If you’ve completed (or are completing) a consumer proposal and you’re wondering whether homeownership is still on the table—good news: you can absolutely qualify for a mortgage after a consumer proposal. The path is different, and the rules are tighter, but with the right strategy you can move from “proposal” to “pre-approval” faster than you think.

This guide breaks down exactly how Canadian lenders assess risk, what documents and down payments you’ll need, how timing affects your rate options, and the 7 helpful ways to boost your approval odds.

Can You Get a Mortgage After a Consumer Proposal?

Short answer: yes. Lenders look at three things first:

-

Stability: Have you completed the proposal or are you on track?

-

Re-established credit: Do you have active, paid-on-time trade lines?

-

Affordability: Does your income support the payment given today’s rates and your debt ratios?

Even if you’re still in a consumer proposal, certain lenders may consider a mortgage or refinance if there’s enough equity and a credible repayment plan. Once your proposal is completed and you’ve rebuilt credit, your options expand significantly.

How Lenders See a Consumer Proposal (A, B & Private Lenders)

Not all lenders are the same. Here’s the broad framework:

-

A-lenders (big banks, prime insurers)

Typically want the proposal fully completed and seasoned (often 1–2 years of clean credit history after completion), stable income, and strong ratios. Best rates live here, but requirements are strict. -

B-lenders (alternative lenders)

More flexible with recent proposals. They’ll weigh income strength, down payment/equity, and credit re-establishment. Rates and fees can be higher than A-lenders, but approvals are more achievable earlier in your recovery. -

Private lenders

Primarily equity-focused. Useful for bridge scenarios (e.g., refinance to pay off the proposal in full, then move to B or A once credit stabilizes). Rates/fees are higher and terms are usually 1–2 years.

Takeaway: Your fastest path may be a staged strategy: Private ➝ B-lender ➝ A-lender, as your credit and proposal season.

Timing Matters: During, Right After, and 24 Months Post-Proposal

Timing influences both approval odds and pricing:

-

During proposal:

Possible with sufficient equity for a refinance, or with a larger down payment for a purchase through alternative lending. You’ll need a credible plan to complete/pay out the proposal. -

0–12 months after completion:

B-lenders are often accessible if you’ve re-established at least two active trade lines and shown perfect payment history. -

12–24+ months after completion:

Your file can start to look “prime-ready.” With stable income and low total debt service ratios, you can often graduate to A-lender pricing.

What to Expect: Rates, Down Payments & Insurance

-

Rates: Expect a premium compared to prime in the early months after a consumer proposal. As your file seasons and your credit score climbs, the premium shrinks.

-

Down payment:

-

Purchase: The stronger your down payment, the easier the approval. Alternative lenders may prefer 10%–20%+.

-

Refinance: Lenders look at loan-to-value (LTV)—lower LTV = easier approval.

-

-

Default insurance: If you’re aiming for minimum down payment insured options, be prepared for stricter underwriting and a longer seasoning period post-proposal. Many borrowers instead use larger down payments with alternative lenders, then refinance to prime later.

Your Mortgage Approval Toolkit (Documents & Proofs)

Have these ready to keep your file clean and fast:

-

Consumer proposal documents: Certificate of full performance (if completed), payment history, and remaining balance (if mid-proposal).

-

Income:

-

Salaried: 2 recent pay stubs, employment letter, T4s/NOAs as requested.

-

Self-employed: 2 years NOAs/T1s, business financials, GST/HST filings if applicable, and bank statements showing cash flow.

-

-

Credit: Two or more active trade lines (credit card, loan, secured card) with on-time payments.

-

Down payment proof: 90-day history (paper trail for deposits/gifts).

-

Property details: MLS feature sheet or tax bill/statement for refinance, current mortgage statement.

-

Budget summary: To demonstrate realistic affordability and strong residual income.

