Divorce is one of life’s most emotionally and financially complex events. When a mortgage is involved, the stress can intensify. For Canadian homeowners going through separation, knowing your mortgage options is essential to protecting your finances, credit, and home. Whether you want to keep the house, sell and start fresh, or refinance to buy out your spouse, this guide breaks down the mortgage solutions available during a divorce.

Divorce doesn’t have to mean financial ruin. You have options — from spousal buyouts to refinancing and even selling your home. This guide walks you through how divorce impacts your mortgage, your credit, your income, and your ability to qualify for new financing.

The Financial Impact of Divorce on a Mortgage

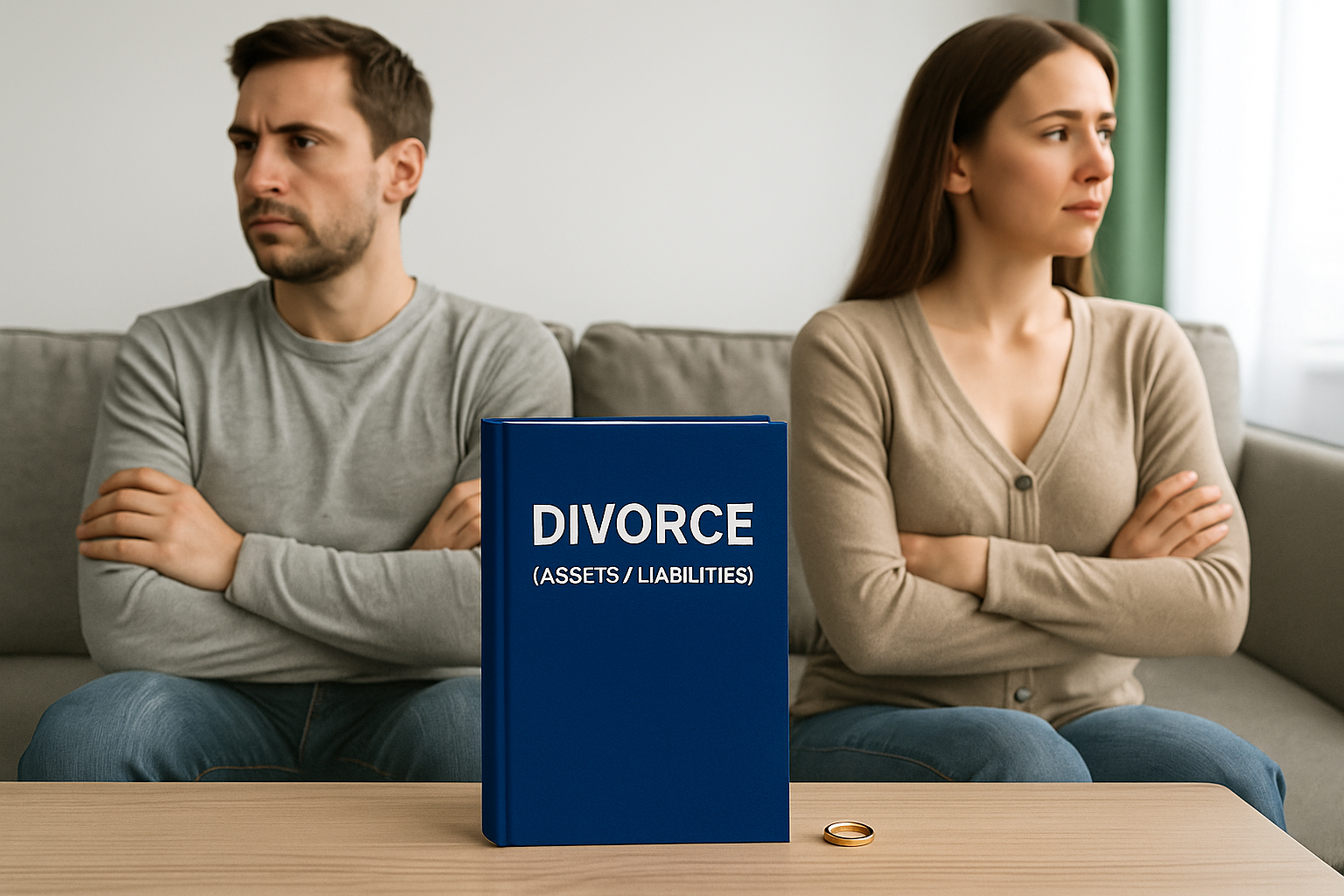

When a couple separates, the home and the mortgage tied to it are among the most significant shared financial obligations. In Canada, most couples have a joint mortgage, meaning both parties are legally responsible for the debt.

