Online mortgage payment calculators are an invaluable tool providing a fast and effortless means of determining your potential mortgage payments. These calculators effortlessly churn out the figures you need with just a few clicks.

Yet have you ever wondered how to calculate mortgage payments? How exactly do they arrive at that specific payment amount? In this blog, we’ll discuss how to calculate mortgage payments to understand the rationale behind your unique payment amount.

What Goes into a Monthly Mortgage Payment?

Depending on your initial down payment, your total monthly mortgage payment includes three distinct expenditures, each playing a crucial role in shaping the overall financial arrangement:

1. Principal

The principal amount is at the core of your mortgage payment – the original sum you borrowed to secure your home. Imagine acquiring a residence worth $400,000, and your down payment is $50,000. In this scenario, the principal sum would stand at $350,000, forming the foundation of your financial commitment.

2. Interest

In exchange for extending the financial aid that facilitates your home purchase, lenders levy interest. The prevailing mortgage interest rates wield substantial influence over the dynamics of your long-term mortgage. The interplay of principal and interest defines the fundamental structure of your monthly payment.

3. Mortgage Default Insurance

For individuals whose down payments fall below 20% of the property’s purchase price, acquiring mortgage default insurance becomes obligatory. This insurance safeguards lenders in case of default, providing them with a safety net.

Notably, the mortgage default premium integrates into the principal, effectively making it part of the principal amount on which interest accrues.

Different Types of Mortgage Payments

In Canadian mortgages, borrowers are presented with various payment options tailored to specific financial circumstances. These options include:

1. Fixed-Rate Mortgage Payments

A fixed-rate mortgage introduces stability by maintaining a consistent interest rate and unvarying monthly payments throughout the mortgage term. Borrowers benefit from predictability, enabling effective budgeting and financial planning.

2. Adjustable-Rate Mortgage Payments

Adjustable-rate mortgages usher in market sensitivity, as interest rates and monthly payments may ebb and flow in tandem with shifts in the market or the Bank of Canada’s overnight rates. While potentially offering flexibility, this mortgage type exposes borrowers to the possibility of higher payments if interest rates climb.

3. Variable-Rate Mortgage Payments

Similar to adjustable-rate mortgages, variable-rate mortgages embrace fluctuating interest rates. However, the stability of monthly payments remains intact, with alterations in interest rates impacting on the proportion of principal repaid each month.

4. Interest-Only Mortgage Payments

Interest-only mortgages permit borrowers to solely pay the interest on the loan for a designated period, usually spanning up to a decade. While facilitating lower initial payments, this option holds long-term risk, as it does not chip away at the principal loan balance.

5. Bi-weekly or Accelerated Mortgage Payments

Bi-weekly and accelerated payment schemes redefine the conventional monthly rhythm. Bi-weekly payments split the monthly obligation into two smaller installments, disbursed every two weeks.

On the other hand, accelerated payments involve exceeding the minimum payment requirements, an approach that expedites mortgage payoff and curtails interest expenses.

What You’ll Need to Calculate Your Mortgage Payments

Before you start calculating, collect these crucial details and have a simple calculator on hand. Note that this formula is specific to monthly mortgage payments and doesn’t apply to bi-weekly or accelerated bi-weekly plans.

The three essential data points needed on how to calculate mortgage interest:

1. Mortgage Principal

This denotes the entirety of your borrowed amount. Compute the mortgage principal by subtracting your down payment from the total home purchase price.

For instance, if your down payment for a $600,000 home is $120,000, your mortgage principal becomes $480,000. With every payment cycle, portions address the principal while others manage interest.

Mortgage principal = purchase price – down payment

Mortgage principal = $600,000 – $120,000

Mortgage principal = $480,000

2. Monthly Interest Rate

Since lenders often stipulate annual interest rates, transform them into a monthly equivalent by dividing the annual rate by 12. Convert the percentage to a decimal and divide it by 12 to acquire a manageable monthly interest rate, which is crucial for the mortgage payment formula.

