Feeling anxious about your mortgage is completely understandable, especially when bills are rising and income feels tight. If you’re worried you can’t pay your mortgage in Canada, this guide walks you through what typically happens, your rights, and the practical options available to you. We’ll explain the stages from a missed payment to mortgage arrears, and how processes like power of sale (common in Ontario) or foreclosure work in plain language. Most importantly, you’ll find calm, step-by-step ways to create breathing room—whether that’s talking to your lender, exploring a short deferral, considering a refinance, or planning a thoughtful next move. You’re not alone, and there are supportive paths forward.

Quick Actions That Help

-

Call your lender immediately. Early contact often unlocks short-term relief options.

-

Know the stages: missed payment, then arrears, then demand letter, then a legal remedy (usually power of sale in many provinces; foreclosure in a few).

-

Stop the bleed: slash discretionary spending, create a cash triage, and explore refinance/second-mortgage or payment deferrals.

-

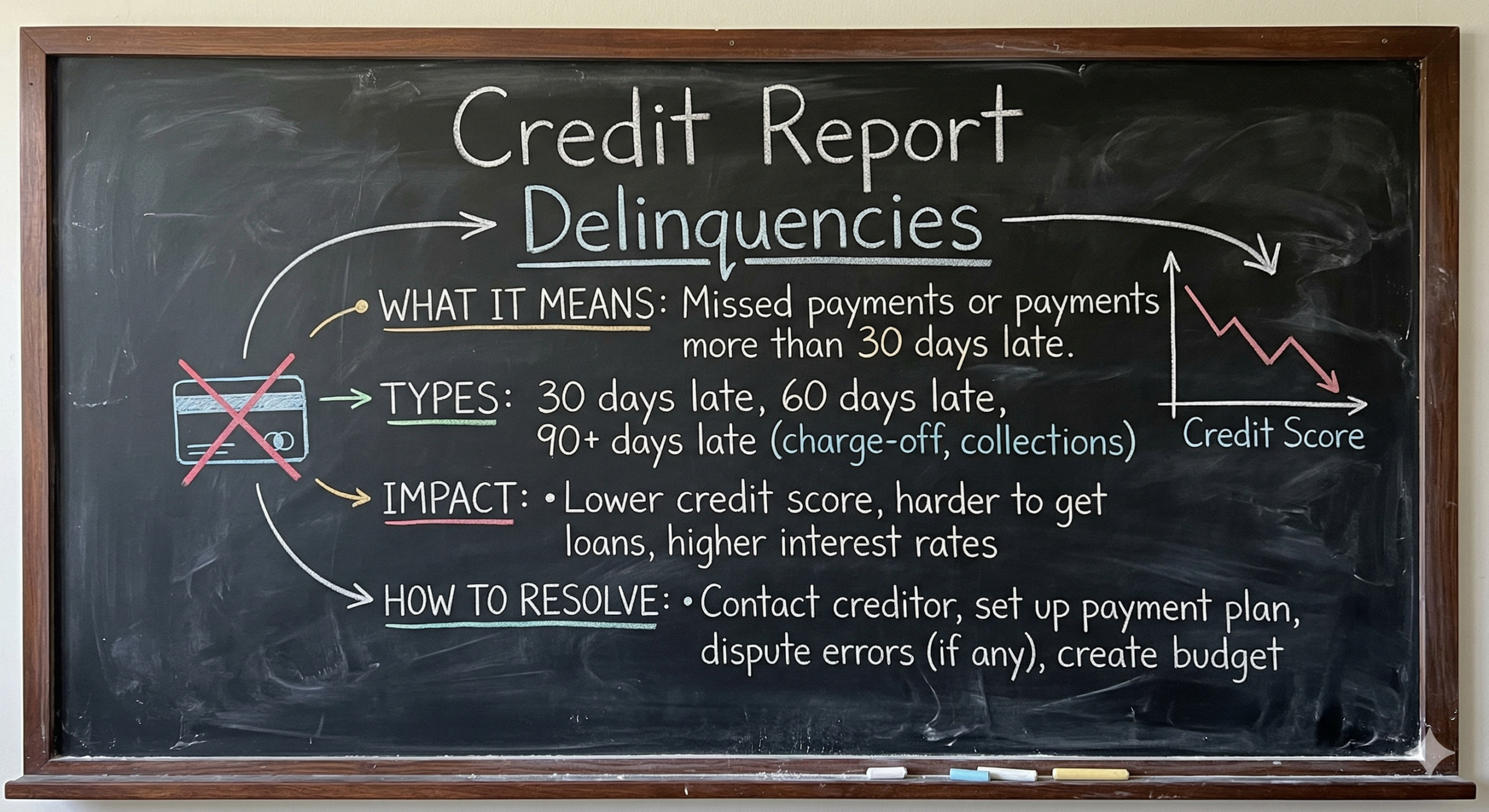

Protect your credit: one late mark can linger; act before 30+ days past due.

-

Get advice: a licensed mortgage broker can compare A/B/private options quickly.

Why Missed Payments Escalate Quickly

Canadian mortgages are backed by binding contracts. When you miss a payment:

-

Late/NSF fees may be added, and interest continues to accrue.

-

Credit impact: 30-day-plus arrears can be reported to bureaus, lowering your score and raising future borrowing costs.

-

Arrears status: after multiple missed payments, you’ll be formally “in arrears.”

-

Demand letter: the lender can require full repayment (including arrears, penalties, and legal fees).

-

Legal remedies: depending on the province and mortgage terms, lenders may pursue a power of sale (more common in Ontario) or foreclosure (title transfer process used in some other provinces).

Important: Timelines and remedies vary by province, lender, and your mortgage contract. Move early—your options narrow as fees and legal steps accumulate.

What Actually Happens – Stage by Stage

Stage 1: First Missed Payment (Days 1–30)

-

What you’ll see: late fee/NSF, collection outreach from lender/servicer.

-

Your moves:

-

Call the lender the same week, ask about a one-time skip, short deferral, or arrears repayment plan.

-

Build a two-week cash map (income vs. essentials). Pause non-essentials immediately.

