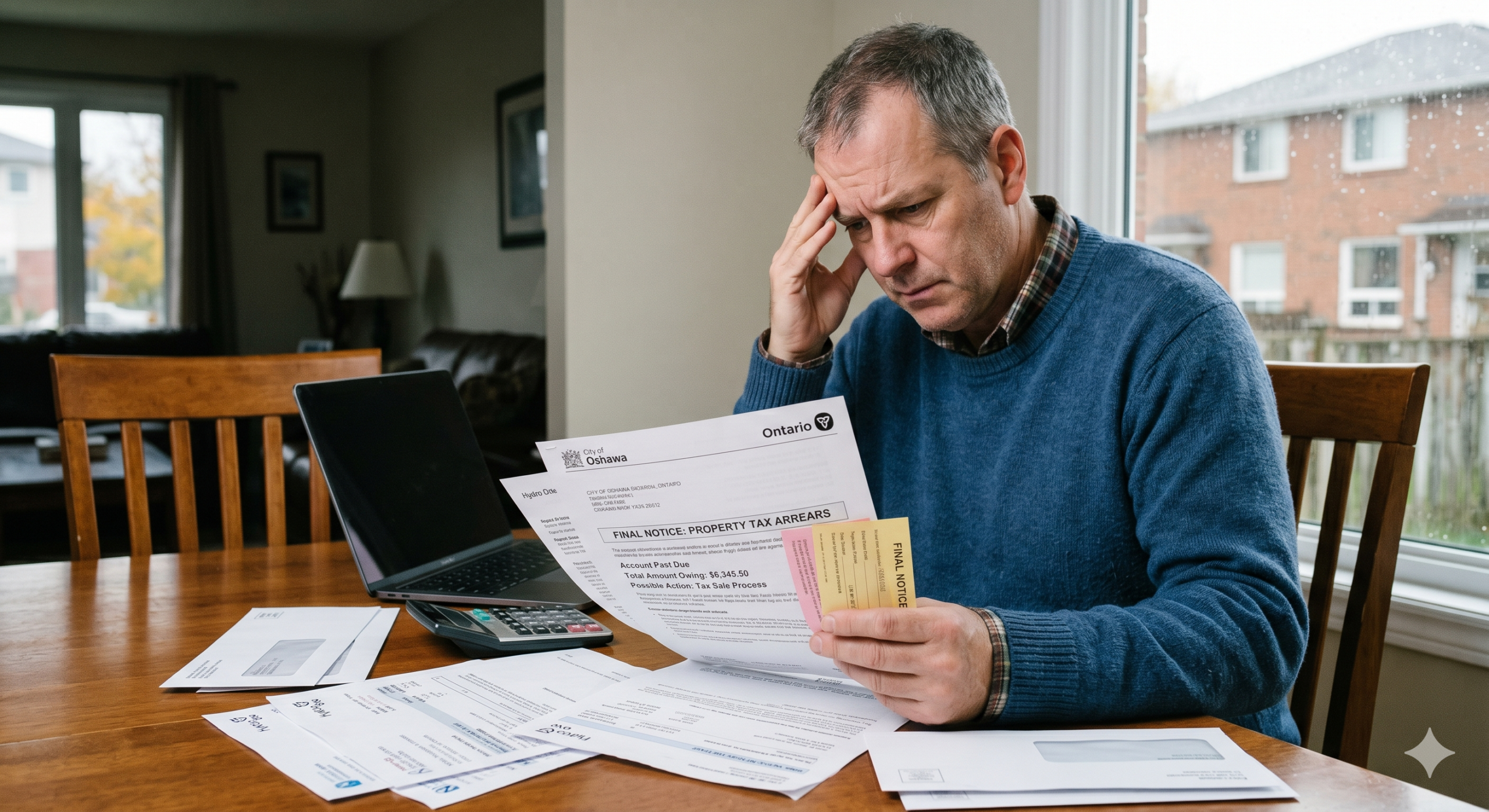

Most Ontario homeowners know they have to pay property taxes. What most don’t know is exactly what happens when they fall behind — and how quickly a manageable situation can spiral into a serious threat to their home.

