If you’re applying for a mortgage in Canada, you need home insurance before closing day. This isn’t optional. Every mortgage lender requires proof of adequate home insurance with the lender listed as a loss payee on the policy. Without an insurance binder showing proper coverage, your mortgage closing will be delayed or cancelled. Home insurance protects both you and the lender from financial loss due to property damage, fire, liability claims, and other risks. Whether you’re completing a home purchase, refinance, or home equity loan, understanding these insurance requirements ensures a smooth mortgage process and protects your investment for years to come.

Why Mortgage Lenders Require Home Insurance

When you take out a mortgage, you’re borrowing a significant amount of money with your home serving as collateral. The lender needs protection for this investment.

Protecting the Lender’s Investment

Your mortgage lender has hundreds of thousands of dollars at risk. If your home is destroyed by fire, severe weather, or another covered event, the lender could lose their entire investment without proper home insurance in place.

Key takeaway: Insurance ensures the lender can recover their money even if a catastrophe strikes. According to industry data, the average home insurance claim in Canada can range quite broadly depending on the type of repairs involved. However, total loss claims for fire or severe weather can reach the full replacement value of the home, potentially exceeding the outstanding mortgage balance.

The loss payee designation on your home insurance policy ensures claim proceeds go directly to the mortgage lender first. This protects their financial interest before you receive any remaining funds. This arrangement continues until you pay off the mortgage completely.

Legal and Regulatory Requirements

Important to note: Canadian banking regulations and mortgage lending standards mandate home insurance for all mortgaged properties. This isn’t just a lender preference but a requirement rooted in sound lending practices and legal protection.

The Canada Mortgage and Housing Corporation (CMHC) specifically requires adequate home insurance for all CMHC-insured mortgages. Even for conventional mortgages where CMHC insurance isn’t required, private lenders universally enforce the same home insurance standards.

Provincial regulations may have slight variations, but the fundamental requirement remains consistent across Canada. Every mortgage contract you sign will include specific clauses about maintaining continuous home insurance coverage throughout the loan term.

What Is a Home Insurance Binder and Why Do You Need One?

Understanding the insurance binder is essential for mortgage closing preparation.

