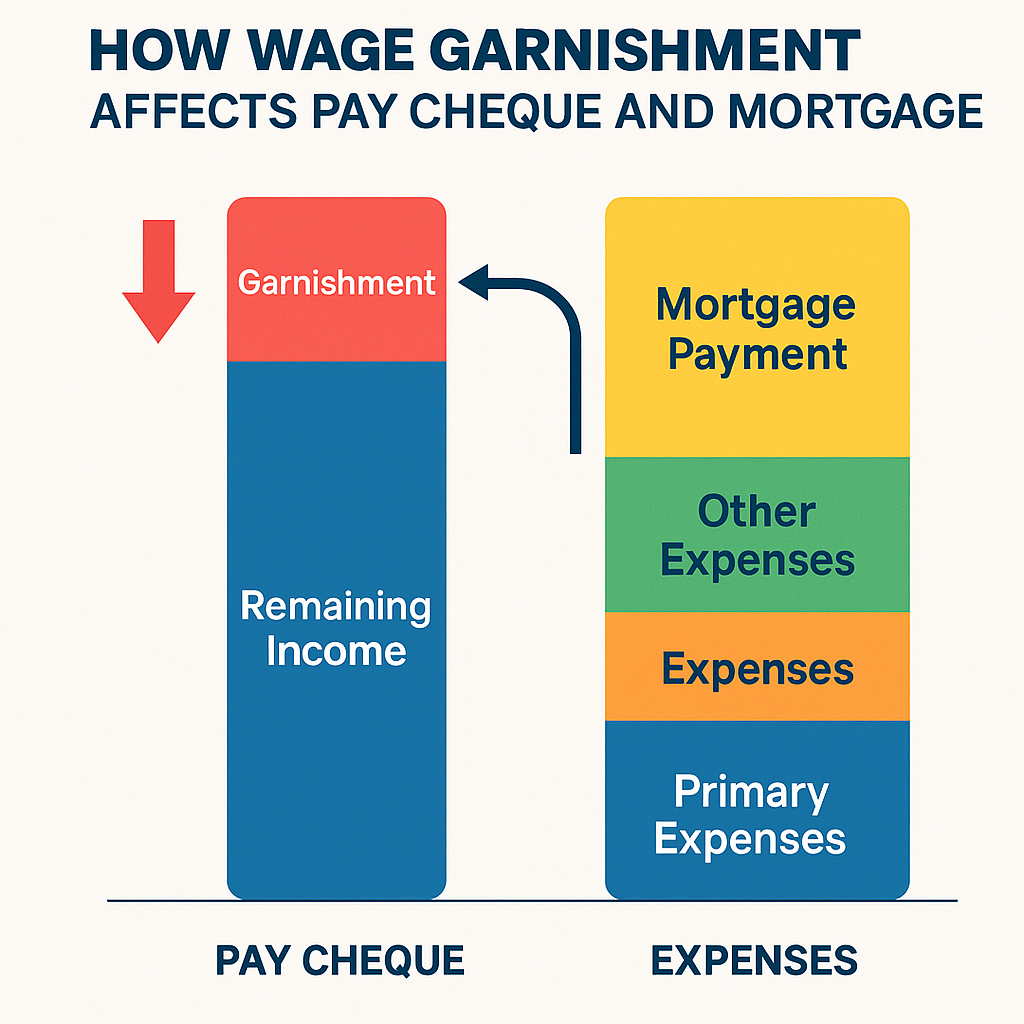

Wage garnishment in Canada happens when creditors or the Canada Revenue Agency (CRA) legally deduct money from your pay cheque to recover unpaid debts. For homeowners, this can make keeping up with mortgage payments harder and create serious financial strain. However, Canadian borrowers can use home equity-based solutions—such as a home equity loan, HELOC, or second mortgage – to pay off the debt and stop wage deductions. Acting quickly helps protect your property, rebuild cash flow, and prevent damage to your credit.

Understanding Wage Garnishment in Canada

Quick Answer:

Wage garnishment is a legal process that allows a creditor or the CRA to collect debts by taking a portion of your income directly from your employer before you’re paid.

In Canada, wage garnishment usually occurs after a creditor obtains a court judgement, or when the CRA enforces tax arrears. Once in place, your employer must remit a specific percentage of your pay cheque until the debt is repaid.

-

Typical range: 20% to 50% of your net pay can be garnished, depending on the province and the type of debt.

-

CRA garnishments: Do not require court approval and can take up to 50% of your wages or 100% of self-employment income.

