Painful Realities of the Interest Rate Differential Penalty You Must Know

The Great Penalty Divide: Fixed vs. Variable

Before diving into the IRD, it is essential to understand that this penalty is almost exclusively a “Fixed Rate” problem. If you have a variable-rate mortgage, your penalty is typically capped at three months of interest. However, if you have a closed fixed-rate mortgage, your lender will charge you the greater of:

-

Three months of interest.

-

The Interest Rate Differential (IRD).

In a declining rate environment, the IRD is almost always the higher number—and it isn’t even close.

What Exactly is the Interest Rate Differential (IRD)?

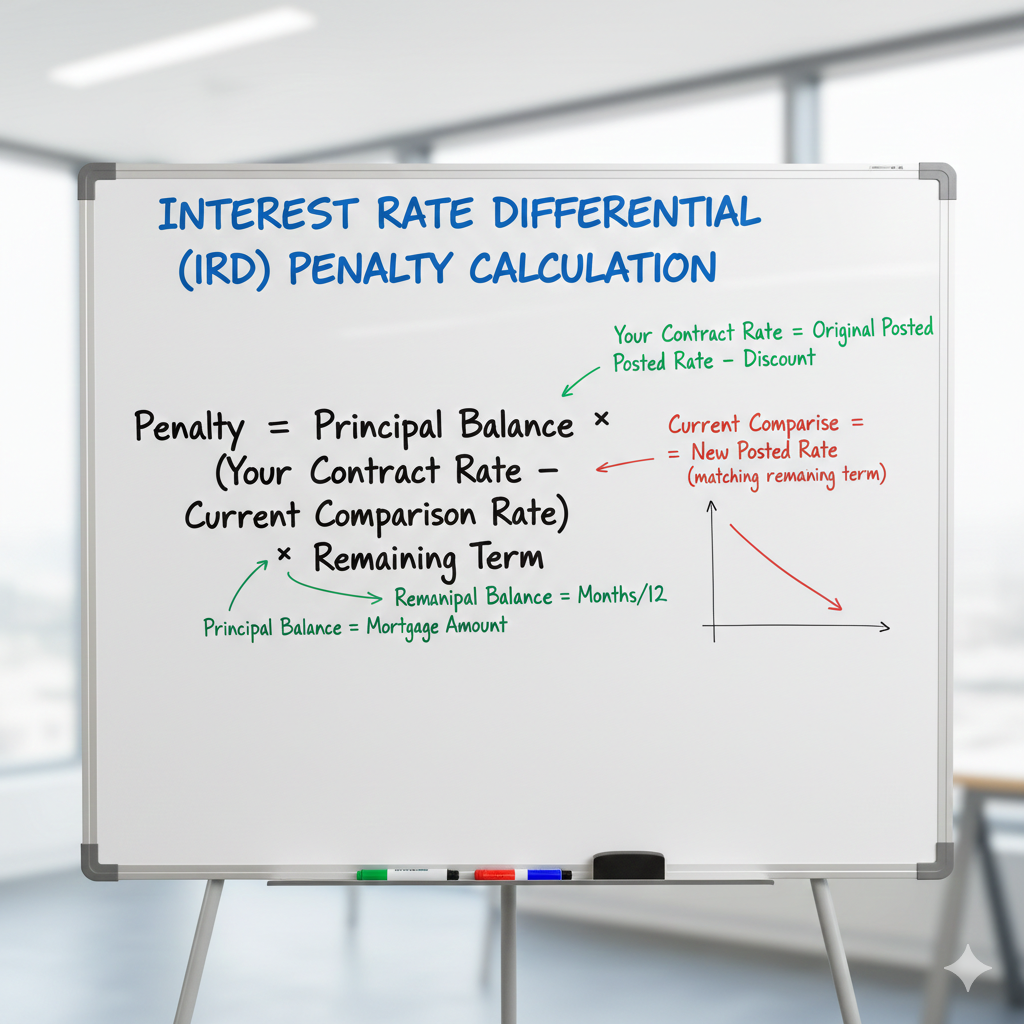

The IRD is a calculation used by lenders to compensate themselves for the interest they lose when you pay off your mortgage before the term is up. If you locked in a rate of 5% two years ago, and current rates for your remaining term are now 3%, the bank is “losing” that 2% spread if you leave. The IRD is their way of making sure they get that money anyway.