Property tax arrears are more common than people think. A job loss, health issue, divorce, or simply a larger-than-expected tax bill can push any homeowner into overdue territory. The good news: there are real solutions — especially if you act early. The bad news: waiting too long significantly narrows your options.

Here’s a clear, honest look at what the process actually looks like in Ontario, and what you can do to catch up.

Table of Contents

ToggleWhy Property Taxes Are Not Like Other Debts

Before we get into the timeline, it’s worth understanding what makes property tax debt different — and why it demands urgent attention.

Unlike a credit card balance or a personal loan, unpaid property taxes carry “super priority” status under Ontario law. This means the municipality’s claim on your property ranks above virtually every other debt — including your mortgage. Your lender doesn’t get paid first. The municipality does.

This also means that if your tax arrears grow large enough, your mortgage lender may step in and pay them on your behalf to protect their own position — and then treat that as a default on your mortgage. In other words, falling behind on property taxes can trigger a power of sale situation even if you haven’t missed a single mortgage payment.

The Ontario Property Tax Arrears Timeline

Understanding the process helps you know exactly when the clock starts ticking.

Stage 1: Overdue Notices (Month 1 Onward)

The moment a payment is missed, interest begins accumulating. In Ontario, most municipalities charge 1.25% per month on the unpaid balance. You’ll start receiving collection notices, and the amounts grow faster than most people expect.

Stage 2: Escalating Collection Activity (Months 3–12+)

If no payment or payment arrangement is made, your file can be escalated to a tax collection officer or the municipality’s legal department. Some lenders may also be notified. The letters become more urgent, and the balance continues to grow.

Stage 3: Tax Arrears Certificate (After 2 Years)

Under the Ontario Municipal Act, 2001, if property taxes remain unpaid for two calendar years, the municipality can register a Tax Arrears Certificate on your property’s title. This is a formal legal lien. Everyone with a registered interest in the property — including your mortgage lender — receives notice by registered mail.

Stage 4: The One-Year Countdown

Once a Tax Arrears Certificate is registered, you have one year to pay the full cancellation price — which includes all unpaid taxes, accumulated interest, penalties, and costs. This is not a negotiable partial payment; the full amount must be paid to have the certificate removed.

Critically, once the certificate is registered, municipalities cannot accept partial payments unless you enter into a formal extension agreement before the one-year period expires.

Stage 5: Tax Sale

If the cancellation price isn’t paid within that year and no extension agreement is in place, the municipality can list your property for a tax sale by public tender. The property is advertised in local papers and the Ontario Gazette. The highest bidder wins — and you lose the home.

Any proceeds beyond the outstanding taxes are returned to you, but by this point, legal costs, penalties, and the compounding effect of interest typically eat into that significantly.

Important: The full process from first missed payment to tax sale typically spans three or more years — but don’t let that timeline give you false comfort. The later you act, the more you owe, the fewer lenders will work with you, and the less equity you have to work with.

What Your Mortgage Lender Will Do

Most mortgage agreements contain a clause requiring property taxes to be kept current. If your lender discovers you’re in arrears — either through the Tax Arrears Certificate process or their own monitoring — they may:

- Pay the outstanding taxes on your behalf to protect their position

- Add that amount to your mortgage balance, triggering a shortfall or default

- Issue a demand letter requiring repayment

- Begin power of sale proceedings if you cannot cure the default

This is one of the most commonly misunderstood risks of property tax arrears. You can lose your home through this route without the municipality ever proceeding to a tax sale.

Your Options for Catching Up

The sooner you act, the more options you have. Here’s what’s available at different stages:

1. Municipal Payment Plans

Most Ontario municipalities offer installment payment plans that let you pay off arrears over time while keeping current on new tax obligations. You typically need to contact the tax department directly, explain your situation, and formally apply. These plans are usually only available before a Tax Arrears Certificate is registered.

2. Property Tax Deferral Programs

Some municipalities offer deferral programs for low-income homeowners, seniors, or those experiencing financial hardship. These programs vary widely by municipality — contact your local tax office to ask what’s available in your area.

3. Home Equity Loan or Second Mortgage

If you have equity built up in your home, this is often the most powerful tool available. A home equity loan or second mortgage can provide the lump sum needed to clear the arrears entirely — removing the lien, stopping the interest clock, and eliminating the risk of tax sale or power of sale.

