How Much Mortgage Can I Afford in Canada? (2025 Affordability Guide)

Buying a home in Canada in 2025 can feel overwhelming, especially with affordability stretched in many provinces. The big question for most households is:

“How much mortgage can I realistically afford?”

The answer depends on your income, debt load, and where you’re buying. In this guide, we’ll walk through the latest affordability data, provide real-life Ontario examples, and even include a manual mortgage affordability calculator so you can estimate for yourself.

Why Mortgage Affordability Matters

Mortgage affordability is more than just the amount a bank says you qualify for. It’s about what you can comfortably afford while still having money left over for savings, unexpected expenses, and everyday life.

The main factors are:

-

Household income

-

Monthly debts (loans, credit cards, car payments)

-

Homeownership costs (taxes, heat, insurance, condo fees)

-

Stress test rate (you must qualify at the greater of 5.25% or your contract rate + 2%)

👉 Want a deeper dive? See our earlier guide: Mortgage Pre-Approval and Affordability Simplified.

2025 Affordability Snapshot

According to CREAJuly 2025 data:

-

Ontario average resale price: $822,356

-

Alberta average resale price: $503,123

-

National average resale price: $672,784

For example household incomes, let’s assume:

-

Ontario household income: $110,000

-

Alberta household income: $104,000

Comparison Table

| Province | Example Household Income | Typical Max Mortgage (20% down, stress test 5.25%+) | Avg. Home Price (Jul 2025) |

|---|---|---|---|

| Ontario | $110,000 | ~$500,000 – $550,000 | $822,356 |

| Alberta | $104,000 | ~$475,000 – $525,000 | $503,123 |

Key takeaway:

-

In Ontario, many households face a significant affordability gap between income-based mortgage capacity and average prices.

-

In Alberta, households are closer to an affordability balance, though still stretched in certain markets.

How Do Lenders Decide What You Can Afford?

Lenders use a few standard rules to size up affordability:

-

Gross Debt Service (GDS): Housing costs (mortgage + taxes + heat + half of condo fees) ≤ 35% of gross income.

-

Total Debt Service (TDS): All debts (housing + loans + credit cards) ≤ 42% of gross income.

For our Ontario household earning $110,000/year (~$9,166/month):

-

GDS limit: ~$3,208/month

-

TDS limit: ~$3,850/month

If that household already has $800/month in debt payments, their maximum housing payment shrinks to ~$2,400–$2,600/month.

Example: Ontario Household in 2025

-

Household income: $110,000

-

Other debts: $800/month (car + credit cards)

-

Property taxes & heating: $450/month

➡️ Under GDS/TDS, this household could afford a mortgage around $500,000–$525,000.

But with Ontario’s average price at $822,356, they would likely need:

