenge effectively.

The key is acting early. Don’t wait until your mortgage is up for renewal or your finances are stretched thin. If you suspect your home’s value has dropped, evaluate your refinance options now. Being proactive gives you more control over your financial future.

Need help navigating a declining housing market?

At LendToday.ca, we specialize in helping Canadian homeowners find solutions—even when the market isn’t on your side. Whether you need a second mortgage, debt consolidation, or creative refinancing options, we’re here to guide you.

Get your free home equity assessment today.

No obligation. Just expert advice tailored to your situation.