Understanding the Insurance Binder

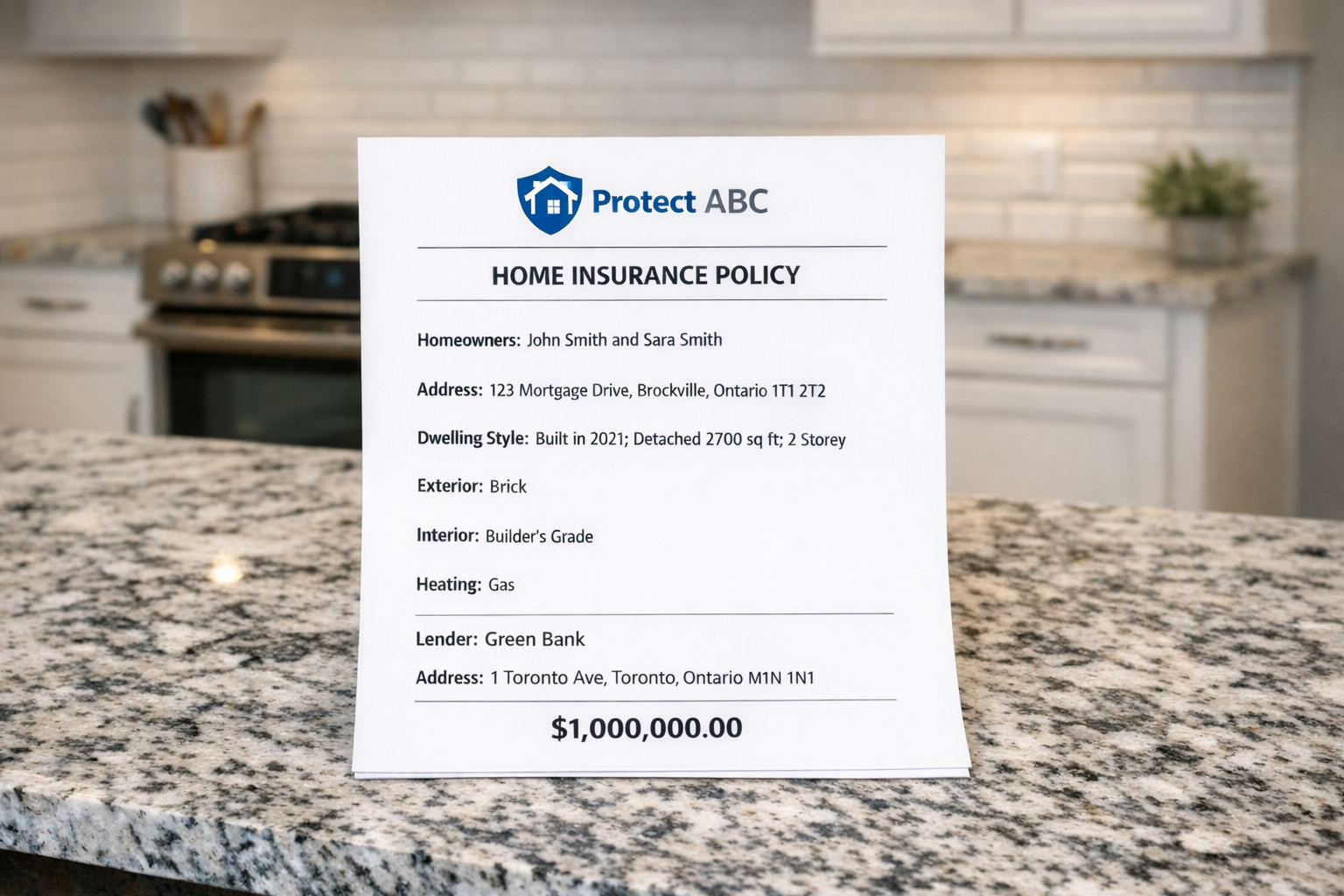

An insurance binder is a temporary document proving you have home insurance coverage. Insurance companies issue binders before the complete policy documents are finalized and delivered.

Your mortgage lender requires this binder at closing to verify coverage is in place. The binder includes essential information: the property address, coverage amounts, effective date, policy number, and critically, the lender’s name as loss payee.

Common mistake: Many homebuyers wait until the week of closing to arrange home insurance. This creates unnecessary stress and can delay closing if the insurance company can’t issue a binder quickly enough. Insurance binders are typically valid for 30 to 60 days, giving you time to finalize the full policy after closing.

Loss Payee vs. Mortgagee Clause

Important to note: These terms are often used interchangeably, but they have specific legal meanings. Understanding the distinction helps you communicate properly with your insurance provider.

A loss payee is a party with a financial interest in the insured property who receives claim payment before the property owner. Your mortgage lender is named as the loss payee, meaning they have first claim to insurance proceeds up to the mortgage balance.

The mortgagee clause is the specific policy language that establishes this relationship. It protects the lender even if you violate policy terms or allow coverage to lapse.

Key takeaway: When a claim occurs, the insurance company writes the check to both you and the mortgage lender. The lender must endorse the check before repairs can proceed, ensuring their collateral is properly restored.

Essential Home Insurance Coverage for Mortgage Approval

Not all home insurance policies meet mortgage lender requirements. Specific coverage minimums must be met.

Dwelling Coverage Requirements

Dwelling coverage insures the physical structure of your home, including built-in appliances, fixtures, and attached structures like garages. This is the most critical coverage for mortgage approval.

Lenders typically require dwelling coverage equal to or exceeding the mortgage loan amount. However, this creates a potential problem. Your home’s market value and replacement cost are often different numbers.

Canadian example: A home purchased for $500,000 might require $600,000 in dwelling coverage because construction costs exceed market value in your area. Conversely, a $700,000 home in a high-demand neighbourhood might only need $450,000 to rebuild.

Common mistake: Basing dwelling coverage on purchase price rather than replacement cost. Your insurance company will assess the true cost to rebuild your home using current construction costs in your region. This is the coverage amount your policy should reflect. Most mortgage lenders accept this professional assessment even if it’s below the loan amount, provided it represents full replacement cost.

