If you’re planning to buy a home, refinance your mortgage, or secure additional financing using your home in Ontario, one essential step is identity verification. Lenders—whether banks, credit unions, or private lenders—require valid identification to protect against fraud and comply with federal and provincial laws. Understanding what ID for mortgage is accepted can save you time and prevent unnecessary delays.

In Ontario, the most common requirement is two pieces of valid ID—one with a photo and one that may be non-photo. The documentation must match your full legal name and be valid (not expired). In some cases, additional documents like utility bills or a SIN card may be needed to confirm your identity or address. Whether you’re applying for your first mortgage or refinancing, here’s what you need to know about ID requirements in Ontario.

Table of Contents

ToggleWhy ID Is Needed for a Mortgage in Ontario

Mortgage lenders in Ontario are legally obligated to verify your identity before they approve or fund a mortgage. This isn’t just an internal policy—it’s a compliance requirement enforced through Canadian federal regulations and provincial mortgage brokerage laws.

Key reasons include:

-

Anti-Money Laundering (AML) Compliance: Canadian lenders must follow FINTRAC regulations and Know Your Customer (KYC) policies to prevent fraud.

-

Legal Document Matching: Your ID must match the mortgage application, land title registration, and legal documents.

-

Fraud Protection: Confirming your ID helps prevent mortgage fraud and impersonation.

Key takeaway: The ID for mortgage approval is not optional—it’s a regulated requirement for all lenders in Ontario.

