The Great Benefits of a Conventional Mortgage. Homeownership is a cherished goal for many Canadians, offering not just a place to live but also a significant investment opportunity. When navigating the world of mortgages, it’s important to choose a financing option that aligns with your financial situation and long-term goals. For those who can make a substantial down payment, a conventional mortgage offers numerous benefits, from lower overall costs to greater financial flexibility. This blog will take a closer look at how conventional mortgages work in Canada, their advantages, and how they compare to other mortgage types.

Table of Contents

- What is a Conventional Mortgage in Canada?

- Benefits of Choosing a Conventional Mortgage

- Lower Mortgage Insurance Requirements

- Competitive Interest Rates

- Flexible Terms

- Tailored to Your Financial Situation

- Potential for Faster Equity Building

- The Role of the Down Payment in a Conventional Mortgage

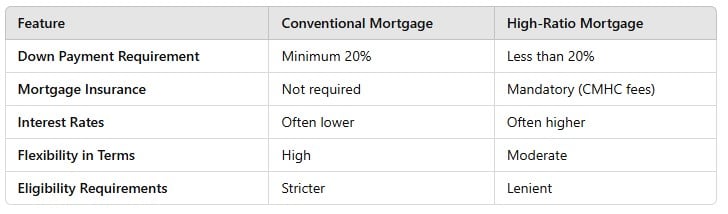

- Comparing Conventional Mortgages to High-Ratio Mortgages

- How to Qualify for a Conventional Mortgage in Canada

- Is a Conventional Mortgage Right for You?

- Conclusion

What is a Conventional Mortgage in Canada?

In Canada, a conventional mortgage is a home loan where the borrower provides a down payment of at least 20% of the property’s purchase price. This higher down payment means the mortgage is not classified as “high-ratio” and, therefore, does not require mortgage loan insurance through organizations like the Canada Mortgage and Housing Corporation (CMHC), Genworth Financial, or Canada Guaranty.

By eliminating the need for mortgage insurance, this mortgage saves homeowners a significant amount of money, particularly at the time of closing and over the life of the loan. Additionally, conventional mortgages typically come with more flexibility in terms and conditions compared to high-ratio mortgages.

Benefits of Choosing a Conventional Mortgage

- Lower Mortgage Insurance Requirements

One of the most immediate benefits is that it avoids the need for CMHC mortgage insurance. For high-ratio mortgages (where the down payment is less than 20%), the CMHC charges an insurance premium that ranges from 2.8% to 4.0% of the loan amount. This premium can either be paid upfront or added to the mortgage balance, increasing the total cost of the home.

With a conventional mortgage, you eliminate this expense entirely, leading to significant savings.

- Competitive Interest Rates

Borrowers who qualify for conventional mortgages often have strong credit profiles, making them less risky to lenders. As a result, lenders are more likely to offer lower interest rates to these borrowers. Even a small difference in the interest rate can save homeowners tens of thousands of dollars over the course of a 25-year amortization.

- Flexible Terms

It offers greater flexibility in choosing the term of the loan. In Canada, mortgage terms typically range from 1 to 5 years, with options for fixed or variable interest rates. Fixed rates provide stability in monthly payments, while variable rates often start lower and can adjust with market conditions. Borrowers can choose terms that match their financial goals and risk tolerance.

- Tailored to Your Financial Situation

Lenders have more leeway when approving these types of mortgages since they are not bound by the stricter rules associated with insured mortgages. This flexibility allows borrowers to negotiate terms that better align with their individual circumstances, such as repayment schedules and prepayment privileges.

- Potential for Faster Equity Building

With a larger down payment, conventional mortgage holders start with more equity in their homes. This not only reduces the amount of interest paid over time but also provides a financial buffer in case of market fluctuations. Home equity can also be tapped into later for purposes like home renovations, debt consolidation, or investing.

The Role of the Down Payment

The size of your down payment plays a crucial role in securing a conventional mortgage. While the minimum is 20% of the purchase price, many Canadians aim to save even more to reduce the total amount they borrow. Larger down payments can:

- Lower your monthly mortgage payments

- Reduce the total interest paid over the life of the loan

- Increase your eligibility for the most competitive interest rates

Saving for a down payment often requires careful budgeting and planning. Programs like the Home Buyers’ Plan (HBP), which allows Canadians to withdraw up to $35,000 from their RRSPs tax-free for a down payment, can help first-time buyers achieve this goal.

Comparing Conventional Mortgages to High-Ratio Mortgages

High-ratio mortgages are often more accessible for first-time buyers with smaller savings, but they come with additional costs and restrictions. Conventional mortgages, on the other hand, are better suited for those with established financial stability.

How to Qualify for in Canada

To qualify, Canadian borrowers typically need to meet the following criteria:

- Down Payment: A minimum of 20% of the home’s purchase price.

- Credit Score: This can range from lender to lender but a minimum of 550 with alternative lenders

- Debt-to-Income Ratio: Your total debt payments (including the mortgage)

- Proof of Income: Employment verification and proof of stable income are essential.

It’s advisable to consult a mortgage broker or financial advisor to determine your eligibility and understand how to strengthen your application.

Is a Conventional Mortgage Right for You?

Its ideal for Canadians who:

- Have saved enough for a 20% down payment

- Want to avoid paying mortgage insurance premiums

- Have a strong credit profile and stable income

- Are looking for flexibility in mortgage terms and repayment options

While these mortgages are not suitable for everyone, they offer significant financial advantages for those who qualify. Homebuyers who cannot meet the 20% down payment requirement can explore high-ratio mortgage options and work toward transitioning to a conventional mortgage later.

Conclusion

Conventional mortgages are an excellent choice for Canadian homeowners seeking to minimize costs and maximize flexibility. With lower interest rates, no mortgage insurance requirements, and the ability to build equity faster, this type of mortgage provides a clear path to achieving long-term financial stability.

If you’re considering buying a home in Canada, take the time to explore whether a conventional mortgage aligns with your financial goals. The choice could save you thousands over the lifetime of the mortgage. With the right preparation and guidance, your dream home could be closer than you think.