Liability Coverage Minimums

Liability coverage protects you if someone is injured on your property or if you’re found legally responsible for damage to others. Most Canadian mortgage lenders require minimum liability coverage of $1 million to $2 million.

This coverage protects both you and the lender. If a major liability claim depletes your personal finances, you might struggle with mortgage payments. Adequate liability coverage prevents this scenario.

The coverage pays for legal defence costs and settlements or judgments against you. Given that Canadian liability awards can reach millions of dollars in severe injury cases, this protection is essential.

Key takeaway: Liability coverage is usually inexpensive to increase. The cost difference between $1 million and $2 million in coverage is often just $20 to $40 annually, making higher limits a smart choice.

Additional Coverage Considerations

Beyond basic dwelling and liability coverage, several additional protections affect mortgage lending:

Personal property coverage insures your belongings but isn’t typically required by mortgage lenders since it doesn’t protect their collateral. However, comprehensive home insurance should include it for your own protection.

Additional living expenses coverage pays for hotel, food, and other costs if you must live elsewhere during repairs. While not strictly required for the mortgage, most lenders expect this as part of a standard homeowner’s insurance policy.

Important to note: Water damage coverage, including sewer backup and overland flooding, has become increasingly important in Canada. Standard policies may exclude these perils. Your lender may require proof of water coverage, especially in flood-prone areas. Many insurance companies now offer or require overland flood coverage as climate-related water damage becomes more common.

Home Insurance Requirements for Different Mortgage Scenarios

Insurance needs vary depending on your mortgage transaction type.

Home Purchase Insurance Needs

When buying a home, you must provide an insurance binder to your lawyer before closing. The coverage must be effective on your possession date, not your closing date, since these can differ.

Your real estate lawyer will review the binder to confirm adequate coverage and proper loss payee designation. Without this documentation, the lender will not release mortgage funds and your purchase cannot be completed.

Plan to have your home insurance arranged at least one week before closing. This timeline allows for any last-minute corrections to the binder if information is incorrect.

Refinance Insurance Requirements

When refinancing your home, your existing home insurance policy continues, but the loss payee must change. Your new mortgage lender must replace the previous lender on your policy.

Contact your insurance company as soon as your refinance is approved. Provide the new lender’s name, address, and loan number. The insurance company will issue an updated declaration page or binder showing the change.

Common mistake: Homeowners forget to update their insurance company about the refinance. The old lender remains listed as loss payee, which can complicate future claims. Your new lender may also require proof that they’re properly listed before finalizing the refinance.

If you’re increasing your loan amount through a refinance, verify that your dwelling coverage still meets the lender’s requirements. You may need to increase coverage limits.

Home Equity Loan Coverage

Home equity loans and home equity lines of credit (HELOCs) can create a second lien against your property. The home equity lender will also require loss payee status on your home insurance policy.

Your insurance policy can list multiple loss payees. In a claim situation, both lenders receive payment according to their lien position. The first mortgage holder has priority, with remaining funds going to the home equity lender.

Adequate dwelling coverage becomes even more important with a home equity loan since total debt against the property increases. Ensure your coverage reflects the combined loan amounts or full replacement cost, whichever is appropriate.

The Fire Insurance Policy and Mortgage Lending

You may see references to “fire insurance policy” in mortgage documents. This is historical terminology.

Important to note: When lenders mention fire insurance policy, they mean comprehensive home insurance. Fire coverage is just one component of modern homeowner’s insurance policies.

Decades ago, fire insurance was sold separately from other property coverage. Today’s home insurance bundles fire, wind, hail, theft, vandalism, liability, and numerous other protections into a single policy.

The term persists in legal documents and mortgage contracts, but no lender accepts only fire coverage. They require full home insurance protecting against all standard perils.

Common myth: Some homebuyers believe they only need fire insurance because that’s what mortgage documents mention. This is incorrect and will prevent mortgage approval. Standard comprehensive home insurance includes fire coverage plus much more, satisfying all lender requirements.

How to Get Home Insurance Before Closing

Proper planning ensures a smooth mortgage closing.

Timeline for Obtaining Coverage

Start shopping for home insurance approximately 30 days before your planned closing date. This gives ample time to compare quotes, select coverage, and obtain the required binder.

