Why Credit Rebuilding Is Different for Homeowners

As a homeowner, you already have secured debt (your mortgage) and often have available equity. That opens strategies renters can’t access, like consolidating high-interest cards into a lower-rate mortgage refinance, HELOC, or second mortgage—dropping utilization quickly and freeing up monthly cash flow. Rebuilding is about both score and affordability, so you can qualify for better terms at renewal.

Helpful resources on LendToday.ca:

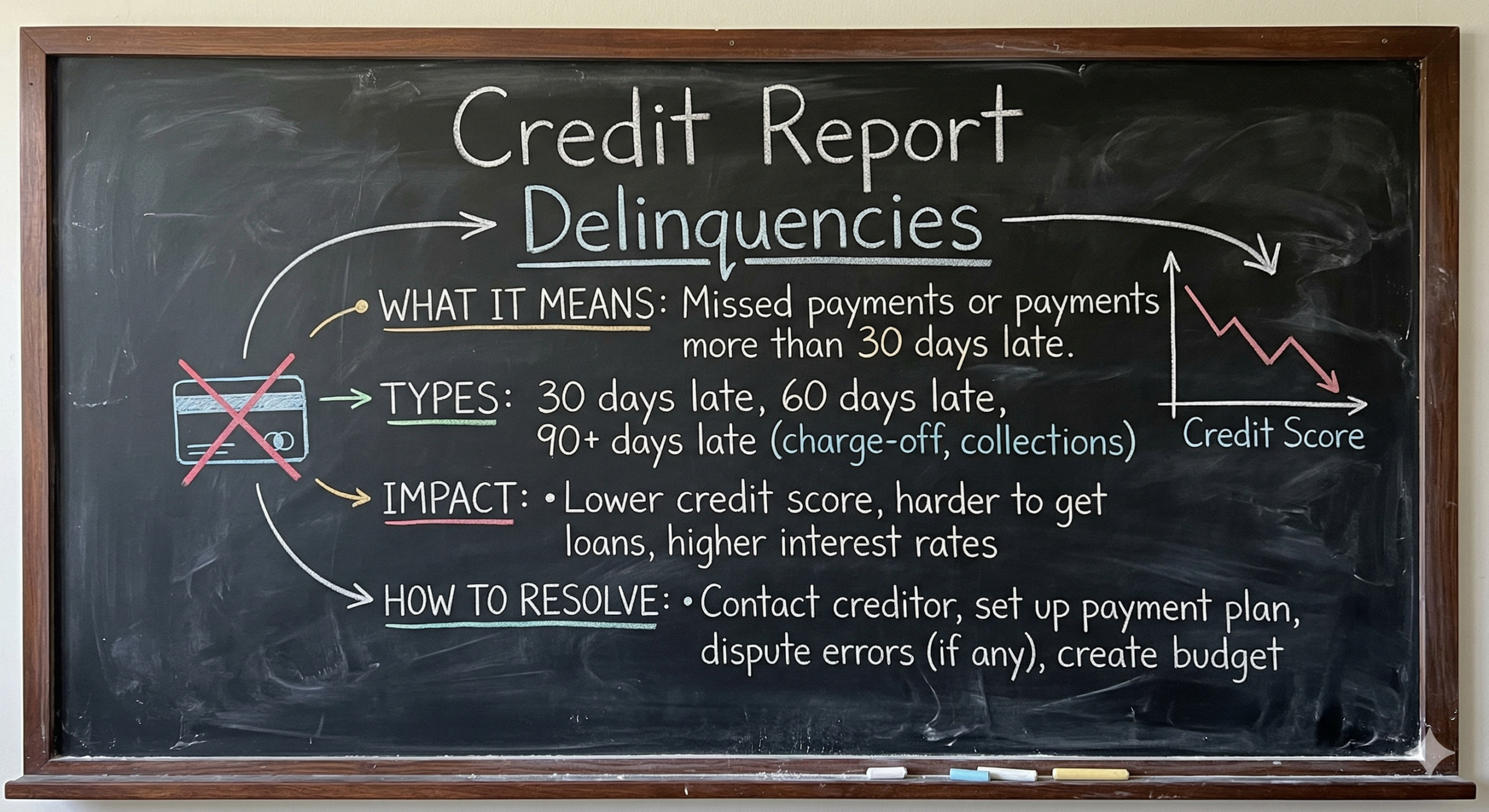

How Canadian Credit Scores Work (Plain-English)

While scoring models vary (FICO, bureau variants), the pillars are consistent:

-

Payment history (35%) — On-time wins; late payments hurt.

-

Utilization (30%) — Your balances vs limits on revolving accounts. Stay below30% per card; 10% is ideal before applications.

-

Credit age (15%) — Older accounts help.

-

Mix (10%) — Blend of revolving (cards/LOC) + installment (loans/mortgage).

-

New inquiries (10%) — Too many hard pulls in a short window can ding scores.

Bottom line: Perfect payment history and low utilization are your fastest levers.

The 10-Tool Credit Rebuild Playbook (Canada)

1) Turn On Auto-Pay Everywhere

Why: Payment history is the biggest factor.

How: Enable auto-pay (at least minimum due) on cards, loans, utilities, and phone bills. Keep a one-month chequing buffer to avoid NSF.

2) Drive Utilization below 30% (Goal: Less than 10%)

Why: The fastest lever for score gains.

How:

-

Make mid-cycle payments (before statement date).

-

Request soft-pull limit increases.

-

Spread balances so each card stays below 30%.

Homeowner advantage: Use a HELOC or second mortgage to clear high-interest cards and report low balances. See: Home Equity Loans & HELOCs.

