As we enter 2026, the Canadian mortgage landscape is undergoing its most significant transformation in a generation. After years of navigating the “higher-for-longer” interest rate environment and a cooling housing market, the dust is finally settling.

For the millions of Canadians who have been watching the Bank of Canada (BoC) with bated breath, 2026 represents a shift toward a “new normal.” While the rock-bottom rates of the pandemic are a distant memory, a new era of stability, technological integration, and expanded borrowing options is emerging.

In this comprehensive guide, we explore the seven positive trends shaping the Canadian mortgage industry in 2026.

1. The Bank of Canada’s “Landing Zone”: Stability at 2.25%

The headline story for 2026 is the end of interest rate volatility. After the aggressive hiking cycle of 2022-2023 and the subsequent easing in 2024-2025, the Bank of Canada has signaled a prolonged “pause” at its current policy rate of 2.25%.

For Canadian homeowners and buyers, this is the best-case scenario. It provides a predictable floor for 5-year fixed mortgage rates, which are currently hovering in the 4.4% to 4.9% range. This stability allows buyers to plan their finances without the fear of a sudden “rate shock” and has significantly reduced the stress-test barrier for many households.

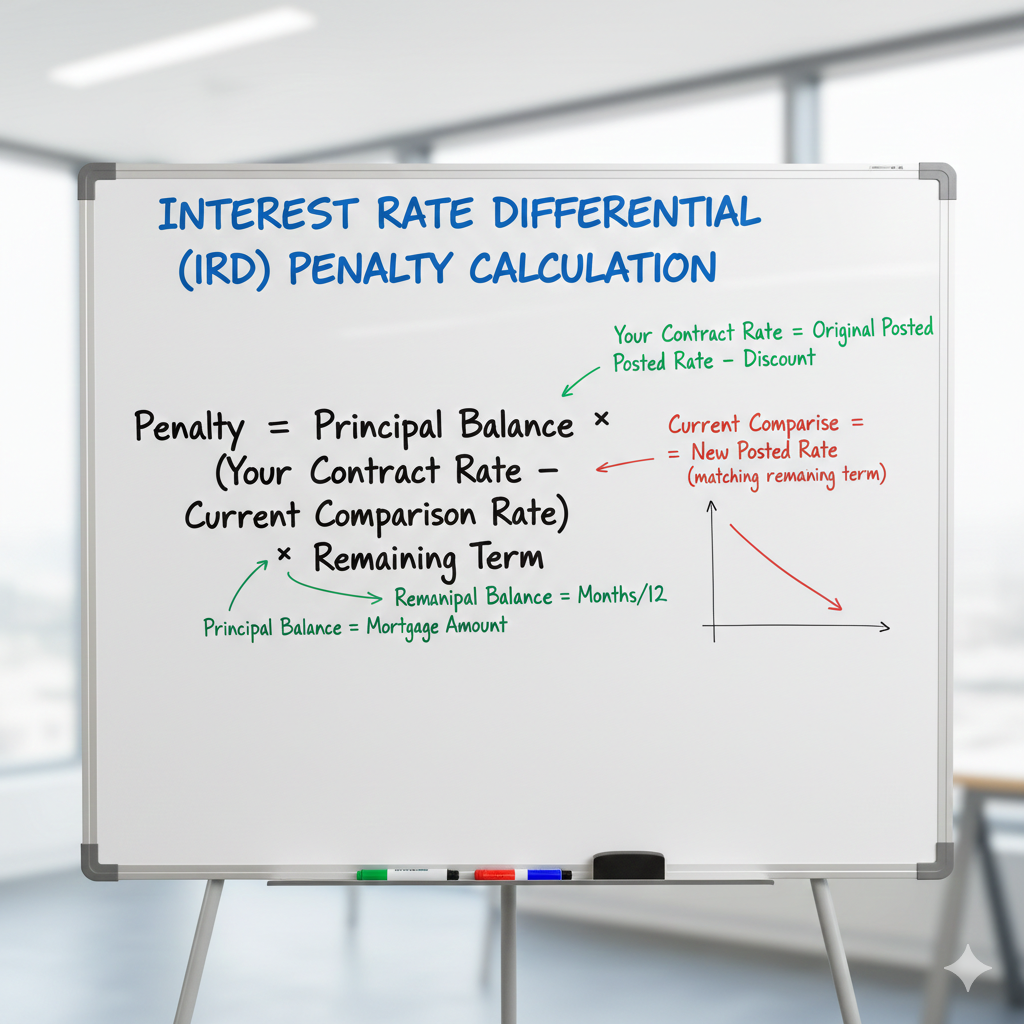

2. Navigating the “Renewal Wave” with Confidence

Between 2025 and 2026, approximately 60% of all Canadian mortgages are set to renew. Many of these borrowers are coming off 2021 contracts where rates were as low as 1.8%. While a “payment shock” of 15-20% is real for some, the outlook is more positive than initially feared.

Thanks to strong wage growth over the last five years and the proactive use of lump-sum payments, the “renewal cliff” is looking more like a “renewal hill.” Canadian lenders have become increasingly flexible, offering specialized renewal products and shorter terms (such as 2 or 3 years) to help homeowners bridge the gap until the next economic cycle.

3. The 30-Year Amortization Advantage for First-Time Buyers

A major policy shift that is reaching full maturity in 2026 is the expansion of 30-year amortizations. Initially introduced for first-time buyers of new builds and later expanded, this rule change has been a game-changer for affordability.

By extending the amortization from 25 to 30 years, monthly payments are reduced by roughly 8-10%, making it easier for young Canadians to pass the OSFI stress test. In 2026, we are seeing a surge in “missing middle” housing—townhomes and semi-detached properties—specifically designed to fit these new mortgage parameters.

