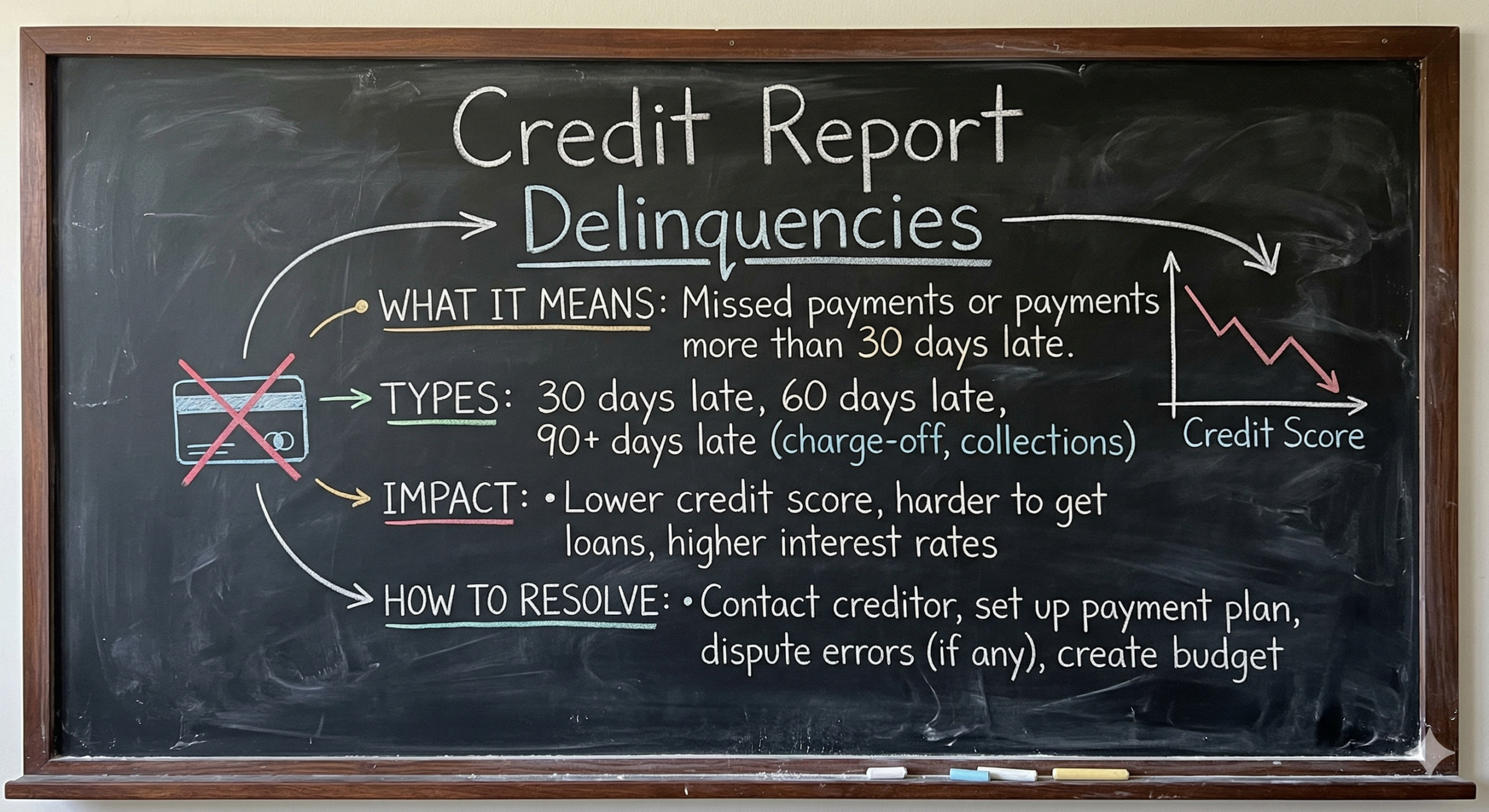

1) What These Options Actually Mean (Plain-English Overview)

Debt consolidation means rolling multiple high-interest debts (credit cards, lines of credit, personal loans) into one new loan with a lower interest rate and a single monthly payment. If you own a home, consolidation often involves a home equity loan, HELOC, or second mortgage to pay off higher-interest balances. If you don’t own a home, you might consolidate through a bank, credit union, or alternative lender—approval hinges on income, credit, and debt-to-income ratios.