3) Add a Secured Credit Card (If Thin/Damaged File)

Why: Builds a positive history safely.

How: One reputable secured card (deposit $500–$2,000), spend <10% of the limit, pay in full monthly.

4) Layer a Credit-Builder Loan (Installment Trade Line)

Why: Improves credit mix and on-time history.

How: Small 12–24 month term; some programs release savings at maturity.

5) Time Your “Rapid Rescore” Moment (Balance Reporting)

Why: Scores lag until bureaus receive updated balances.

How: Pay down cards, then apply after statement cut dates so low balances are reported.

6) Dispute Only Genuine Errors

Why: Deleting an inaccuracy can pop scores.

How: Pull Equifax and TransUnion; dispute provably wrong items (mixed files, duplicates, paid accounts showing open). Keep documentation.

7) Consolidate Strategically (Refi / HELOC / Second Mortgage)

Why: Converts high-rate revolving debt to lower-rate installment debt, slashing utilization and interest.

Options:

-

Refinance near renewal (or earlier if the penalty math still nets savings).

-

HELOC for flexible payoff (commit to a repayment plan).

-

Second mortgage as a short-term bridge with an exit plan to a prime product.

Start here: Second Mortgage in Ontario | Mortgage Renewal Options

8) Use a Payment Calendar + Snowball/Stack

Snowball: Pay the smallest balance first for momentum.

Stack (Avalanche): Pay the highest interest first for maximum savings.

Tip: Combine with consolidation to clear multiple cards at once, then attack the new lower-rate balance aggressively.

9) Keep Old Accounts Open (Fee-Free)

Why: Preserves average age and total available limit.

How: If a card has an annual fee, downgrade to a no-fee version instead of closing.

10) Put One Small Recurring Bill on a Low-Limit Card

Why: Ensures ongoing positive reporting with low utilization.

How: Add a $10–$25 subscription + auto-pay. Set and forget.

30-Day Quick-Start Checklist

Week 1

-

Pull Equifax + TransUnion; list balances, limits, statement dates.

-

Turn on auto-pay for every account.

-

Choose the snowball or stack strategy.

-

If utilization is high, explore HELOC/second mortgage quotes.

Week 2

-

Make mid-cycle payments to bring each card ≤30% (aim <10%).

-

Apply for one secured card (if needed) and add a tiny recurring bill.

Week 3

-

Dispute genuine report errors with documents.

-

Finalize consolidation if using refi/HELOC/second mortgage; pay cards to near-zero.

Week 4

-

Let statements cut and confirm the low balances reported.

-

Avoid new hard pulls.

-

Re-check scores; document progress.

Renewal/Refi Strategy with Bruised Credit

-

Start 6–9 months before renewal to allow multiple low-utilization cycles to report.

-

Broker-shop smartly: one bureau pull, many lender options.

-

Stage your exit:

-

Stage A (12-24 months): Use a B-lender/private solution to consolidate and rebuild on-time history.

-

Stage B: Refinance back to an A-lender once scores and ratios improve.

-

-

Over-document: NOAs, pay stubs, letters of explanation for past late payments.

Mistakes to Avoid

-

Closing your oldest card (hurts age + utilization).

-

Stacking multiple new applications in a short window.

-

Re-maxing a HELOC after you clear cards—protect the win.

-

Ignoring statement dates (that’s when utilization is captured).

-

Relying on “repair” shortcuts, focus on accurate reporting and fundamentals.

Questions and Helpful Answers

1. How fast can I raise my score?

If utilization is high, lowering balances below 30% (ideally 10%) can help within 1-2 statement cycles. Late payments take longer to offset; consistent on-time history over 6-18 months is key.

2. Will a second mortgage or HELOC hurt my score?

You’ll get a hard inquiry (small, temporary dip). Paying down revolving balances usually creates a net positive once low balances are reported.

3. Should I close cards after consolidating?

Generally no. Keep fee-free cards open to preserve age and available limit; place a tiny recurring bill + auto-pay.

4. Can I rebuild during a consumer proposal or after bankruptcy?

Yes—start with a secured card and possibly a credit-builder loan. Homeowners may leverage equity for consolidation once eligible; timing is crucial.

5. Do utilities/phone bills help?

Missed payments can hurt. Some providers report positive history—assume on-time always, and ask your provider what’s reported.

How To: Lower Credit Utilization Before a Mortgage Application

Goal: Reduce revolving utilization under 30% (target should be 10%) within 30-60 days.

Steps:

-

List accounts with balances, limits, and statement dates.

-

Make mid-cycle payments one week before each statement date.

-

Re-distribute balances to keep each card below 30%.

-

Request soft-pull limit increases if available.

-

Consolidate high-interest debt using a HELOC/second mortgage to drop utilization quickly.

-

Apply after statements cut so low balances are reported.

Copy-and-Paste This Handy Checklist

-

Auto-pay on all accounts

-

Push each card below 30% (with a goal 10%) before the statement date

-

Add one secured card if thin/damaged

-

Consider a credit-builder loan (12–24 months)

-

Explore HELOC/second mortgage for consolidation

-

Dispute genuine errors only

-

Keep oldest cards open (fee-free)

-

Put a small recurring bill on one card + auto-pay

-

Avoid clustered hard pulls

-

Re-check scores after statements cut

You don’t have to wait a year to feel a difference. With the right plan, on-time payments, low utilization, and the smart use of home equity, you can rebuild faster. If you’re a Canadian homeowner ready to turn momentum into measurable score gains, the LendToday.ca team can help

Credit Score Bruised?

Talk to a mortgage professional today about using your equity to consolidate debts.