How Joint Mortgages Are Handled in a Separation

-

Both parties remain equally liable until the mortgage is refinanced or paid off.

-

You can’t simply remove a name from a mortgage without the lender’s approval.

-

One spouse can refinance the mortgage under a spousal buyout program to take over full responsibility.

What Happens to the Matrimonial Home?

There are typically three outcomes for the home during a divorce:

-

Sell the Home: The most straightforward solution. Both parties split the proceeds after paying off the mortgage and closing costs.

-

One Spouse Keeps the Home: Requires refinancing or a spousal buyout to remove the other’s name and settle their equity portion.

-

Deferred Sale: In rare cases (usually with young children), the couple may agree to defer the sale until a later date.

Key Takeaway: Lenders will require a formal separation agreement before making any changes to the mortgage. This is a legal document, not just a verbal agreement.

Mortgage Options Available During Divorce

Navigating mortgage solutions during a divorce depends on your income, credit score, available equity, and the legal agreement in place.

Option 1: Spousal Buyout Program

This is a unique refinance option available through some A lenders and B lenders:

-

Allows you to refinance up to 95% of the home’s appraised value.

-

The funds can be used to pay out your spouse’s share and settle joint debts.

-

Requires a signed separation agreement outlining the division of assets and debts.

-

The spouse taking over the home must qualify for the new mortgage alone.

Option 2: Sell the Home and Split the Equity

This is common in high-conflict divorces or where neither party can afford the home independently.

-

Proceeds from the sale go toward paying off the mortgage and shared debts.

-

Remaining equity is split as per the separation agreement.

-

Clean financial and emotional break.

Option 3: Refinance with a New Lender

If the original lender declines your refinance request, you can look to:

-

B-lenders (alternative lenders) who are more flexible on credit/income.

-

Private lenders who approve based on home equity rather than income or credit.

-

These solutions may come with higher rates but can offer short-term relief.

Important to Note: If you receive regular child support or spousal support, these can count toward your qualifying income with the right documentation.

Divorce Mortgage Solutions Compared

| Divorce Mortgage Solution | Best For | Key Requirements |

|---|---|---|

| Spousal Buyout Program | One party staying in the home | 95% LTV, signed separation agreement |

| Sell & Split Proceeds | Both parties moving on | Property sale, agreement on split |

| Refinance with New Lender | Credit/income changed post-divorce | Income proof, support documents |

| Private Mortgage or HELOC | Low credit score, urgent need | Equity (min 20%), legal documentation |

How Income, Debts, and Support Payments Affect Approval

Divorce doesn’t just affect your relationship — it changes your financial profile. Lenders will reassess your income, debts, and credit when considering your mortgage options.

Including Spousal and Child Support as Income

Lenders will accept spousal or child support payments if:

-

They’re documented in a formal separation agreement or court order.

-

You can show 3–6 months of consistent deposits into your account.

-

The support payments will continue for at least 3 more years.

Credit Score Impacts After Divorce

Divorce itself doesn’t appear on your credit report — but missed joint payments do.

-

One partner missing payments can damage both credit scores.

-

Separating finances early helps avoid long-term credit issues.

-

You may need to work with B-lenders or private lenders temporarily while rebuilding.

Handling Joint Debts and Liabilities

Common Mistake: Leaving joint credit cards or loans open post-separation.

-

Both parties remain liable, even if one uses the card.

-

Unpaid joint debts can ruin both credit profiles.

-

Refinancing the mortgage to pay off joint debts can be a smart solution.

