The Ultimate Guide: 3 Powerful Levels of Mortgages Every Canadian Homeowner Should Know

When it comes to securing financing for a home purchase, refinancing, or debt consolidation, not all mortgages are created equal. In Canada, borrowers typically navigate three levels of mortgage lending: A lending, B lending, and private financing. Each tier comes with its own set of rules, advantages, and requirements.

Understanding these three levels can help you make the right decision for your financial situation—whether you have excellent credit and stable income, or you’re dealing with challenges like self-employment, credit blemishes, or high debt ratios.

In this guide, we’ll break down how A, B, and private mortgages work, who they’re designed for, and why you might need them.

What Are the 3 Levels of Mortgage Lending?

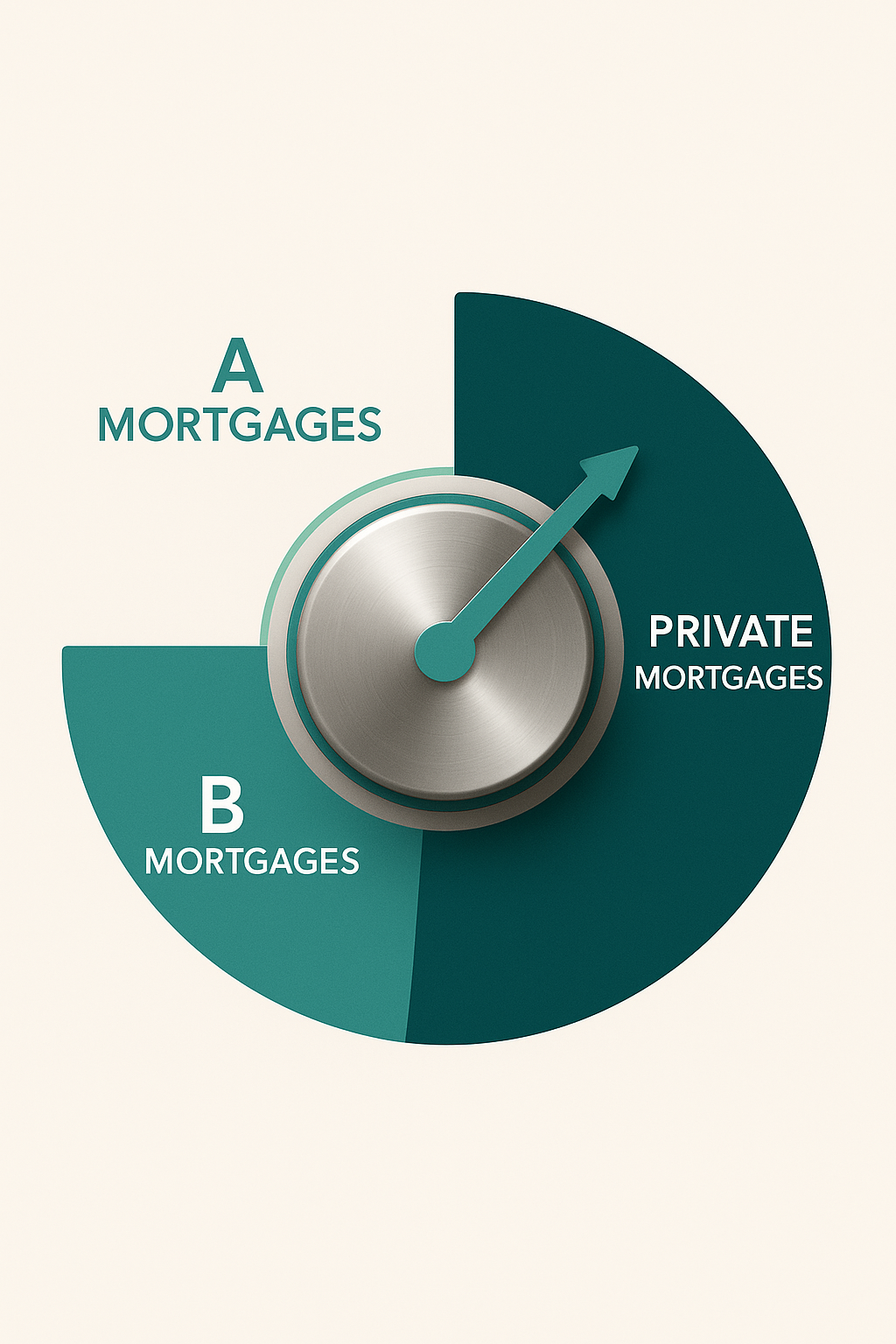

Mortgage lenders in Canada can be divided into three broad categories:

-

A Lenders (Traditional / Prime Lenders)

-

B Lenders (Alternative Lenders)

-

Private Lenders (Equity-Based Lending)

Think of them as steps on a ladder. The higher your financial profile (credit score, income documentation, debt levels), the more likely you’ll qualify for an A lender. If you’re somewhere in between, B lenders may be the right fit. And if banks and alternative lenders say no, private financing becomes the most flexible option.

1. A Lenders – The Traditional Mortgage Route

Who Are A Lenders?

A lenders are the big banks, credit unions, and other prime lending institutions regulated by the federal government. Examples include RBC, TD, Scotiabank, BMO, and CIBC.

What They Look For:

-

Credit Score: Typically 680+ is required.

-

Income: Must be steady and verifiable through pay stubs, T4s, or Notices of Assessment.

