The Negative Consequences If You Can’t Pay Property Taxes (And Smart Ways to Fix It)

If you’re falling behind on property taxes, you’re not alone. Budgets get squeezed by higher groceries, rising interest rates, job changes, separation, or unexpected bills. The problem is that property taxes are not like a typical bill you can ignore for a few months without consequences. Municipalities have powerful collection tools, and once arrears start piling up, the costs and stress can snowball.

This guide breaks down what usually happens when you can’t pay property taxes, what timelines often look like, and what you can do to get control before things escalate. It is written for homeowners, especially those with equity who may have options even if a bank has said no.

Why unpaid property taxes are a big deal

Property taxes fund essentials like schools, road maintenance, snow removal, fire services, and local infrastructure. Because the municipality relies on this revenue, they are typically quicker and more structured about collecting arrears than many other creditors.

Here’s the core issue: property taxes are tied to the home, not just to your personal credit profile. That means collection is anchored to the property itself, and enforcement can become serious if you fall too far behind.

1. You get late fees, interest, and penalties

The first consequence is usually financial, and it starts immediately. Municipalities commonly charge penalties and interest on unpaid balances. Even if the monthly amount seems manageable, these added costs can make the total feel like it is running away from you.

What this means in real life: the longer you wait, the harder it becomes to catch up with normal payments plus the growing arrears. This is why “I’ll handle it next month” can turn into “How did it get this high?”

Quick win

Call your municipality as soon as you know you’ll miss a payment. You may be able to arrange a plan, reduce escalation, and keep the situation from triggering enforcement steps.

2. Your account can be transferred to tax collection enforcement internally

After a period of missed payments, your property tax account usually shifts from routine billing to a more formal collections track within the municipality. That can mean more frequent notices, stricter deadlines, and less flexibility.

This stage is often still very fixable, but the tone changes. The municipality is documenting the situation and moving it toward formal recovery.

Quick win

Document everything: dates, amounts, who you spoke with, and what was agreed. If you set up a payment arrangement, ask for it in writing.

3. You may lose access to “nice to have” payment flexibility

Many homeowners rely on convenience to stay current, like installment plans, pre-authorized payments, or spreading bills across the year. When taxes go into arrears, municipalities may tighten those options until the balance is under control.

Even if your municipality allows a repayment plan, it often requires you to keep paying current taxes on schedule while also paying the arrears. This double-payment reality is where many homeowners get stuck.

Quick win

Ask about a structured arrears plan that aligns with your pay schedule. Some municipalities will work with you if you show consistent follow-through.

4. Your mortgage lender may get involved

A lot of homeowners do not realize this until it happens: if your lender is concerned that unpaid property taxes could threaten the property, they may step in. Depending on how your mortgage is set up, a lender may:

-

pay the taxes on your behalf to protect the property

-

add the amount to your mortgage balance or demand repayment

-

increase your monthly payment to collect taxes through the mortgage

-

treat ongoing tax arrears as a serious default risk

This can feel like the bank is “making it worse,” but from their perspective, they are protecting their collateral.

Quick win

If you’re behind, communicate before they discover it through other channels. A proactive plan often keeps things calmer.

5. Your credit and borrowing options can get harder

Unpaid property taxes do not always show up the same way a missed credit card payment does, but the ripple effect is real. If your lender pays the taxes and adjusts your mortgage, or if you fall behind on other bills while juggling tax arrears, your credit can take a hit.

Plus, even if your score is okay, arrears can make approval harder because lenders look at overall risk. Being behind on taxes can raise concerns about cash flow, budgeting strain, or broader financial instability.

Quick win

If you need to borrow to clear arrears, it is usually better to do it earlier, while your file is still stronger, instead of waiting until the situation forces a desperate solution.