Key Takeaway: Divorce is the time to review and restructure all debts — not just the mortgage.

Legal Documentation and Professional Help

Trying to manage everything on your own during a divorce is a recipe for financial chaos. Legal and professional support is critical when mortgages and property are involved.

Why a Separation Agreement is Crucial

A separation agreement outlines:

-

Who gets the home and other assets

-

Debt division (credit cards, lines of credit)

-

Support payment obligations

-

Parental responsibilities (if children are involved)

Lenders will not approve a spousal buyout or refinance without this document.

Appraisals and Title Transfers

-

Required if one spouse is keeping the home.

-

Cost ranges from $400–$600 for an appraisal in Canada.

-

Title transfer legal fees may cost $1,500–$3,000 depending on the province and complexity.

Role of a Mortgage Broker During Divorce

A mortgage broker helps by:

-

Reviewing lender options based on your new financial profile.

-

Helping with the spousal buyout or refinance paperwork.

-

Coordinating with your lawyer and real estate appraiser.

-

Explaining what lenders require and helping you qualify.

Important to Note: Brokers can also help both parties separately, even if one is staying and one is purchasing elsewhere.

Mortgage Solutions if You Have Bad Credit

Divorce often brings credit strain, especially if payments are missed during emotional times. Fortunately, lenders in Canada offer options for those with less-than-perfect credit.

-

Private lenders and B-lenders focus more on equity than credit score.

-

If you have at least 20% equity, you may qualify for a second mortgage or HELOC.

-

These can be used to pay out a spouse, consolidate debts, or transition to a new home.

Checklist to Qualify for Mortgage After Divorce:

| ✅ Checklist Item | 🔍 How To Do It |

|---|---|

| Review your credit score and correct any errors | Use Equifax or TransUnion to download your report and dispute mistakes |

| Finalize your separation agreement | Have it prepared by a lawyer — lenders require a formal legal doc |

| Get an updated home appraisal | Book a licensed appraiser for an accurate market value |

| Gather proof of income and support payments | Include pay stubs, NOAs (notice of assessments), and 3–6 months of support deposits |

| Work with a mortgage broker | Choose one with experience in divorce and home equity lending |

Common Myth: Bad credit means no options — in reality, equity-based lenders help thousands of divorced Canadians each year.

Long-Term Considerations After Divorce

Even after the dust settles, managing your home and finances post-divorce requires careful planning.

-

Rebuild your credit by making consistent payments and limiting new debts.

-

If moving, consider portable mortgages or assumption clauses.

-

Create a new household budget to reflect your single-income reality.

-

Keep track of your home equity for future needs, such as renovations or your children’s education.

Common Mistake: Rushing into another mortgage or home purchase without planning. Take the time to recover financially and emotionally.

FAQ Section

Q: Can I qualify for a mortgage after a divorce in Canada?

A: Yes. If you have enough income (from employment and support), equity in the home, and a formal separation agreement, many lenders will work with you — even if your credit is bruised.

Q: What happens to our joint mortgage during a divorce?

A: You are both liable for the mortgage until it’s paid out, refinanced, or assumed by one party. A separation agreement is essential to outline the next steps and avoid future issues.

Q: Can spousal or child support help me qualify for a mortgage?

A: Absolutely. If support payments are consistent and documented for at least 3 months, lenders often consider them part of your qualifying income. Court-ordered payments are generally mandatory.

Q: Do I need a lawyer to refinance during a divorce?

A: Yes. Any mortgage transaction tied to a divorce — including a spousal buyout — must be handled by a licensed real estate lawyer.

Q: What if my credit score dropped during the separation?

A: Lenders like B-lenders and private lenders often approve based on home equity, not credit score. A mortgage broker can match you with the right solution.

- Want to Pay Off Your Mortgage Faster? Here’s Exactly How to Do It - May 5, 2026

- Insured Mortgage, Uninsured Mortgage, Insurable Mortgage: Which Category Are You In? - April 28, 2026

- Hard Money Lender Alberta: Guide for Homeowners in 2026 - February 26, 2026