-

Debt Ratios: Strict guidelines. Most lenders want your Gross Debt Service (GDS) under 39% and Total Debt Service (TDS) under 44%.

-

Stress Test: You must qualify at the higher of the Bank of Canada qualifying rate or your contract rate plus 2%.

Pros of A Lenders:

-

Lowest interest rates on the market.

-

Long amortization periods (up to 25 or 30 years).

-

Government-backed mortgage insurance available (through CMHC, Sagen, or Canada Guaranty).

Cons of A Lenders:

-

Toughest approval requirements.

-

Limited flexibility if you’re self-employed, new to Canada, or have bruised credit.

When You’d Use an A Lender:

If you’ve got strong credit, stable employment, and manageable debt, an A lender is your first choice. This is the most cost-effective option, giving you the lowest possible borrowing costs.

2. B Lenders – The Middle Ground

Who Are B Lenders?

Also called “alternative lenders” or “near-prime lenders,” B lenders are often trust companies or smaller financial institutions. They operate under less rigid guidelines compared to banks.

What They Look For:

-

Credit Score: Can be as low as 550–600.

-

Income: More flexible income verification, great for self-employed borrowers or those with seasonal work.

-

Debt Ratios: Higher tolerance—sometimes TDS up to 50%.

-

Property Type: Wider acceptance of unique properties that banks may not approve.

Pros of B Lenders:

-

Greater flexibility than banks.

-

Approvals for borrowers who may not meet strict A lender requirements.

-

Ability to consolidate debt into one manageable mortgage payment.

Cons of B Lenders:

-

Higher interest rates than banks (usually 1–3% more).

-

May require lender/broker fees (1–2% of mortgage amount).

-

Shorter terms (often 1–3 years).

When You’d Use a B Lender:

B lending is ideal if you:

-

Have recently recovered from bankruptcy or a consumer proposal.

-

Are self-employed without traditional income proof.

-

Have higher debt ratios than what A lenders accept.

-

Need a short-term solution to rebuild credit and eventually move back to an A lender.

3. Private Lenders – The Flexible Option

Who Are Private Lenders?

Private financing comes from individual investors, Mortgage Investment Corporations (MICs), or small lending firms. These lenders focus primarily on the equity in your home, not your credit or income.

What They Look For:

-

Equity: How much you own in your home. Loan-to-value (LTV) ratios are critical—most private lenders will lend up to 75–85% of your home’s value.

-

Property Location: Urban, in-demand areas are more attractive.

-

Exit Strategy: They want to know how you’ll repay (e.g., refinancing later, selling, or improving credit to move to a B or A lender).

Pros of Private Lenders:

-

Fast approvals—sometimes in just a few days.

-

Minimal documentation required.

-

A solution for urgent situations like stopping foreclosure, paying tax arrears, or consolidating high-interest debt.

Cons of Private Lenders:

-

Highest interest rates (often 7–12% or more).

-

Additional lender fees (2–4% of loan amount).

-

Typically short-term (6 months to 2 years).

When You’d Use a Private Lender:

Private financing is often the “last resort,” but it can be a lifeline. It’s useful if you:

-

Are facing foreclosure or power of sale.

-

Have tax arrears or judgments against you.

-

Need fast financing that banks won’t provide.

-

Want to leverage your home equity without traditional barriers.

Why These 3 Levels of Mortgages Exist

The Canadian mortgage system is designed to serve borrowers at different financial stages.

-

A Lenders protect the stability of the system with low-risk borrowers.

-

B Lenders fill the gap for borrowers with unique situations who need more flexibility.

-

Private Lenders provide quick, equity-based solutions for those in urgent need.

For many homeowners, these levels work as stepping stones. You may start with a private lender during a difficult time, transition to a B lender as your finances improve, and eventually move back to an A lender for the lowest rates.

Key Takeaway

Understanding the 3 levels of mortgages in Canada—A lending, B lending, and private financing—empowers you to make the right financial decision based on your current situation.

-

If you’re financially stable with strong credit, A lending is the best choice.

-

If you need flexibility due to credit or income challenges, B lending can bridge the gap.

-

If you’re in urgent need or traditional lenders won’t approve you, private financing can provide fast, equity-driven solutions.

Final Thoughts

Choosing the right lender isn’t just about interest rates—it’s about finding a solution that matches your current financial reality and future goals.

Whether you’re buying your first home, refinancing, or trying to prevent foreclosure, understanding these three levels helps you take control of your options.

If you’re unsure where you fit—speak with a licensed mortgage broker. They can assess your credit, income, and equity to determine whether you should pursue an A, B, or private lender.

👉 At LendToday.ca, we specialize in helping Canadian homeowners find the right mortgage solution. Whether you need to refinance, consolidate debt, or access your home equity, we’ll walk you through the options and connect you with the right lender for your needs.

✅ Key Takeaway

3 levels of Mortgages – having a financial plan isn’t optional — it’s essential.

1. A Lenders (Prime Mortgages) Offer the lowest rates but has the strictest rules

2. B Lenders (Alternative Mortgages) More flexible, but come with higher rates and some fees

3. Private Lenders: Fast approvals, but the highest rates and short terms

- 7 Vital Facts About Secured Line of Credit Monthly Payments: A Complete Guide - February 11, 2026

- 12 Powerful Wins and Warnings: Our 2025 Year in Review on Mortgages, and Money - December 31, 2025

- Mortgage Co-Signer vs Guarantor in Canada: Expert Playbook to a Smarter Approval in 2025 - September 24, 2025