Get quotes from at least three insurance providers. Rates vary significantly between companies, and coverage terms differ as well. Focus on reputable insurers with strong financial ratings and good claims service reputations.

Request your insurance binder at least one week before closing. While many companies can issue binders within 24 to 48 hours, unexpected delays happen. Early preparation prevents last-minute panic.

Key takeaway: According to industry estimates, approximately 15% of mortgage closing delays relate to insurance issues. Most of these are preventable through earlier action.

Coordinate the coverage effective date with your possession date. The home insurance must be active when you take ownership, even if that’s before the formal closing date in some transactions.

Working With Insurance Providers

Your insurance company needs specific information to quote accurately and issue a binder:

Property details, including age, square footage, construction type, roofing material, heating system, and any recent renovations, affect pricing and coverage. Be prepared to provide this information, which is usually available in the home inspection report or property listing.

Disclose your mortgage lender’s information, including the exact legal name, mailing address, and loan number once available. Accuracy is critical since the loss payee designation must match the lender’s records exactly.

Request a binder naming the lender as the loss payee specifically. Standard proof of insurance letters don’t include this designation and won’t satisfy mortgage requirements.

Confirm the coverage start date matches your possession date. Your insurance company can backdate coverage if needed, but it’s simpler to set the correct date initially.

Keep proof of payment for your initial premium. Some lenders want confirmation the insurance is paid, not just in place.

What Happens If You Don’t Maintain Home Insurance?

Maintaining continuous home insurance throughout your mortgage term is mandatory, not optional.

Important to note: Allowing home insurance to lapse or cancel is a mortgage default. Your mortgage contract specifically requires continuous coverage, and violation of this term has serious consequences.

If your insurance lapses, the mortgage lender receives notification directly from the insurance company in most cases. Lenders also conduct periodic insurance checks on their mortgage portfolios.

When lapse is discovered, the lender will typically give you 10 to 30 days to reinstate coverage or obtain new home insurance. If you don’t comply, the lender can purchase force-placed insurance and add the cost to your mortgage balance.

Force-placed insurance is extremely expensive, typically costing two to three times normal home insurance premiums. It covers only the dwelling to protect the lender’s collateral. Your personal belongings, liability, and additional living expenses receive no coverage.

Continued failure to maintain proper home insurance can ultimately lead to mortgage default proceedings and potential foreclosure. Lenders take this requirement very seriously because their collateral protection depends entirely on active coverage.

Key takeaway: Set up automatic premium payments or calendar reminders for policy renewals. Continuous coverage protects you and keeps your mortgage in good standing.

Common Mistakes and How to Avoid Them

Learning from others’ errors saves time, money, and stress.

Common mistake #1: Cancelling existing home insurance before the new mortgage closes. If you currently own a home and are buying a new one, maintain insurance on both properties until the sale and purchase are complete. Gaps in coverage can delay or prevent closing.

Common mistake #2: Insufficient dwelling coverage based on purchase price rather than replacement cost. Work with your insurance company to determine accurate rebuilding costs. Don’t assume purchase price equals appropriate coverage.

Common mistake #3: Not updating the loss payee after refinance or mortgage transfer. When your mortgage changes hands, update your home insurance immediately. Many mortgages are sold to other lenders after closing, requiring policy updates each time.

Common mistake #4: Allowing coverage to lapse due to payment issues or policy non-renewal. Set up automatic payments and monitor renewal notices carefully. Insurance companies must provide advance notice of cancellation or non-renewal, giving you time to act.

Key takeaway: Maintain open communication between your insurance provider and mortgage lender. Proactive management of your home insurance prevents problems before they affect your mortgage or financial security.

Frequently Asked Questions

Q: How much home insurance do I need for a mortgage in Canada?

A: Most Canadian mortgage lenders require dwelling coverage equal to the replacement cost of your home or the mortgage loan amount, whichever is greater. However, replacement cost is the more important number. Your insurance company will calculate the cost to rebuild your home using current construction costs in your area. Even if this amount is less than your mortgage, lenders typically accept it if it represents full replacement coverage.

Liability coverage minimums usually range from $1 million to $2 million, depending on the lender. Additional coverage, like personal property and additional living expenses are standard in comprehensive home insurance policies, but isn’t specifically mandated amounts. Work with your insurance provider to ensure your policy meets both lender requirements and your personal protection needs.

