Which is better HELOC or cash-out refinance? Buying a home in Canada isn’t only rewarding and fulfilling, but it’s also beneficial in many ways. If down the road you need funds to help you renovate or pay off credit, you can tap into your home’s equity. Whether you need funds for your children’s schooling or for investing, using your home equity lets you access to cash quickly and with better terms.

HELOC and Cash-Out Refinance are two methods that let you acquire funds from the equity you’ve built up. This article will discuss the benefits of both methods and which is suitable for your needs.

Understanding what a HELOC is

A home equity line of credit or HELOC offers a line of credit that you can keep using to pay off debt or for a vacation. Like credit cards, you are given a maximum amount that you can use however you want. Your “limit” depends on the equity you have built up for your home. You’re free to use some or the entire amount. With HELOC, you are charged variable interest based only on the amount that you have borrowed. The monthly payment would vary as it depends on the current interest rate and how much you borrow at a certain time.

One of the advantages of HELOC is that you can only borrow the amount you need, which will reduce your monthly payment. However, you do need to discipline yourself if you don’t want higher monthly payments.

Benefits of HELOC

You can borrow up to 80 percent of your home equity with HELOC. Below are the benefits of using it:

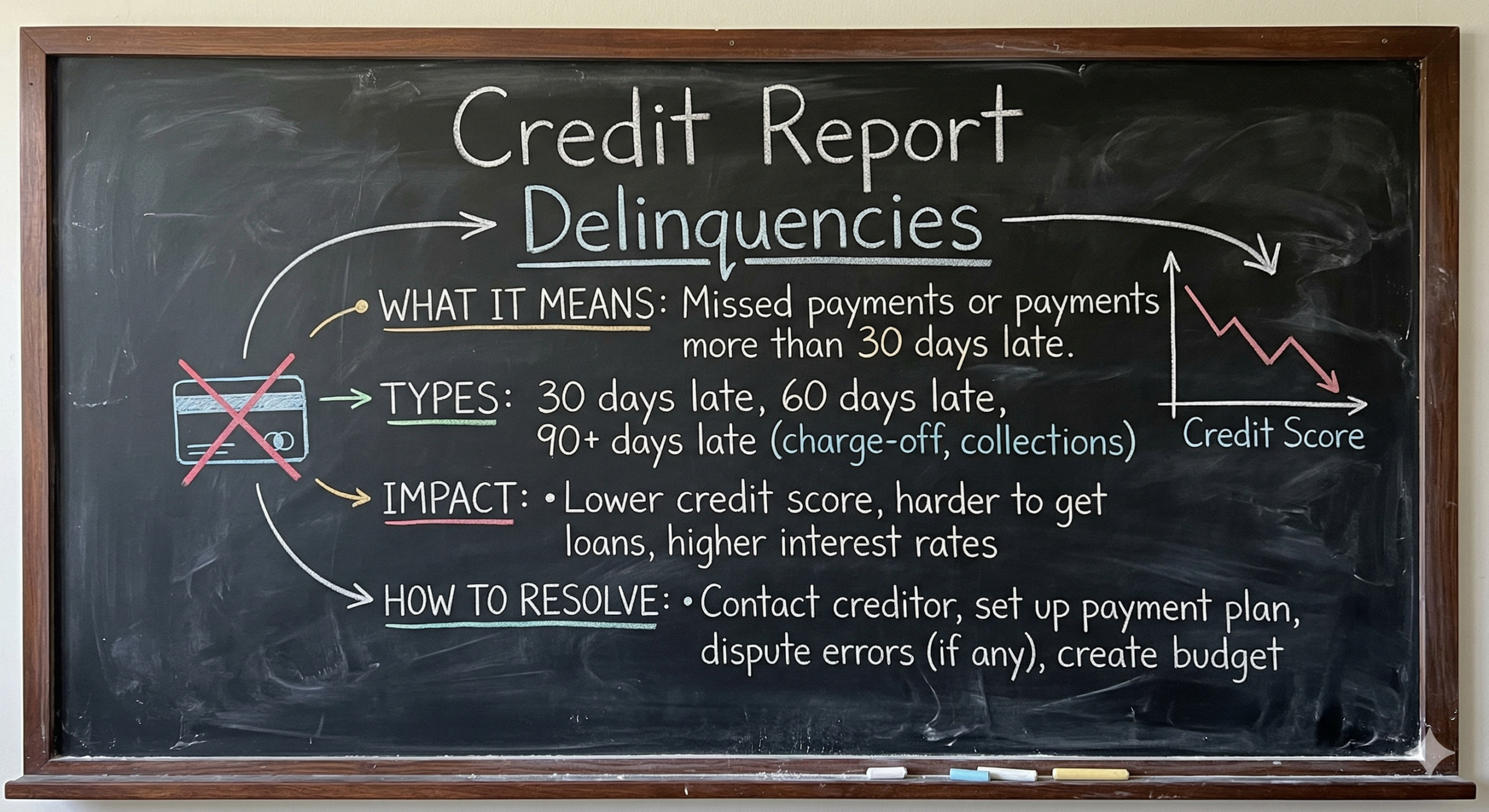

Improve your credit score

One factor that would raise your credit score is the payment history and the different types of credit that you acquire. Adding HELOC and making on-time payments every month can significantly boost your credit score.

Fewer Restrictions on the Funds

With HELOC, you’re free to use the funds however you like. You don’t need to use it for home improvements only; you can use it to pay off debt, travel, or school tuition costs. If you use it for home improvements, you may be able to deduct the interest paid on your HELOC.

You May Qualify for a Low APR

One of the benefits of getting HELOCs is that you can have lower interest rates and lower initial costs. It’s one of the best options if you’re trying to consolidate your debt. Compared to credit cards, HELOC has better rates. The average APR for credit cards is higher.

Like all other loans, it’s essential to have a good credit standing to improve your chances of getting approval. You need to also prove that you have an income. Don’t worry, as we are a team of professionals who can connect you with lenders who can approve borrowers with bad credit.

Cash-Out Refinance