-

Court-ordered garnishments: Require legal proceedings and a judge’s authorization.

If you live in Ontario, Alberta, or British Columbia, the garnishment laws differ slightly. For example, Ontario’s Wages Act limits garnishment to 20% of net wages in most cases, while Alberta allows up to 50% for larger debts.

Key takeaway:

Wage garnishment immediately reduces your disposable income and affects your ability to keep up with essential expenses, especially your mortgage payments.

How Wage Garnishment Impacts Mortgage Payments

Reduced Income and Increased Stress

When a wage garnishment hits, your take-home pay shrinks overnight. If your mortgage payment remains the same, your budget is instantly strained. Even a 20% deduction can disrupt your ability to cover utilities, groceries, and loan obligations.

For instance, if you earn $4,000 monthly and lose 25% ($1,000) to garnishment, that leaves only $3,000 for all living expenses. If your mortgage is $2,000, you’re now operating with minimal breathing room.

Late or Missed Payments

Missed mortgage payments lead to late fees, higher interest, and can cause your lender to report delinquencies to credit bureaus. Two or more missed payments can trigger default proceedings or even power of sale or foreclosure, depending on your province.

Credit Score and Refinancing Challenges

A wage garnishment signals to lenders that you’re under financial stress. Your credit score will likely drop due to missed payments or the legal judgment itself, limiting future borrowing opportunities.

Quick Example:

A Whitby homeowner earning $80,000 per year faced a 30% CRA garnishment for unpaid taxes. Their monthly mortgage and debt payments exceeded what remained from each pay cheque. By securing a second mortgage, they paid off the CRA in full, stopped the garnishment, and reduced monthly obligations by over $700.

Important to note:

Communicating early with your lender or broker is crucial. Many lenders are willing to help restructure payments before a foreclosure process begins.

Types of Wage Garnishment in Canada

1. CRA Wage Garnishment (Tax Arrears)

When taxes go unpaid, the CRA can garnish wages, freeze bank accounts, or place liens on property. CRA garnishment is powerful because it does not require a court order.

2. Court-Ordered Wage Garnishment (Judgments and Writs)

Private creditors, like credit card companies or lenders, must obtain a court judgment first. Once approved, a writ of seizure or garnishment is served to your employer.

3. Family Support Garnishment

For unpaid spousal or child support, courts can order up to 50% of wages to be deducted.

Mini-summary:

Each type of garnishment carries different legal authority and repayment rules. However, all these reduce disposable income and put mortgage stability at risk.

Using Home Equity to Manage Wage Garnishment

When wage garnishment limits your income, your home equity can be your strongest financial tool.

Home Equity Loan

A home equity loan provides a lump-sum amount based on the appraised value of your home and remaining mortgage balance.

-

Fixed rate and term.

-

Ideal for paying off garnishment-related debts or judgments in full.

-

Interest rates typically range from 7% to 12%, depending on credit and loan-to-value (LTV).

Home Equity Line of Credit (HELOC)

A HELOC works like a revolving line of credit. You borrow only what you need and pay interest on the used amount.

-

Flexible repayment structure.

-

Great for managing reduced income or covering temporary shortfalls.

-

Typically variable at prime + 1–3%.

Second Mortgage

A second mortgage is registered behind your existing mortgage.

It offers a larger lump sum than a HELOC, often used for:

-

Paying off CRA debts or court judgments.

-

Consolidating multiple high-interest obligations.

-

Catching up on arrears.

Quick Example:

A Toronto homeowner faced both wage garnishment and property tax arrears. Using a second mortgage, they cleared the CRA balance and municipal taxes, restoring full income and avoiding foreclosure.

Key takeaway:

Equity-based borrowing solutions like a second mortgage or HELOC can stop garnishments by paying off the underlying debt, protecting your pay cheque and your home.

Refinancing During or After Wage Garnishment

Refinancing can be another effective way to eliminate wage garnishment, but it depends on your current mortgage, credit score, and home equity.

When Refinancing Makes Sense

-

You have significant equity in your home (typically 20% or more).

-

You want one lower monthly payment by consolidating debts.

-

Your credit score, while impacted, still qualifies with a B-lender or private lender.

Challenges to Expect

-

Traditional banks may decline applications due to recent garnishments.

-

Private or alternative lenders often step in when institutional lenders say no.

-

Expect slightly higher rates but faster approval and flexibility.

Important to note:

Waiting too long can cause further credit damage. The earlier you refinance or secure a second mortgage, the more equity you preserve.