The “Posted Rate” Trap: Why Your Penalty is Higher Than You Think

This is where many Ontario homeowners feel the sting. Most “Big Five” banks do not calculate the IRD based on the discounted rate you actually pay. Instead, they use a “Posted Rate” and apply a “Discount” to the calculation.

The basic formula looks like this:

If a homeowner has a $500,000 balance (B), a 4.5% interest rate (R), and the current market rate for their remaining 2 years (T) is 3.0% (R):

In this scenario, the homeowner would owe $15,000 to break the mortgage.

However, banks often use the Posted Rate from when you signed minus the Current Posted Rate for a term that matches your remaining time. This mathematical sleight of hand can double or triple the penalty compared to what a fair-market lender might charge.

Step-by-Step Breakdown: Calculating the Cost

Let’s look at a hypothetical scenario for a homeowner in Ontario:

-

Current Balance: $500,000

-

Your Rate: 4.5%

-

Remaining Term: 3 years (36 months)

-

Current Bank Rate for a 3-year term: 3.0%

-

The Spread: 1.5%

In this simplified example, the annual loss to the bank is 1.5% of $500,000, which is $7,500. Multiply that by the 3 years remaining, and your IRD penalty is $22,500. Compare that to a 3-month interest penalty, which would only be roughly $5,625.

Why Do Lenders Charge This?

Lenders fund fixed-rate mortgages by matching them against bonds. When you break your contract, they are stuck with high-interest obligations but can only re-lend your money at today’s lower rates. The IRD protects their profit margin. While it makes sense from a corporate accounting perspective, it can be devastating for a family trying to refinance to save money.