Another way to tap into the equity of your home is by acquiring a cash-out refinance. With this option, you replace your current home loan with a new one, allowing you to benefit from your home’s equity. With a cash-out refinance, you usually get a lower interest rate for the new loan or a shorter term of your loan. Additionally, you can withdraw in a lump sum a portion of your home’s equity. The more equity you have built up, the bigger amount you can borrow.

A cash-out refinance is advantageous when you can reduce the interest rate on your first mortgage and use the funds well. It’s ideal for those borrowers who want to renovate their homes because they want to sell them in the future. With the lump sum, you can also use it to consolidate debts.

With your new mortgage, you can use it for funding your home renovation projects or when you’re planning to invest in another property. Like the HELOC, you can also use the money for consolidating your high-interest debts, paying for your credit cards, or for your child’s education.

Benefits of Cash-Out Refinance

The benefits of the cash-out refinance are similar to the HELOC. You can still lower your interest fees and improve your credit, especially when you make on-time payments every month. You can also leverage the tax deductions if you plan to use the cash-out refinance for home improvement.

To take advantage of the tax deductions, you can use your cash-out refinance funds for these acceptable projects:

- Adding a swimming pool

- Installing a home security system

- Improving your roof

- Replacing your windows

- Constructing a new bathroom or bedroom

One of the differences between HELOC and Cash-Out Refinance is the Closing Cost. You will need to pay for it as you are going to fully pay the existing loan. The prepayment penalty may be equal to three months worth of interest.

With the cash-out refinance, you can have a lump sum; however, the interest accrues on a full loan, whereas, with HELOC, the interest is only on what you withdraw.

Which One is Right For You?

Whether you should get HELOC or Cash-Out Refinance depends on your needs. If you prefer a lump sum, then cash-out refinances may be what you need. However, if you’re not really thinking about using the money now or you don’t want to pay for closing costs, consider getting the HELOC.

Talk to us so we can help you make an informed decision on which one is suitable for you. We are highly experienced when it comes to HELOC, cash-out refinance, or second mortgages. We are also connected with different lenders in Canada. Our team can help you get approved for either of the two, albeit if you have bad credit. Get in touch with us so we can talk about your financial options. Our team is more than happy to assist. You may also choose to apply today!

- Hard Money Lender Alberta: Guide for Homeowners in 2026 - February 26, 2026

- How Many Paystubs Are Required for a Mortgage in Canada? Helpful Guide - February 19, 2026

- Home Insurance Requirements for a Mortgage in Canada - February 13, 2026