Mini-summary:

Refinancing replaces your current mortgage with a new one that pays off all debts, including garnished accounts, into a single manageable payment.

What To Do If You’re Facing Wage Garnishment

Step 1: Review the Garnishment Notice

Verify the creditor, amount owed, and the type of debt. Mistakes sometimes occur, especially with older or transferred debts.

Step 2: Contact the Creditor or CRA

Negotiate repayment terms or request a voluntary payment plan. CRA agents may reduce or pause garnishment if you show good-faith effort.

Step 3: Consult a Mortgage Broker or Financial Expert

Professionals can assess whether a home equity loan, HELOC, or second mortgage could stop the garnishment and restore your cash flow.

Step 4: Avoid High-Interest Unsecured Loans

Payday loans or unsecured personal loans can worsen your debt situation. Stick with secured, equity-based borrowing.

Step 5: Prioritize Your Mortgage

Protecting your home should remain your top financial goal. Missing mortgage payments can trigger legal action much faster than other debts.

Mini-summary:

Taking quick, informed action can prevent escalating financial damage. Don’t ignore the notice; use your home’s value as leverage to regain control.

How to Prevent Wage Garnishment in the Future

-

Maintain communication with creditors: Silence leads to legal action; dialogue leads to solutions.

-

Automate payments: Set up direct withdrawals for bills and mortgage payments.

-

Create an emergency fund: Aim for at least three months of living expenses.

-

Review credit reports regularly: Identify potential issues before they escalate.

-

Seek debt counselling: Non-profit agencies can help structure payment plans before garnishment happens.

Key takeaway:

Financial stability begins with proactive planning, budgeting, responsible borrowing, and using equity strategically.

💡 Equity-Based Solutions for Wage Garnishment Relief

| Solution | Type | Best For | Typical Interest (2025) | Flexibility |

|---|---|---|---|---|

| Home Equity Loan | Lump-sum | Paying judgments, debt consolidation, and property taxes | 6–12% | Fixed term |

| HELOC | Revolving | Managing monthly expenses, debt consolidation, and property taxes | Prime + 1–3% | High |

| Second Mortgage | Lump-sum | Clearing arrears, CRA debts, and property taxes | 8–14% | Fixed term |

| Refinance | Full mortgage replacement | Debt consolidation, home renovations and more | 6–10% | Medium |

Tip: Equity-based financing can help stop wage garnishment, clear CRA debts, and restore cash flow fast.

Key Takeaways for Canadian Homeowners

-

Wage garnishment can reduce income by 20–50%, quickly impacting mortgage affordability.

-

CRA garnishments are powerful but can be stopped by paying off tax debt using home equity.

-

Equity-based borrowing (HELOC, home equity loan, or second mortgage) provides flexibility and relief.

-

Private and B-lenders often approve financing when banks decline.

-

Acting early preserves equity and protects your credit rating.

Frequently Asked Questions

1. Can I get a mortgage while under wage garnishment in Ontario?

Yes, it’s possible, especially with private lenders. Approval depends on your available home equity and property value rather than just income or credit score. A second mortgage can provide the funds to stop garnishment and improve cash flow.

2. Can a home equity loan stop CRA wage garnishment?

Absolutely. Paying off the tax debt in full through a home equity loan or refinance can cause the CRA to lift the garnishment almost immediately.

3. How much of my pay cheque can be garnished in Canada?

Generally, up to 20% of net pay in Ontario, up to 30% in British Columbia, and up to 50% in Alberta. The CRA may garnish up to 50% of wages or 100% of self-employed income.

4. Does wage garnishment affect my credit score?

Yes. It appears as a legal judgment or debt collection and can drop your score significantly, limiting traditional borrowing options. Private lenders may still offer solutions.

5. What’s better for stopping wage garnishment: a HELOC or a second mortgage?

It depends on your needs. A HELOC offers flexibility if you want ongoing access to credit, while a second mortgage is ideal for paying off large debts immediately and stopping the garnishment at once.

Final Thoughts

Wage garnishment is stressful, but it doesn’t have to end your financial stability. For many Canadian homeowners, home equity represents the fastest path to relief. By using tools like a home equity loan, HELOC, or second mortgage, you can pay off judgments or CRA debts, stop income deductions, and regain full control of your finances.

If you’re facing wage garnishment or reduced income, contact LendToday.ca; a team that specializes in fast, reliable mortgage solutions for Canadian homeowners, even with bruised credit or income challenges.