A consumer proposal is a formal, legally binding settlement under the Bankruptcy and Insolvency Act, negotiated by a Licensed Insolvency Trustee (LIT). You repay only a portion of what you owe (often over up to 5 years) and, once completed, remaining eligible unsecured debt is forgiven. Collection calls stop, wage garnishments can be halted, and interest on included debts typically stops—but there’s a significant impact on your credit during and after the proposal.

Key difference: Consolidation restructures debt through a new loan you must qualify for; a consumer proposal reduces debt through a legal settlement, without traditional credit approval.

2) The 7 Helpful Facts You Must Know

1: If you still qualify for a decent rate, consolidation preserves more future borrowing power.

A consolidation loan (especially one secured by home equity) can protect your access to mainstream credit products later. A consumer proposal, by contrast, places a heavy derogatory mark on your credit file during the term and for a period after completion.

2: A consumer proposal can slash what you owe—sometimes by 30%–70%—but the trade-off is credit impact.

Proposals dramatically reduce principal and freeze interest on included unsecured debts. It’s powerful relief—but lenders will view your profile as higher risk for years.

3: Home equity changes everything.

Ontario homeowners with sufficient equity can often consolidate at a lower cost of borrowing than they’re currently paying on credit cards, even if their credit took a hit. This route can be faster and simpler than a proposal and may save more over time, depending on rates and fees.

4: Renters with limited income or damaged credit often find proposals more attainable.

If you can’t qualify for consolidation (no collateral, insufficient income, major delinquencies), a proposal may be the most realistic way to eliminate debt pressure and stop collections.

5: Monthly cash-flow relief can come from both options—just in different ways.

Consolidation lowers interest and re-amortizes your debt for a smaller payment; a proposal reduces principal and spreads it over up to five years. Both can shrink your monthly outflow—what differs is the credit consequences and total cost over time.

6: Timing matters if a mortgage renewal is coming up.

Entering a consumer proposal before renewing can limit your lender choices and affect rates/terms. A well-structured consolidation before renewal can tidy up your profile and position you for better renewal outcomes.

7: The right choice is the one you can complete comfortably—without backsliding.

Whether you choose consolidation or a proposal, success means staying current. Pick the path you can actually maintain; missed payments on either option can set you back.

3) Credit Score Impact: Short-Term vs. Long-Term

Debt Consolidation (Loan/HELOC/Second Mortgage):

-

Short-term: A hard inquiry and a new tradeline may dip your score slightly. Paying off high-utilization cards can boost your score within a few reporting cycles.

-

Medium to long-term: On-time payments and lower utilization can lead to steady recovery and often higher scores than before.

Consumer Proposal:

-

Short-term: Credit file shows a serious event. Expect a significant drop.

-

During the proposal: New credit is limited; some secured products (e.g., secured cards) may help rebuild slowly.

-

After completion: The mark remains for a period after discharge (commonly up to 3 years post-completion for major bureaus; timelines can vary). Rebuild is possible, but patience is required.

Bottom line: If you can qualify for consolidation at a reasonable rate and manage payments, you typically protect your long-term credit outlook better than with a proposal. If you cannot qualify, a proposal is still a credible path to reset.