-

A larger down payment,

-

A longer amortization (if uninsured), or

-

Alternative financing options through a mortgage broke

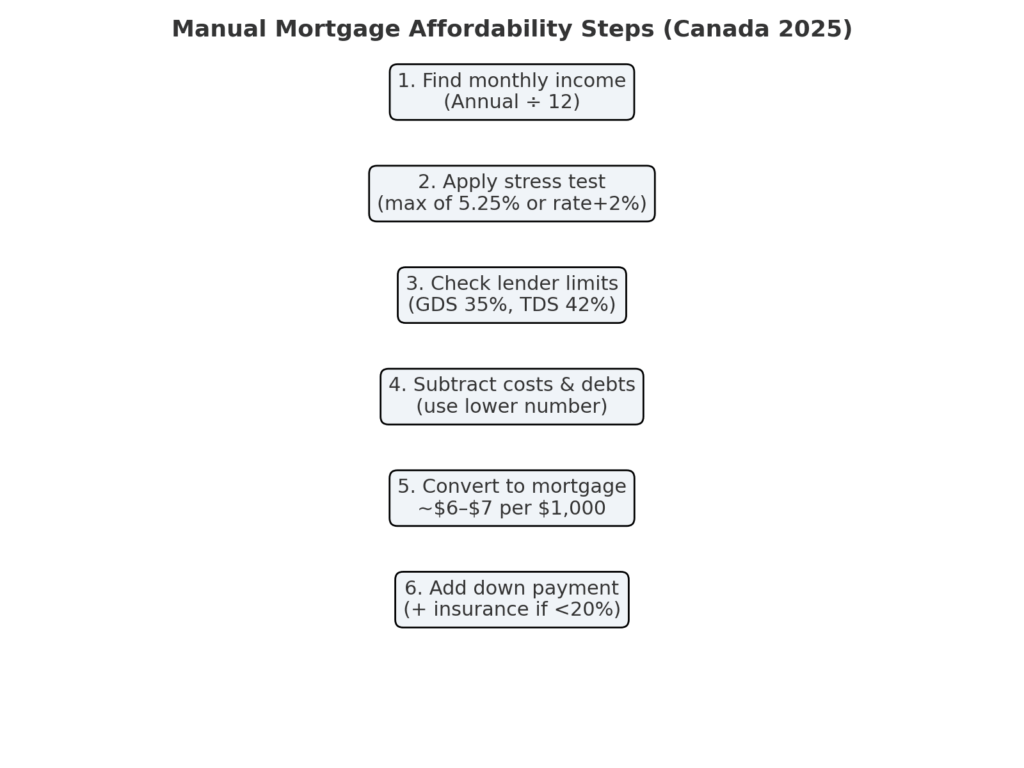

How to Manually Calculate Your Mortgage Affordability

If you’d rather skip calculators, here’s a quick way to estimate what you can afford:

-

Find your monthly income

Divide your household income by 12.

Example: $110,000 ÷ 12 = $9,166/month -

Apply the stress test

Use the higher of 5.25% or your contract rate + 2%. -

Check the lender limits

-

GDS (35%): Housing costs ≤ 35% of monthly income

-

TDS (42%): All debts ≤ 42% of monthly income

-

-

Subtract fixed costs and debts

-

GDS room = 35% of income – (taxes + heat + 50% condo fees)

-

TDS room = 42% of income – (other monthly debts)

→ Use the lower number as your max housing payment.

-

-

Convert payment into mortgage

As a rule of thumb (25-year amortization):-

At 5.25%: every $1,000 mortgage costs ≈ $6/month

-

At 7%: every $1,000 mortgage costs ≈ $7/month

Example: $2,800/month budget ÷ $7 = ~$400,000 mortgage

-

-

Add your down payment

Mortgage + down payment = rough home price.

(Add insurance premium if <20% down.)

Making Your Mortgage More Affordable

Here are a few ways Canadians in 2025 are keeping payments manageable:

-

Bigger down payment → Reduces the size of the mortgage.

-

Extended amortization → Lowers monthly payments (but more interest overall).

-

Comparison shopping → A mortgage broker can shop across banks, credit unions, and private lenders.

-

Government incentives → First-Time Home Buyer Incentive still applies in some cases.

-

Debt reduction before applying → Improves your TDS ratio.

Additional Costs to Remember

Beyond the mortgage itself, budget for:

-

Closing costs (1.5–4% of purchase price)

-

Land transfer tax (varies by province and municipality)

-

Home insurance

-

Ongoing expenses like utilities and condo fees

Start Your 2025 Home-Buying Journey with LendToday

At LendToday, we recognize that mortgage affordability in 2025 is more challenging than ever. Rising home prices in Ontario, steady increases in Alberta, and the impact of the mortgage stress test all mean Canadian families need to look carefully at both their current financial situation and their future goals before stepping into homeownership.

Our role is not just about securing you a mortgage—it’s about helping you gain clarity on your overall finances. We work with clients to:

-

Review today’s reality: income, debts, credit, and monthly obligations.

-

Uncover budgeting strategies: from reducing non-essential spending to consolidating high-interest debts so more of your income can go toward housing.

-

Plan for tomorrow: whether it’s preparing for a first home, upgrading to a larger property, or building equity to improve financial stability.

By exploring both short-term solutions (such as flexible mortgage products) and long-term options (like refinancing strategies or building a stronger credit profile), we aim to make homeownership more sustainable, not just possible.

If you’re ready to see what’s realistic for your household, let’s talk. Call us today at 1-855-242-7732 or begin your affordability review online—your path to a home you can truly afford starts with a clear plan.