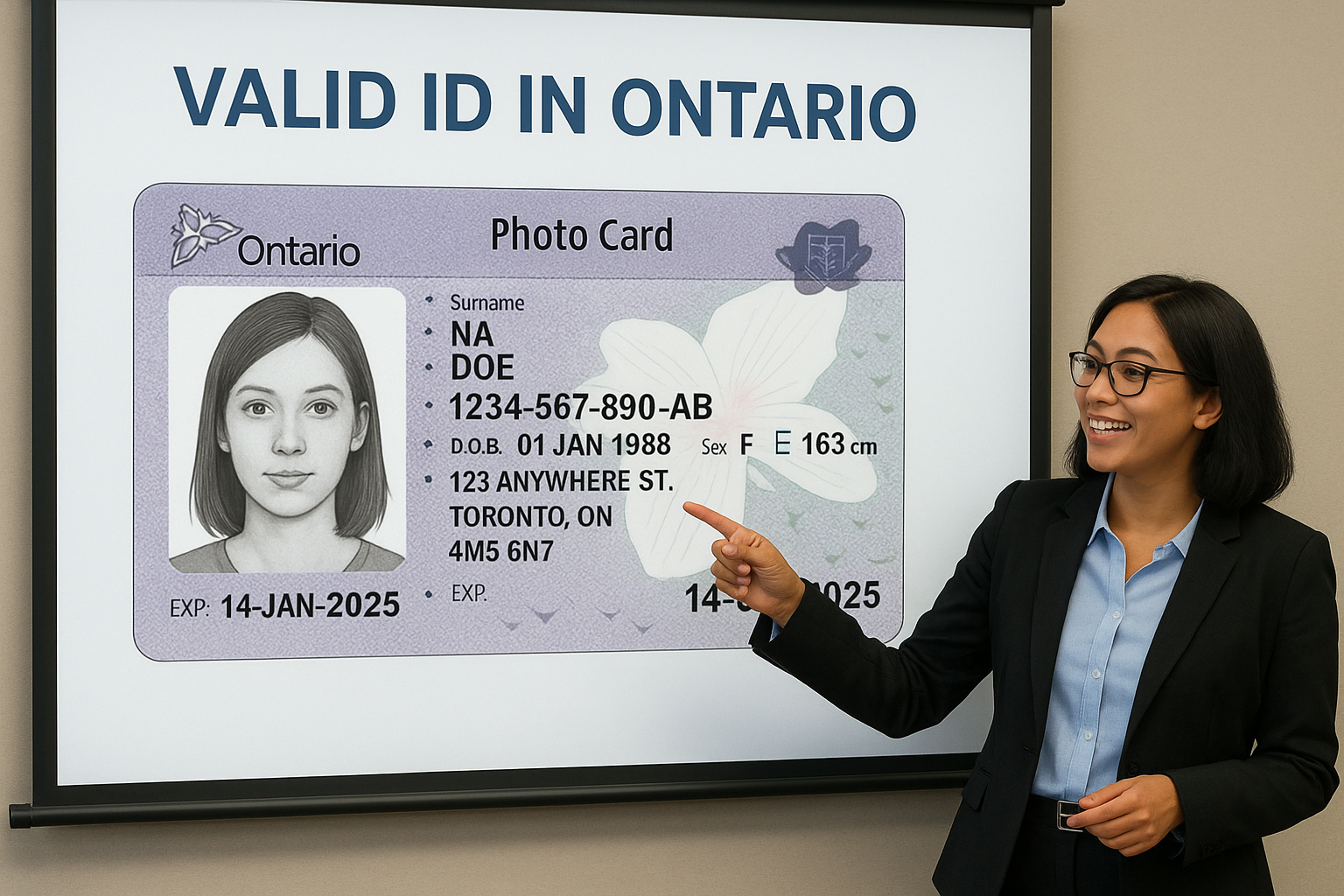

Types of ID Accepted for a Mortgage in Ontario

Different lenders may have slightly varying standards, but all require two valid forms of ID, including one government-issued photo ID.

Here’s a breakdown:

Primary ID (Photo ID)

This is the most important form of ID for mortgage applications in Ontario.

-

Canadian Passport

-

Ontario Driver’s Licence

-

Ontario Photo Card (issued by ServiceOntario)

-

Permanent Resident Card

-

Canadian Armed Forces ID

These IDs must:

-

Be valid and not expired

-

Display your full legal name

-

Be issued by a government authority

Common mistake: Submitting an expired driver’s licence. Even if it expired yesterday, it cannot be accepted.

Secondary ID (Non-Photo or Supplemental)

This second piece helps verify your identity or confirm your address.

-

SIN Card (original only—not a photocopy)

-

Canadian Birth Certificate

-

Citizenship Certificate

-

Utility bill (within the past 60 days)

-

CRA notice of assessment

-

Major credit card or bank statement with your name

Important to note: Both pieces of ID must complement each other. If your photo ID shows a maiden name and your bill shows your married name, you’ll need to provide legal proof of name change.

Checklist for Mortgage ID in Ontario

✅ One valid government-issued photo ID

✅ One secondary piece of ID (e.g., SIN, utility bill)

✅ Full legal name matches mortgage application

✅ ID must not be expired

Special Cases That May Affect ID Requirements

Name Mismatches or Recent Name Changes

If your current ID doesn’t reflect your legal name, you’ll need additional documentation.

Accepted proofs:

-

Marriage certificate

-

Divorce decree

-

Legal name change certificate

Common myth: You can “just explain” your name change to the lender—not true. You’ll need legal proof.

Newcomers or Non-Residents

If you’re new to Canada or are not a permanent resident, lenders will request different documentation.

Additional documents may include:

-

Foreign passport (if Canadian ID unavailable)

-

Immigration documents (PR card, work permit, study permit)

-

Canadian utility bill or lease agreement

Some private lenders may still proceed with just a passport and immigration status, but it’s on a case-by-case basis.

Power of Attorney or Corporate Borrowers

In these cases, you’ll be asked for documentation to prove authorization:

-

Certified Power of Attorney document

-

Two IDs for the person acting as attorney

-

Corporate registry and signing authority verification

Important to note: The original Power of Attorney document may need to be registered with the local land registry office before closing.

What Happens If You Don’t Have Proper ID?

If you can’t provide the correct ID for mortgage purposes in Ontario, your application may stall—or worse, be denied.

Possible scenarios:

-

Delays: The lender cannot complete their underwriting without full ID verification.

-

Denials: Some lenders have strict no-ID policies—no exceptions.

-

Additional steps: You may need to visit a notary public or government office to confirm your identity.

Common myth: You can use your Ontario health card as ID. False. Ontario health cards are not acceptable for mortgage applications.