-

If variable with adjustable payments and rates have risen, ask about a term reset or switching to interest-only temporarily (if available).

-

Stage 2: Multiple Missed Payments (30–60+ Days)

-

What you’ll see: account in arrears, stronger collections language, and potential credit bureau reporting.

-

Your moves:

-

Request a formal repayment plan to spread arrears.

-

Explore refinance (blend-and-extend, switch to a new lender) if equity and income support it.

-

If scores/income are tight, review B-lender or private short-term solutions to clear arrears, then plan a return to an A-lender in 6–18 months.

-

Stage 3: Demand Letter / Statement of Claim

-

What you’ll see: a legal notice requiring full repayment and outlining next steps (fees mount).

-

Your moves:

-

Ask about reinstatement (pay arrears, costs, and resume the mortgage) or redemption (pay off in full via refinance or sale).

-

Engage a mortgage broker to source fast funding; get a realistic budget and an exit plan back to lower rates.

-

Consider selling on your own terms to protect equity if the math no longer works.

-

Stage 4: Power of Sale / Foreclosure

-

What you’ll see: lender initiates a remedy to recover funds; in power of sale, the property is sold to repay the loan and costs; in foreclosure, title may transfer to the lender (varies by province).

-

Your moves:

-

Move quickly on any remaining reinstatement/redemption options.

-

Obtain independent legal advice on timelines, rights, and potential deficiency balances.

-

If a sale is inevitable, coordinate cooperatively to preserve equity and minimize damage.

-

9 Proven Ways to Stabilize Your Mortgage Situation

-

Call the lender first. Demonstrate a plan and ask for a temporary deferral, payment reduction, or arrears plan.

-

Refinance to consolidate high-interest debt. Replacing 20%+ credit card rates with mortgage-level rates can free cash flow.

-

Short-term private or B-lender bridge. Clear arrears now, fix credit, and plan a return to an A-lender in 6–18 months.

-

Extend amortization. A longer amortization lowers the monthly payment (watch total interest paid).

-

Switch term/type. Fixed can add payment certainty; variable with adjustable payments can ease the payment shock in certain cases—ask about interest-only periods if offered.

-

Rent a room/suite. Documented rental income can help debt-service ratios and cash flow.

-

Sell non-essential assets. Vehicles, recreational items, or investments that aren’t core can buy time.