4) Costs, Fees & Total Interest: Where the Money Really Goes

Here’s a quick comparison to understand what you pay and why.

| Cost Factor | Debt Consolidation | Consumer Proposal |

|---|---|---|

| Upfront fees | May include appraisal, legal, broker/lender fees (especially for home-equity or alternative loans). | Built into the proposal payments; the LIT’s fees come from what you repay (you don’t pay them on top). |

| Interest | You pay interest at the loan’s rate. With home equity, this rate can be far lower than credit cards. | No ongoing interest on included unsecured debts once the proposal is accepted. |

| Total paid | Principal + interest + closing costs. Can be less than current trajectory if your rate meaningfully drops. | A portion of your original principal (the settlement) + trustee fees (included). Usually much less than carrying everything at high interest. |

| Tax implications | Interest may not be tax-deductible (personal debt). | Forgiven debt is generally not taxed as income in Canada for consumer proposals (speak with a tax pro for your specifics). |

Key insight: If you’re a homeowner with decent equity, consolidation can dramatically lower interest costs compared to credit cards. If you’re not a homeowner or can’t qualify, a consumer proposal can dramatically lower total principal owed—often the cheapest path to clean slate when consolidation isn’t on the table.

5) Timelines: How Fast You Can Be Debt-Free

-

Debt consolidation: Terms vary from 1–5 years (unsecured) and potentially longer for home-equity-backed loans. Paying extra can speed things up.

-

Consumer proposal: Typically up to 5 years. You can pay it off early if funds become available (e.g., bonus, tax refund, family help), which shortens the credit-reporting tail after completion.

Speed tip: If cash flow improves, accelerate payments—either option gets cheaper and shorter if you prepay.

6) Homeowners vs. Renters: Different Paths That Make Sense

Homeowners (Ontario):

-

If you have equity, explore home equity refinancing, HELOC, or a second mortgage. Even with bruised credit, there may be B-lenders or private options that beat the math of high-interest unsecured debt.

-

Consolidation can also help you prepare for mortgage renewal by cleaning up revolving balances and lowering utilization.

-

If there’s not enough equity or your income is too tight, a proposal might be the safest reset.

Renters (Ontario):

-

Without collateral, consolidation approvals depend on income, debt-to-income, and credit.

-

If approvals are tough or rates are too high to make consolidation worthwhile, a consumer proposal offers structured relief and legal protection from collections.

7) Real-Life Scenarios (3 Ontario Case Studies)

Case 1: The Equity-Rich Homeowner

Megan in Whitby owes $38,000 on credit cards/lines at high rates. She has $300,000 in home equity. Even with a moderate credit dip, a second mortgage at a lower rate consolidates all balances. Her new monthly payment is lower, cash flow stabilizes, and her utilization plummets. Within 6–12 months of on-time payments, her score improves, positioning her for a stronger mortgage renewal.

Why consolidation won: The cost of funds was much lower than her unsecured rates, and the credit trajectory was positive.

Case 2: The Renter With Limited Income

Jake in Barrie owes $28,000 on credit cards and a personal loan. High utilization, recent late payments, and income variability make him a poor candidate for a low-rate consolidation loan. A consumer proposal reduces his repayable amount to $14,000 over 48–60 months, stops interest, and ends collection stress.

Why the proposal won: He couldn’t qualify for an affordable consolidation. The proposal delivered predictable payments and legal protection.

Case 3: The Owner Facing Renewal in 10 Months

Alicia in Oshawa owes $45,000 across cards/LOCs. Mortgage renewal is coming. A consumer proposal now would likely restrict her lender pool and push her into less favourable renewal terms. Instead, she uses a HELOC to consolidate, slashing interest and cleaning up utilization. At renewal, she qualifies with an A-lender and later accelerates HELOC repayments.

Why consolidation won: It protected her renewal options and overall borrowing costs.

How to Decide (Quick Decision Framework)

Use this decision tree to get a direction fast:

-

Can you qualify for a consolidation loan at a rate that meaningfully beats your current weighted average interest?

-

Yes: Lean consolidation (especially with home equity).

-

No / Unsure: Go to #2.

-

Is cash flow too tight even after a hypothetical consolidation at that better rate?