The advantage here is significant: private lenders and alternative lenders assess your application based primarily on your home equity, not your credit score or income history. Even if your credit has taken a hit from the financial pressure that caused the arrears in the first place, you may still qualify.

4. Mortgage Refinancing

If the arrears haven’t yet been registered as a lien, and your mortgage is approaching renewal, refinancing to roll the arrears into your mortgage balance is another option. This needs to be explored before a Tax Arrears Certificate is filed, as most traditional lenders will not touch a property with a registered lien on title.

5. Private Lending

When traditional lenders won’t help either because of the lien, credit issues, or income irregularities private lenders can step in quickly with bridge financing to resolve the arrears. Private lending is not a long-term solution, but it can buy critical time and protect your equity from being wiped out in a forced tax sale.

A Note on Acting Early

The single most important piece of advice in this entire article: don’t wait for the registered mail.

Once a Tax Arrears Certificate hits your title, your options narrow dramatically. Partial payments can no longer be accepted. Traditional lenders won’t refinance the property. The full cancellation price including every accumulated penalty, interest charge, and legal cost must be paid in one shot.

At that point, the only practical solutions are private lending or a home equity product from an alternative lender. Both are available, but the cost is higher and the timeline is tighter than it would have been months earlier.

If you’ve missed even one or two payments, or if you’re receiving collection notices, now is the right time to explore your options — before the situation becomes a crisis.

FAQ

What happens if you don’t pay property taxes in Ontario?

If property taxes go unpaid, your municipality will begin charging monthly interest and penalties on the outstanding balance. Over time, collection activity escalates, and after two years of arrears the municipality can register a Tax Arrears Certificate on your property’s title — formally starting the countdown toward a potential tax sale. Your mortgage lender may also intervene, paying the taxes on your behalf and treating the amount as a mortgage default.

How long before the municipality can sell my home for unpaid property taxes?

Under Ontario’s Municipal Act, 2001, a Tax Arrears Certificate can be registered after two calendar years of unpaid taxes. Once registered, you have one year to pay the full cancellation price. If no payment or extension agreement is made within that year, the municipality can proceed with a tax sale by public tender — meaning the full process takes a minimum of three years, but acting early is critical.

Can I lose my home to property tax arrears even if I’m paying my mortgage?

Yes. Most mortgage agreements require property taxes to be kept current. If your lender discovers significant arrears, they may pay the outstanding taxes on your behalf to protect their position and then treat that amount as a mortgage default — which can lead to power of sale proceedings regardless of your mortgage payment history.

Can I make a partial payment once a Tax Arrears Certificate has been registered?

Generally, no. Once a Tax Arrears Certificate is registered on your title, municipalities are required to collect the full cancellation price — which includes all unpaid taxes, interest, penalties, and costs. Partial payments are not accepted unless you have entered into a formal extension agreement with the municipality before the one-year redemption period expires.

Can I get a loan to pay off property tax arrears if I have bad credit?

Potentially yes if you have sufficient equity in your home. Private lenders and alternative lenders evaluate applications based primarily on home equity rather than credit score or employment history. A home equity loan, second mortgage, or private bridge loan can be used to clear the arrears in full, remove the lien, and stop the interest from compounding further.

What is the fastest way to resolve property tax arrears in Ontario?

The fastest resolution is typically a lump-sum payoff of all outstanding taxes, interest, and penalties. If you don’t have the cash on hand, a home equity loan or private mortgage can provide the funds quickly — often within days. A licensed mortgage broker who specializes in these situations can help you move fast, which matters enormously once a Tax Arrears Certificate has been registered.

How LendToday Can Help

At LendToday.ca, we work with homeowners across Ontario who are dealing with property tax arrears at every stage — from early overdue notices to properties already under a Tax Arrears Certificate. We access a network of over 50 lenders, including private and alternative lenders who specialize in exactly these situations.

We can help you:

- Understand exactly where you are in the arrears process

- Identify which lending solutions apply to your situation

- Move quickly — because in these situations, speed matters

Don’t wait until your options run out. Contact LendToday today for a free, no-obligation consultation.