How to Prepare Your ID for a Smooth Mortgage Application

To prevent delays or rejections, here are a few tips for preparing your ID:

Before applying:

-

Check that your ID is valid and not expiring soon

-

Ensure the name matches across all documents

-

If you’re planning to change your name (e.g., post-marriage), delay your application or ensure you have proof of the change

When applying:

-

Send scanned copies or photos in high resolution

-

Inform your broker or lender if you anticipate ID issues

-

Ask early about ID requirements if using a private lender

Key takeaway: The best way to avoid complications is to be proactive. Notify your lender in advance if something is out of the ordinary.

ID for Mortgage Refinancing vs. New Purchase

Whether you’re purchasing a new home or refinancing your existing mortgage, the ID requirements are the same:

-

Two valid IDs must be provided

-

Supporting documents like property tax bills, utility bills, and your current mortgage statement may also be requested

-

If refinancing through a private lender, they may ask for additional proof of ownership (e.g., property title)

Important to note: Even if you’ve dealt with the lender before, they’ll ask for ID again—it’s not stored long-term due to privacy laws.

Comparison Table: Accepted ID Types for a Mortgage in Ontario

| Type of ID | Examples | Required For | Notes |

|---|---|---|---|

| Primary (Photo ID) | Driver’s Licence, Passport | All mortgage applications | Must be valid and match legal name |

| Secondary (Non-Photo ID) | SIN Card, Utility Bill | Address verification | Utility bill must be recent |

| Special Cases | PR Card, Immigration Docs | Newcomers | May require multiple documents |

| Legal Name Change Proof | Marriage Certificate, Legal Change Cert | Name mismatch | Must be official government-issued |

Identification Verification for Title Insurance Companies

When applying for a mortgage in Ontario, it’s not just the lender that needs to verify your ID—title insurance companies also require strict identity verification as part of their risk assessment process. This step is mandatory whether you’re purchasing a home, refinancing, or securing a second mortgage.

What is Title Insurance?

Title insurance protects homeowners and lenders against losses related to the property’s title or ownership. It covers issues like:

-

Unknown title defects

-

Existing liens or encumbrances

-

Fraud or forgery

-

Survey errors or boundary disputes

-

Title impersonation

Important to note: Most lenders won’t advance funds without a title insurance policy in place.

Why Title Insurance Companies Scrutinize ID

Since identity theft and real estate fraud have been on the rise across Canada, title insurers now play a critical role in verifying a borrower’s identity. The process is intended to prevent fraudulent activity like:

-

Forged signatures on mortgage documents

-

Impersonation of the property owner

-

Use of stolen or fake ID for mortgage applications

To protect all parties involved, title insurance companies often ask lawyers or notaries to:

-

Confirm the borrower’s identity in person

-

Validate two pieces of ID

-

Record details for audit purposes

FAQ: ID for Mortgage in Ontario

Q: Can I use my Ontario health card as ID for a mortgage?

A: No. Ontario health cards cannot be used as ID for mortgage purposes due to health privacy laws. Use a driver’s licence or passport instead.

Q: What if my ID shows a maiden name but my mortgage application uses my married name?

A: You’ll need to provide a legal marriage certificate or name change document to prove the identity match.

Q: I’m self-employed—do I need additional ID?

A: No extra ID is needed just for being self-employed, but you may be asked to provide income proof separately (e.g., business registration or CRA statements).

Q: Can I use a credit card as ID?

A: Credit cards may be used as a secondary ID, but only when paired with a primary photo ID. It must have your full legal name.

Q: What happens if my ID is expired?

A: Your mortgage application can’t proceed until valid ID is provided. Renew your documents before applying.

Final Thoughts on ID Requirements for a Mortgage in Ontario

When applying for a mortgage in Ontario, providing valid and correct ID is just as important as having a strong credit score or proof of income. Whether you’re working with a bank, credit union, or private lender, having your ID ready will streamline the approval process and protect you from legal or financial delays.

If your situation is unique—such as a recent name change, newcomer status, or acting under Power of Attorney—it’s essential to let your mortgage professional know early in the process.

Key takeaway: Being prepared with the right ID can mean the difference between a fast mortgage approval and a frustrating delay. Always double-check, ask questions, and stay informed.

Questions About Id? We Can Help