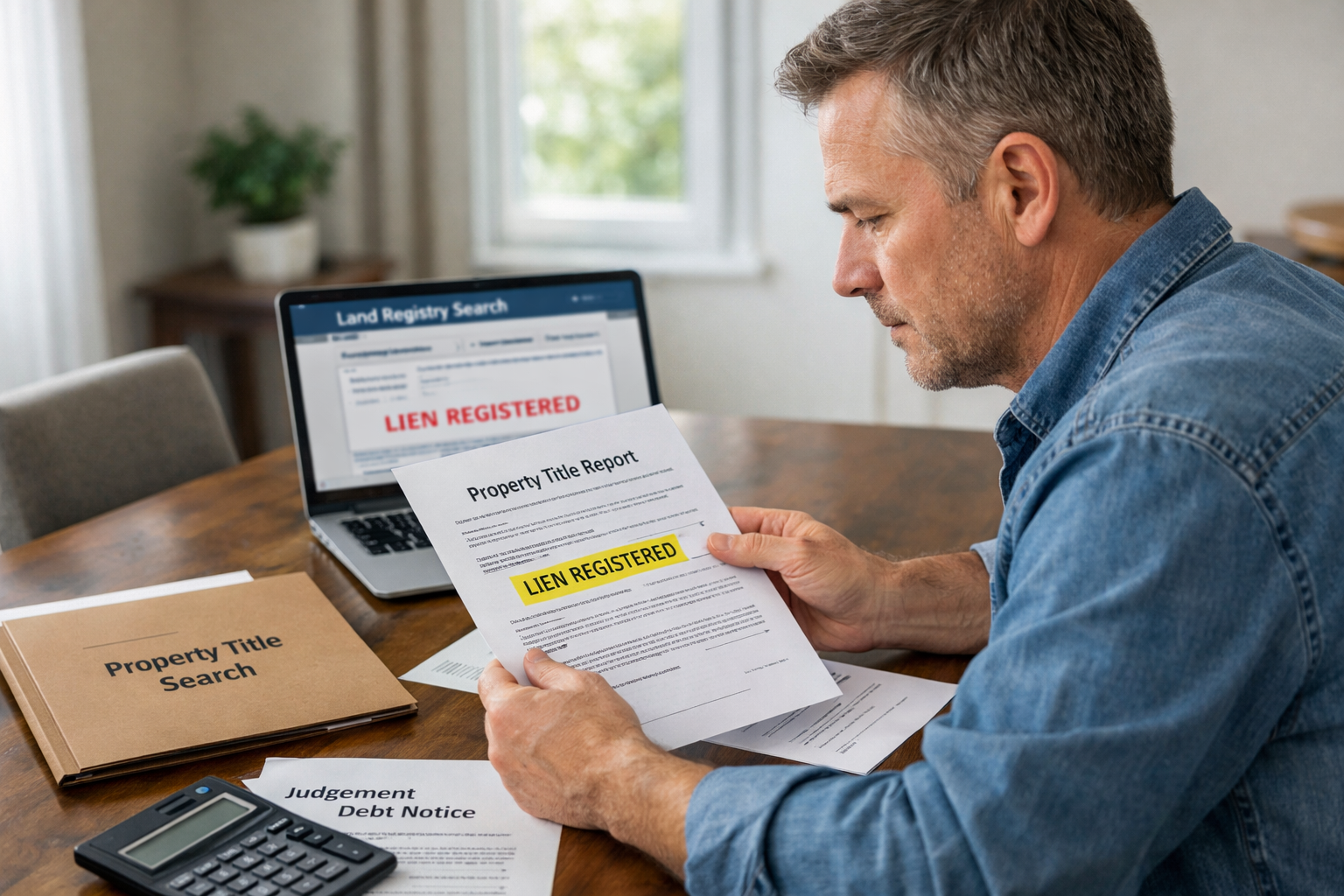

6. You can face a tax lien or tax registration actions

This is the point where things start sounding intimidating, and honestly, it should. Municipalities can take formal legal steps against the property when taxes remain unpaid long enough. The terminology varies by location, but the concept is similar: the municipality registers its claim tied to the property.

Once formal registration happens, it can complicate selling or refinancing because the arrears must be dealt with as part of any transaction. It also signals that the file is progressing toward more severe enforcement if unresolved.

Quick win

If you receive a formal notice (not just a routine bill), treat it as urgent. Waiting for “one more month” can be the difference between a manageable repayment plan and a legal escalation.

7. The most severe consequence: tax sale or forced sale process

If property taxes remain unpaid long enough, municipalities can begin a tax sale process (rules and timelines vary by province and municipality). The big idea is simple: the municipality wants to recover the money owed, and the home can become part of that recovery process.

This is not the same as a bank foreclosure, but the outcome can still be devastating if you ignore it. A tax sale process can lead to the property being sold to recover taxes, penalties, interest, and costs.