4. The OSFI “Pure Rental” Shift: Good News for Homeowners

Effective January 2026, the Office of the Superintendent of Financial Institutions (OSFI) has implemented stricter rules for “income-producing residential real estate” (IPRRE). While this makes it harder for mega-investors to “double-count” rental income to buy dozens of units, it has a hidden benefit for the average Canadian.

With fewer speculative investors competing for entry-level condos and townhomes, first-time homebuyers are finding more inventory and less “blind bidding.” The 2026 market is no longer a “frenzy”; it is a balanced environment where buyers can actually include a home inspection condition.

5. Open Banking and AI: The 48-Hour Approval

2026 marks the year that Open Banking has truly arrived in Canada. Gone are the days of hunting for paper T4s and bank statements. Under new federal frameworks, borrowers can now securely share their financial data with lenders via API.

When combined with AI-driven underwriting, the Canadian mortgage process has been slashed from weeks to days. Many digital-first lenders now provide binding mortgage commitments in under 48 hours. This speed is particularly vital in 2026’s balanced market, where being “finance-ready” can still be the deciding factor in a successful offer.

6. The Rise of “Multi-Generational” Mortgage Products

In response to Canada’s housing supply challenges, 2026 has seen a boom in multi-generational mortgages. With the federal “Multigenerational Home Renovation Tax Credit” fully active, more Canadians are adding garden suites or secondary suites to their properties.

Lenders have responded with products that allow families to co-sign mortgages while factoring in the potential rental income from an Accessory Dwelling Unit (ADU). This trend is helping to solve the affordability crisis from the inside out, allowing families to pool equity and live together while maintaining privacy.

7. The “Green” Mortgage Rebate Momentum

Sustainability is no longer a “nice-to-have” in Canadian lending. In 2026, CMHC (Canada Mortgage and Housing Corporation) has expanded its “Eco Plus” programs. Borrowers purchasing energy-efficient homes or committing to retrofits can receive partial premium refunds of up to 25%.

These “Green Mortgages” are often paired with lower interest rates from Canada’s Big Six banks, as energy-efficient homes are statistically proven to have lower default rates. For a homeowner in 2026, “going green” is a savvy financial strategy that pays off in both monthly utility savings and mortgage discounts.

Canada Mortgage Market Comparison: 2024 vs. 2026

| Feature | 2024 (Averages) | 2026 (Projections) |

| BoC Overnight Rate | 5.00% | 2.25% |

| 5-Year Fixed Rate | 5.2% – 6.0% | 4.4% – 4.9% |

| Standard Amortization | 25 Years | 30 Years (For Qualified Buyers) |

| Approval Method | Manual/Document Heavy | Open Banking/AI-Integrated |

| Market Sentiment | High Anxiety | Stabilized / Balanced |

Action Plan for Canadian Borrowers in 2026

If your mortgage is up for renewal this year, or if you’re looking to buy, follow these three steps:

-

Start Your Renewal Strategy 6 Months Out: Don’t wait for your bank’s letter. In 2026, competition for renewals is fierce. Shop around at the 180-day mark to lock in a rate.

-

Evaluate the “Short-Term Fixed” Option: Many Canadians are opting for 2 or 3-year fixed terms in 2026, betting that rates may soften even further by 2028-2029.

-

Leverage New ADU Rules: If you’re buying a home, look for properties with “suite potential.” The ability to use rental income to qualify for your mortgage is easier under 2026’s “house hacking” friendly regulations.

Conclusion: A New Chapter for Canadian Real Estate

The Canadian mortgage industry for 2026 is defined by a return to fundamentals. We have moved past the era of “easy money” and the era of “interest rate panic.” What remains is a market that is more tech-savvy, more accessible to first-time buyers thanks to amortization changes, and significantly more stable.

While challenges remain—particularly in high-cost hubs like Toronto and Vancouver—the systemic shifts we see today suggest a healthier, more sustainable housing future for all Canadians.

Frequently Asked Questions (FAQ)

1. Will mortgage rates go down further in 2026?

Most economists believe the Bank of Canada has reached its “neutral rate” of 2.25%. While minor fluctuations are possible depending on inflation, the significant rate-cut cycle of 2024-2025 has concluded. Stability is the theme for 2026.

2. How much will my mortgage payment increase at renewal in 2026?

If you are renewing a 5-year fixed rate from 2021 (when rates were ~2%), you can expect a monthly payment increase of roughly 15% to 20%. However, if you have been making accelerated payments, your actual “shock” may be significantly lower.

3. Can I get a 30-year mortgage in Canada now?

Yes, as of late 2024 and through 2026, 30-year amortizations are available for first-time homebuyers and those purchasing newly constructed homes. This is designed to lower monthly payments and improve accessibility.

4. What is “Open Banking” and how does it help my mortgage?

Open Banking allows you to give your lender “read-only” access to your financial data. In 2026, this eliminates the need to provide physical pay stubs or bank statements, leading to faster approvals and more accurate rate offers based on your actual spending habits.

5. Are condo prices still dropping in 2026?

In major centers like Toronto and Vancouver, the condo market remains “soft” due to a high volume of new completions and stricter rules for investors. This has created a buyer’s market for condos, making 2026 an excellent entry point for those previously priced out of the city.

- The Empty Nester’s Guide (2026): Should You Downsize or Use a Reverse Mortgage to Age in Place? - February 28, 2026

- Can a Mortgage Company Evict You in Ontario? (2026 Power of Sale Guide) - February 23, 2026

- Crucial Ways to Survive the Redemption Period During Foreclosure: A Guide - February 21, 2026