7 Helpful Ways to Get a Mortgage After a Consumer Proposal

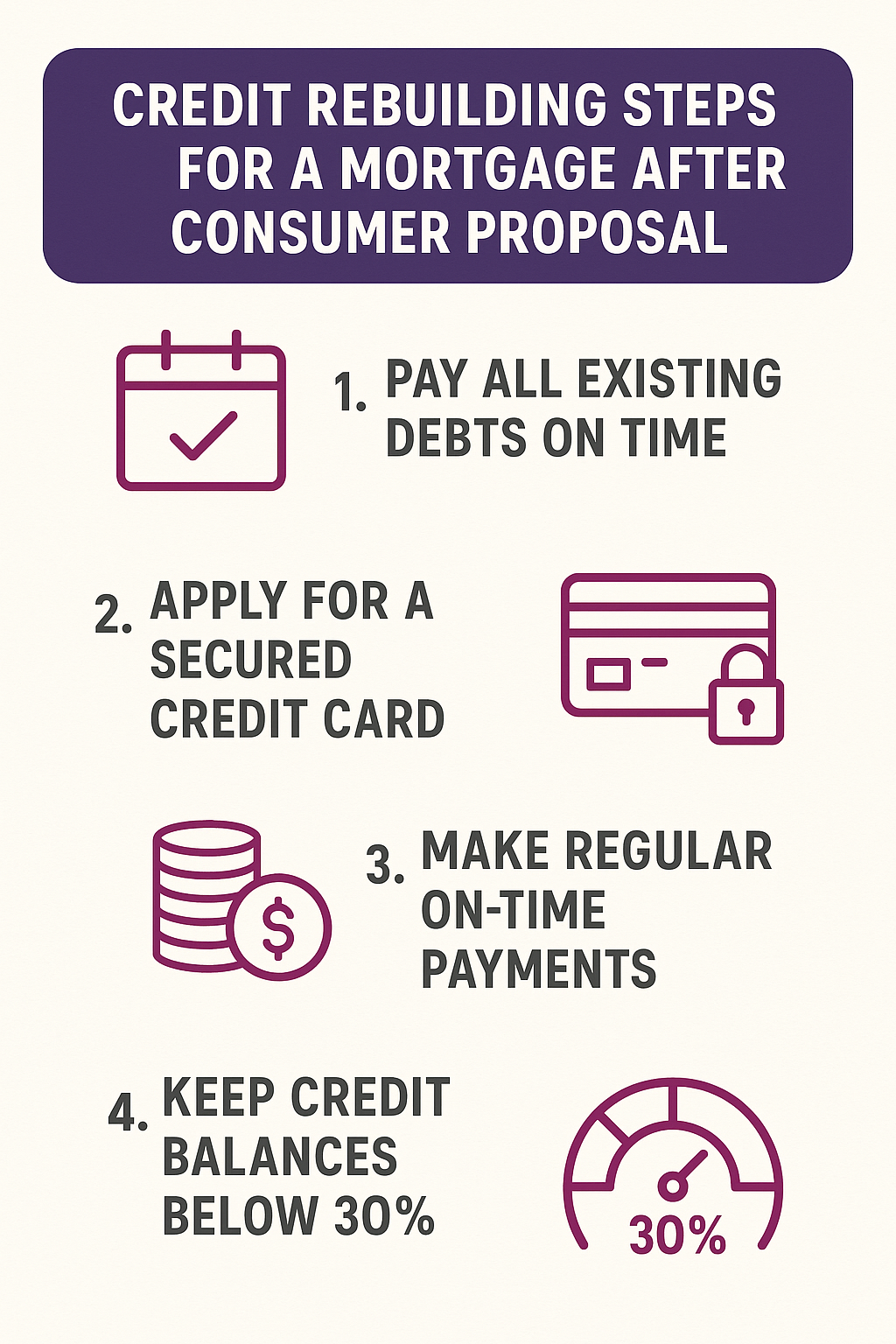

1) Re-establish Two Strong Trade Lines—Now

Lenders love recent, clean credit. Aim for two trade lines with limits that fit your budget (e.g., $1,500–$3,000 each). If you’re rebuilding, start with secured credit cards, then graduate to unsecured. Keep utilization under 30% and pay on time every month.

2) Season Your File With Perfect Payment History

Your report should tell a simple story: you borrowed, you paid—on time. A 12–24 month streak of punctual payments after proposal completion is incredibly persuasive to underwriters. Automate payments to avoid slip-ups.

3) Strengthen Your Down Payment or Equity Position

More skin in the game reduces lender risk. For purchases, target 10–20%+ down if prime insured options aren’t available yet. For refinances, keep your LTV conservative. Strong equity can unlock approvals even while you’re still mid-proposal.

4) Optimize Your Debt Ratios (TDS/GDS)

Lenders use gross debt service (GDS) and total debt service (TDS) to assess affordability. Lower is better. Ways to improve:

-

Pay off/settle any small lingering balances.

-

Consolidate non-mortgage debt if it reduces monthly obligations.

-

Avoid new vehicle or installment loans before applying.

-

Increase verifiable income (more on that next).

5) Solidify Verifiable Income (Employees & Self-Employed)

-

Employees: Ensure your employment letter confirms position, full-time status, and base income. If hours vary, gather a 12-month average proof via pay statements.

-

Self-employed: Prepare two years of filed returns/NOAs if possible. If your latest year is stronger, highlight it. Provide business bank statements showing steady deposits. For commission/contract income, document the history and pipeline.