Q: Can I use the same home insurance when I refinance my mortgage?

A: Yes, you can and should maintain your existing home insurance when refinancing. You don’t need a new policy. However, you must update the loss payee designation on your current policy to show the new mortgage details instead of the old ones.

Contact your insurance company as soon as your refinance is approved. Provide your new lender’s information and request an updated declaration page or binder showing the change. If you’re borrowing more money through the refinance, verify your coverage limits still meet lender requirements. You may need to increase dwelling coverage if your loan amount has grown significantly.

Q: What is the difference between a loss payee and an additional insured?

A: A loss payee has a financial interest in the insured property and receives claim payments before the property owner. Your mortgage lender is listed as the loss payee, meaning insurance claim proceeds are paid to both you and the lender jointly. This protects the lender’s collateral investment.

An additional insured is a party protected by the liability portion of the policy. This designation is more common in commercial insurance. For residential mortgages, lenders typically require loss payee status, rather than additional insured status. The loss payee designation ensures the lender can recover their investment if the property is damaged or destroyed.

Q: When should I get home insurance when buying a house?

A: Start shopping for home insurance 30 days before your scheduled closing date. This allows time to compare quotes, select the best coverage, and address any issues. Request your insurance binder at least one week before closing to prevent last-minute delays.

Your home insurance must be effective on your possession date. Coordinate this timing with your insurance provider when setting up the policy. You cannot close on your mortgage without proof of insurance, so early preparation is essential. Many Canadian homebuyers underestimate how important this timeline is and face unnecessary stress by waiting too long.

Q: What happens if my home insurance claim is less than my mortgage balance?

A: If you file a home insurance claim, the insurance company issues payment jointly to you and your mortgage lender as loss payee. The lender reviews the claim and determines how funds will be released.

For small claims where repair costs are well below the mortgage balance, many lenders allow you to receive the funds directly after you complete repairs and provide proof. For larger claims, especially those involving major structural damage, the lender typically holds the claim proceeds in escrow. They release funds in stages as repairs progress, ensuring their collateral is properly restored.

If your home is a total loss and the insurance payout is less than your mortgage balance, you remain responsible for the difference. This is why adequate dwelling coverage equal to replacement cost is so important. Underinsurance creates financial hardship in total loss situations.

Q: Does home insurance go into my mortgage payment?

A: No, home insurance premiums are not included in your mortgage payment in Canada. Unlike property taxes, which some lenders collect monthly, home insurance is handled separately and paid directly to your insurance company.

You are responsible for arranging your own home insurance through a third-party insurance provider and making premium payments independently from your mortgage. Most insurance companies offer flexible payment options, including annual, semi-annual, or monthly payment plans that you manage yourself.

While your mortgage lender requires proof of continuous coverage, they do not collect, hold, or pay your insurance premiums on your behalf. You must provide annual proof of renewal and payment to your lender to confirm your home insurance remains active. This gives you direct control over your insurance relationship but also means you bear full responsibility for ensuring timely payment and avoiding coverage gaps that could put your mortgage in default.

Conclusion

Home insurance is not optional when you have a mortgage in Canada. Every lender requires adequate coverage with a proper loss payee designation protecting their investment in your property. Whether you’re completing a home purchase, refinance, or home equity loan, understanding these requirements ensures smooth mortgage processing and protects your largest financial asset.

Start your insurance search early, obtain proper dwelling and liability coverage, and maintain continuous protection throughout your mortgage term. The fire insurance policy terminology in mortgage documents refers to comprehensive home insurance covering all standard perils. Work closely with reputable insurance providers who understand mortgage requirements and can issue the necessary binder for closing.

At LendToday.ca, we help Canadian borrowers navigate every aspect of the mortgage process, including home insurance requirements. Proper preparation and understanding of these protection requirements creates confidence in your home financing journey and security for your future.

- Home Insurance Requirements for a Mortgage in Canada - February 13, 2026

- Assignment of Rents in a Mortgage: What You Need to Know - February 9, 2026

- Mortgage Without Tax Returns Explained: Helpful Canadian Options - January 20, 2026