-

Yes: A consumer proposal may fit better—because it reduces principal and freezes interest.

-

No: Consolidation may still work—adjust term length to hit a comfortable payment.

-

Is a mortgage renewal coming up within 12–18 months?

-

Yes (homeowner): Strongly consider consolidation first to keep renewal options open.

-

No: Choose the option that best balances payment relief and long-term credit health.

-

Are collections/garnishments already in motion?

-

Yes: A consumer proposal can stop them and provide legal protection quickly.

-

No: You have more time to price out consolidation options and compare.

Remember: The “best” path is the one you can finish with confidence.

FAQs: Ontario-Specific Rules You Shouldn’t Ignore

Q1: Will a consumer proposal erase all my debts?

No. It generally covers unsecured debts (credit cards, lines of credit, personal loans, some tax debt). Secured debts (like mortgages or car loans) aren’t included—you must keep paying those if you want to keep the asset.

Q2: Can I keep my home if I file a consumer proposal?

Yes, as long as you continue to meet your mortgage obligations and your lender doesn’t take action for other reasons. Many homeowners file proposals while keeping their homes, but always review equity, affordability, and renewal timing.

Q3: How long does a consumer proposal affect my credit?

While exact reporting rules can vary by bureau and change over time, expect the mark to remain during the proposal and for a period after completion (commonly up to 3 years post-completion). You can rebuild with time, secured products, and spotless payment history.

Q4: Is debt consolidation always cheaper than a consumer proposal?

Not always. If consolidation rate/fees are too high—or you can’t qualify—your total cost may still exceed a proposal’s reduced principal. You have to run the numbers.

Q5: What if I start one option and it isn’t working?

-

If a consolidation payment proves too heavy, don’t wait—talk to a qualified professional about alternatives (including proposals) before missing payments.

-

If a proposal payment is too high, you might discuss a variation with your LIT, or explore early payout if your situation improves.

Q6: Does either option include payday loans or CRA tax debt?

-

Consolidation: It can pay off payday loans and some tax balances if the lender approves the loan amount.

-

Consumer proposal: Often includes payday loans and can cover many CRA debts; your LIT will confirm which obligations are eligible.

Q7: Can I get new credit during a proposal?

Yes, but expect limited options and higher costs. Many people use secured credit cards as part of the rebuild strategy.

Next Steps & Free Checklist

If you’re in Ontario and weighing debt consolidation vs. consumer proposal, here’s a simple action checklist to move forward confidently:

-

List all debts (balances, rates, minimum payments, creditor names).

-

Calculate your current weighted average interest rate.

-

Run a consolidation scenario at a realistic rate & term (with/without home equity).

-

Test proposal math: What could you afford monthly for 48–60 months?

-

Check your timeline (any mortgage renewal or major life event in the next 12–18 months?).

-

Decide your priority: credit preservation vs. maximum immediate relief.

-

Get expert eyes on the numbers:

-

Homeowners: Ask a mortgage professional to assess HELOC/second mortgage options (including B-lenders/private).

-

All borrowers: Book a free chat with a Licensed Insolvency Trustee to understand potential proposal terms.

-

-

Choose the option you can complete—and set up automatic payments to stay on track.

-

Start rebuilding immediately: keep utilization low, avoid new high-interest debt, and set aside a small emergency fund.

-

Re-evaluate in 6 months: if income improves, consider prepayments or early payout strategies.

Final Word

There’s no one-size-fits-all answer. Debt consolidation shines when you can secure a meaningfully lower rate, protect your credit trajectory, and align payments with your cash flow—especially for Ontario homeowners with usable equity. Consumer proposals deliver powerful relief when consolidation approvals aren’t feasible or when you need legal protection and principal reduction to reset.

Whichever path you choose, the real victory is the one you can finish—calmly, consistently, and on your terms.

Need to consolidate debt?

Talk to a mortgage professional today about using your equity to consolidate debts.