-

Consumer proposal (last-resort for unsecured debt). May reduce unsecured payments; get advice first due to credit and mortgage qualification impacts.

-

Strategic sale. If carrying costs exceed realistic income, selling early may preserve the most equity.

Cash-Flow Triage: A Simple Priority Order

-

Mortgage/property taxes/insurance

-

Utilities and essential transportation

-

Groceries and medical

-

Minimums on other credit

-

Everything else (pause or cancel)

Option Snapshot (At-a-Glance)

| Option | Best For | Pros | Cons | Typical Goal |

|---|---|---|---|---|

| Lender deferral/repayment plan | Short-term hiccup | Fast, low cost | Temporary approval needed | Bridge a gap |

| Refinance with A-lender | Good credit/income, equity | Lowest rates, consolidate debt | Qualification rules | Long-term fix |

| B-lender / Private | Bruised credit, urgent arrears | Speed, flexible | Higher rates/fees | 6–18-mo bridge |

| Extend amortization | Need lower payment now | Immediate relief | More interest over time | Cash-flow stability |

| Sell proactively | Negative cash flow, low runway | Preserve equity | Must relocate | Reset finances |

How This Affects Your Credit (and How to Limit Damage)

-

30-day late can dent your score; 60–90-day lates and collections hit harder.

-

Limit new late marks: set up auto-pay, even if for interest-only, while you negotiate a plan.

-

Dispute errors with bureaus and ask lenders to report the account as current once arrears are cleared (not guaranteed, but worth asking).

-

Rebuild strategy: keep utilization <30% on revolving credit, avoid multiple new inquiries, and make a 12-month clean payment streak your mission.

Taxes, Insurance & Condo Fees – Don’t Miss These

Falling behind on property taxes, home insurance, or condo fees can trigger separate legal issues or force-placed insurance often more expensive. If cash is tight, contact each party early to discuss a plan.

Power of Sale vs. Foreclosure (Plain-English Overview)

-

Power of Sale (common in Ontario and some other provinces): The lender sells the property to recover what’s owed and expenses. Any surplus after costs may return to you; if there’s a shortfall, you could still owe the deficiency.

-

Foreclosure (used in some provinces): The lender seeks title to the property; deficiency rules differ.

-

Takeaway: Act before legal steps harden. Reinstating or refinancing early usually protects the most equity and credit.

This guide offers general education, not legal advice. Get independent legal advice for your province and contract.

FAQs

1) Will one missed payment ruin my credit?

Not necessarily, but a 30-day-late payment can lower your score. Call the lender immediately to try and resolve before the 30-day mark.

2) Can my lender offer a deferral?

Sometimes. Options depend on your lender, product, insurer (if any), and payment history. Early contact improves your chances.

3) Is a second mortgage a bad idea?

It’s a tool—not inherently good or bad. Used properly, it can clear arrears and high-interest debt, buying time to reset and return to an A-lender.

4) Should I pick fixed or variable if I’m struggling?

If payment certainty is key, fixed may help budgeting. If you expect income relief soon and can handle payment changes, a variable could work. Ask a broker to model scenarios.

5) Will a consumer proposal help with my mortgage?

It targets unsecured debt. It can free cash flow, but it may complicate new mortgage approvals. Get advice before filing.

6) Can I stop a power of sale/foreclosure once it starts?

Sometimes, via reinstatement or redemption, refinancing, or selling, timelines are critical. Get legal and broker support immediately.

7) Should I sell now or wait?

If negative cash flow is unsustainable and arrears are mounting, selling early typically protects the most equity and reduces stress.

Action Plan You Can Start Today

-

Make the call to your lender and ask about a written arrears plan or short deferral.

-

Audit cash flow and cut 3–5 line items today.

-

Get a mortgage options report (A/B/private) from a broker with a 6–18-month exit plan back to prime rates.

-

List debts and rates; target anything >12% for payoff via refinance if feasible.

-

Set calendar reminders for payment dates and follow-ups; enable auto-pay if possible.

-

If needed, prep for sale

Struggling with payments? The LendToday team can map out fast arrears solutions (A-lender, B-lender, or private) and craft a clear exit back to low-cost financing. Reach out for a confidential assessment.