Here’s the painful part: homeowners often have equity, but they lose control of time and options once things escalate. The earlier you act, the more choices you keep.

Quick win

Do not wait for the “final notice” mindset. If you are even worried you might get there, that is your signal to explore solutions now.

Smart ways to fix property tax arrears

Let’s talk solutions. Most homeowners who fall behind are not irresponsible. They are overwhelmed. The goal is to choose the option that stabilizes your monthly cash flow while protecting your home and your equity.

Option A: Payment arrangement with the municipality

If the arrears are still relatively small, a payment plan is often the cleanest path. This works best when you can realistically handle:

-

ongoing current property taxes, plus

-

a monthly amount toward arrears

When it works, it keeps you out of legal escalation and preserves your borrowing profile.

Option B: Borrowing against home equity to pay taxes

If you have equity but your monthly budget is tight, using home equity can convert a high-pressure, fast-growing arrears situation into a predictable monthly payment.

Common ways homeowners do this include:

-

refinancing the first mortgage (if rates and qualification make sense)

-

a HELOC (home equity line of credit) if you qualify

-

a second mortgage if you need a faster approval or have bruised credit

-

alternative/private lending as a short-term bridge while you stabilize

This is where a mortgage broker can be useful: not just to find a lender, but to structure something that solves the immediate crisis without trapping you in an unmanageable payment.

When this option makes sense

-

You have significant equity

-

You are behind due to short-term disruption (job change, illness, separation)

-

You can afford a consolidated payment better than the arrears pressure

-

You want to stop escalation quickly

Option C: Cut expenses and prioritize the highest-risk items

If borrowing is not ideal, you still need a triage plan. In many cases, property taxes sit in the “must pay” category alongside mortgage and utilities.

Practical moves:

-

reduce discretionary spending for 60 to 90 days

-

pause extra debt payments temporarily (only where safe to do so)

-

sell unused assets

-

negotiate temporary relief on other bills to free cash for taxes

This is not fun, but it can stop the spiral.

Option D: Sell the property strategically, before you lose leverage

Sometimes the right answer is selling, especially if:

-

the home is unaffordable long-term

-

arrears are growing faster than your income can recover

-

you have strong equity and can downsize or rent with breathing room

Selling early protects your equity and gives you control of the timeline, which usually means a better outcome than being forced into a rushed process.

How to decide what to do next

If you are unsure where you fit, use this quick decision guide:

-

Arrears are small and income is stable: start with a municipal payment plan

-

Arrears are growing and cash flow is tight but you have equity: explore refinancing, HELOC, or a second mortgage

-

Credit is bruised or bank said no: look at alternative lending with a clear exit plan

-

Income is uncertain long-term: consider selling before enforcement limits your choices

The most important thing is speed. Not panic. Just speed.

FAQ: What happens if I can’t pay property taxes?

Can the city take my house for unpaid property taxes?

Municipalities can take enforcement steps that may eventually lead to a tax sale process if arrears remain unpaid long enough. The exact rules and timelines depend on your province and municipality.

How long can you go without paying property taxes?

It varies by location. Most municipalities apply penalties and interest quickly, then move toward more formal notices and enforcement if arrears persist.

Will unpaid property taxes affect my mortgage?

They can. In some cases, your lender may pay the taxes to protect the property and then collect the amount from you, or adjust your mortgage payment structure.

Can I refinance to pay property tax arrears?

Yes, many homeowners use refinancing, a HELOC, or a second mortgage to clear arrears, especially when they have equity but need cash flow relief.

What if my credit is bad and I’m behind on taxes?

You may still have options through alternative or private lending if you have sufficient equity. The key is making sure the payment is manageable and having a plan to transition to a better option later.

Should I set up a payment plan with the municipality or borrow?

If you can handle current taxes plus arrears payments, a municipal plan is often the simplest. If the double payment is too heavy, borrowing against equity can create one predictable payment and stop escalation.

Can unpaid property taxes stop me from selling my home?

You can usually still sell, but arrears typically must be paid out as part of the closing. If enforcement has escalated, it can add urgency and complexity.

Closing thought

If you can’t pay property taxes, the worst move is silence. The best move is getting a plan in place while you still have choices. Whether that is a municipal payment plan, using home equity to clear the balance, or selling strategically, acting early protects your home and your equity.