6) Consider a Staged Lender Strategy to Lower Your Cost Over Time

Approval now, lowest cost later. A common path is:

-

Private (if needed to finish proposal or bridge an immediate need).

-

B-lender (as credit re-establishes and payment history seasons).

-

A-lender (12–24+ months post-completion when your profile is prime-ready).

Build this roadmap upfront so you know how and when you’ll reduce rates/fees.

7) Work With a Broker Who Knows Proposal Files Cold

A specialized broker understands which lenders will entertain during-proposal scenarios, which want completion certificates, who accepts gifted down payment, and who values rapid re-score or alternative proofs. They’ll also package your story for underwriters, which can be the difference between declined and approved.

Buying vs. Refinancing After a Consumer Proposal

Buying a Home

-

Stronger down payment can offset recent proposal history.

-

Expect manual underwriting—be ready to explain the proposal cause, how you corrected course, and why the new payment is sustainable.

-

A co-borrower or guarantor with strong credit can help, but both debt ratios and long-term sustainability still matter.

Refinancing Your Current Home

-

Equity-driven approvals are common with private and B-lenders.

-

Use a refinance to pay out the consumer proposal entirely, then begin your seasoning clock for A-lender eligibility.

-

Keep closing costs and prepayment penalties in view; design a plan that reduces total borrowing cost over 12–36 months, not just the next 60 days.

Common Mistakes to Avoid

-

Applying too early with no trade lines or recent late payments.

-

Maxing out new credit and carrying high balances—your utilization matters.

-

Taking on a car loan before your mortgage—this crushes TDS.

-

Skipping documentation (no paper trail on down payment, missing NOAs).

-

Shopping randomly with multiple credit pulls—instead, use a broker to target the right lenders.

FAQs: Mortgages After a Consumer Proposal

1) Can I get a mortgage while still in a consumer proposal?

Yes, in some cases—especially for refinances with equity or purchases with larger down payments through alternative or private lenders. Approval hinges on affordability, equity, and a credible plan to complete the proposal.

2) How long after completing a proposal can I qualify with a bank (A-lender)?

Many borrowers see prime options around 12–24 months after completion, with strong re-established credit and on-time payments. Your exact timeline depends on income, ratios, and credit depth.

3) Do I need a big down payment to buy after a proposal?

Not always, but a larger down payment increases approval odds and can reduce the rate premium. Alternative lenders often prefer 10–20%+ down.

4) Will my interest rate be much higher?

Initially, likely higher than prime. As you build payment history and season post-proposal, you can often refinance into lower-cost options.

5) What credit score do I need?

There’s no single number. Lenders look at the whole file—trade lines, utilization, late payments, income stability, and LTV. A rising score plus two clean trade lines for 12+ months is a strong signal.

6) Can a co-signer help?

Yes, a credit-strong co-signer can improve ratios and confidence. But long-term affordability still matters; the goal is a sustainable payment on your own merits over time.

7) Is it better to refinance to pay off the proposal first?

Often, yes—if the numbers work. Paying out the proposal can open doors to more lenders sooner. But weigh fees, penalties, and future refinance timelines with a broker.

8) Will multiple mortgage inquiries hurt my chances?

Excessive, scattershot pulls aren’t ideal. Work with a broker who targets the right lenders based on your profile to minimize unnecessary inquiries.

Next Steps & How We Can Help

If you’re serious about getting a mortgage after a consumer proposal, the winning move is a clear, staged plan:

-

Credit Re-establishment: Two active trade lines, low utilization, automated payments.

-

Income & Docs: Employment letter, pay stubs or full self-employed package, down payment paper trail.

-

Lender Roadmap: Choose the fastest path to approval now with a defined refinance/downshift to better pricing later.

-

Timeline & Targets: Set milestones for when you can graduate from private ➝ B ➝ A.

Ready to map your path to approval?

Reach out to the Lendtoday team and we’ll review your proposal status, credit, income, and goals—then design a lender-by-lender plan to get you home, and get your cost down over time.

Final Word

A mortgage after a consumer proposal isn’t just possible—it’s common with a smart plan. Nail down two strong trade lines, keep payments perfect, document your income, and pick the right lender at the right time. With a staged approach, you can get approved now and lower your cost as your credit score improves.

- Can a Mortgage Company Evict You in Ontario? (2026 Power of Sale Guide) - February 23, 2026

- Crucial Ways to Survive the Redemption Period During Foreclosure: A Guide - February 21, 2026

- Painful Realities of the Interest Rate Differential Penalty You Must Know - February 15, 2026