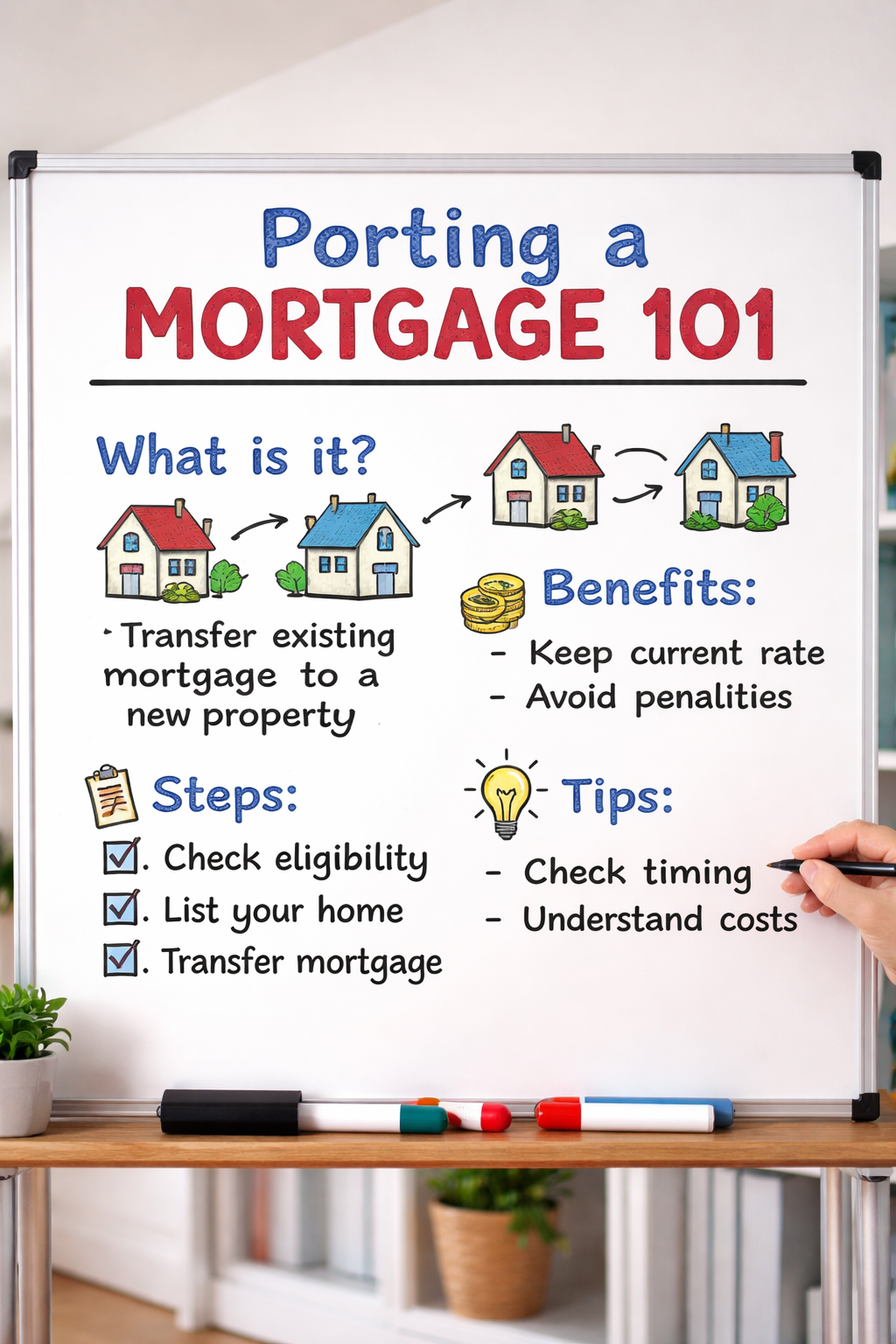

Strategic Ways to Avoid or Reduce the IRD

-

Porting Your Mortgage: If you are selling your home and buying a new one, you can often “port” your existing rate and terms to the new property, avoiding the penalty entirely.

-

The 15% or 20% Prepayment Trick: Most mortgages allow you to pay down a percentage of the principal annually without penalty. Before requesting a payout statement, apply your maximum allowable prepayment. This reduces the principal balance that the IRD is calculated against.

-

The “Date of Discharge” Timing: If you are close to the end of your term (within 3-6 months), it may be cheaper to wait or look for a lender that offers a “switch” program where they cover a portion of the costs.

-

Blended Rates: Instead of breaking the mortgage, ask for a “blend and extend.” This mixes your old high rate with a new lower rate, usually without a massive upfront penalty.

When Does Paying the Penalty Actually Make Sense?

It sounds counterintuitive to pay $20,000 to save money, but sometimes the math works. If breaking your mortgage allows you to:

-

Consolidate $50,000 in credit card debt at 22% into a mortgage at 4%.

-

Lower your monthly payment by enough to break even on the penalty within 18–24 months.

-

Access equity for a high-return investment or necessary home renovation.

In these cases, the IRD isn’t just a fee—it’s an investment in your future cash flow.

Frequently Asked Questions (FAQ)

Q: Can I negotiate my IRD penalty with the bank?

A: Generally, no. The penalty is baked into the standard charge terms you signed. However, you can sometimes negotiate a “waiver” if you are staying with the same lender for a larger, more expensive mortgage.

Q: Does every lender use the same IRD calculation?

A: Absolutely not. This is a major point of difference. Credit unions and “monoline” lenders often use much fairer IRD calculations than the major big banks because they don’t rely on inflated “posted rates.”

Q: Is the IRD tax-deductible?

A: In Canada, if the mortgage is for an investment property, the penalty paid to break a mortgage may be deductible as a cost of financing. Always consult a tax professional.

Q: How do I get an accurate quote for my penalty?

A: You must call your lender and ask for a “Payout Statement.” Be aware that this quote is usually only valid for 30 days, as interest rates fluctuate.

Conclusion: Navigating the Numbers with Lendtoday

The Interest Rate Differential penalty is a complex, often frustrating hurdle for Canadian homeowners. It highlights the importance of not just looking at the lowest interest rate when you sign a mortgage, but also looking at the fine print regarding how penalties are calculated.

At Lendtoday, we specialize in looking past the surface-level rates. We help Ontario homeowners analyze whether breaking a mortgage makes financial sense and hunt for lenders with “fair-penalty” clauses to protect you in the future. Don’t let a hidden calculation stall your financial progress. Whether you’re looking to refinance or buy your next home, we’re here to ensure your mortgage works for you, not the other way around.