Monthly interest rate = annual interest (%) / 100 / 12 months

Monthly interest rate = 2.69 / 100 / 12

Monthly interest rate = 0.00224

3. Payment Period Count

This corresponds to the total mortgage payments needed for complete repayment, contingent upon the amortization period. Distinguish between amortization period (loan duration) and mortgage term (contract duration).

While lenders commonly offer amortization periods of five to 25 years, numerous mortgage terms might be undertaken before complete repayment.

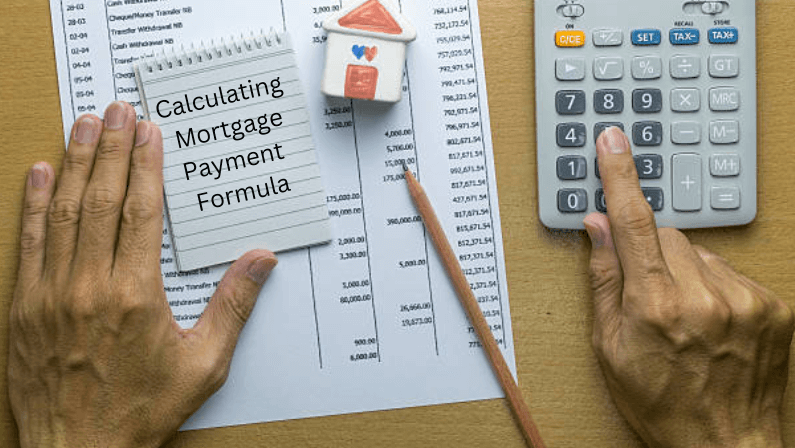

Using The Mortgage Payment Formula to Calculate Mortgage Payments

For clarity on how to calculate your mortgage payments, we’ve attributed symbols to the inputs in the formula.

Here’s how you manually calculate mortgage payment:

Monthly payment = P x (I x (1+ I)^N ) / ((1 + I)^N – 1)

Where:

P = Mortgage principal

I = Monthly interest rate

N = Number of payment periods

Substitute the symbols with your own figures and execute the calculation following these steps:

1. Calculate the inner parentheses first, adhering to PEMDAS rules (parentheses, exponents, multiplication, division, addition, and subtraction).

2. Compute the exponents (^), signifying a series of multiplications.

3. Complete the remaining multiplications and divisions.

For example, suppose you’re considering a $600,000 home with a 20% down payment ($120,000), amortized over 25 years at a 2.69% rate. Given these inputs:

P = 480,000 I = 0.00224 N = 300

Substitute these into the equation:

Monthly payment = P x (I x (1+ I)^N ) / ((1 + I)^N – 1)

Monthly payment = 480,000 x (0.00224 x (1 + 0.00224)^300) / ((1+0.00224)^300 – 1)

Monthly payment = 480,000 x (0.00224 x 1.00224^300) / (1.00224^300 – 1)

Monthly payment = 480,000 x (0.00224 x 1.95667) / (1.95667 – 1)

Monthly payment = 480,000 x 0.00438 / 0.95667

Monthly payment = 2,102.4 / 0.95667 Monthly payment = 2,197.62

The result, $2,197.62, signifies your monthly mortgage payment amount. While inputting the same details into a mortgage payment calculator may yield a slightly different outcome, due to rounding, remember that varying the number of decimal points can lead to divergent results that might not exactly align with calculator outputs.

Factors that Can Affect Your Mortgage Payments

Calculating mortgage payments involves navigating a landscape influenced by several pivotal elements, each molding the size of your financial commitment.

The following key factors shape mortgage payment calculation:

1. Home Price

The cornerstone of your mortgage calculation, the price of your home determines the borrowing amount needed.

2. Down Payment

Your upfront investment towards the home purchase influences the magnitude of the required mortgage, subsequently affecting the size of monthly payments.

3. Total Mortgage Amount

This encompasses the home’s price minus the down payment, potentially incorporating mortgage insurance if applicable.

4. Interest Rate

The interest rate attached to your mortgage significantly impacts monthly payments. Lower rates translate to reduced payments, with LendToday’s expertise in locating favorable rates to optimize your financial standing.

5. Amortization Period

The timeline for repaying your mortgage—the amortization period—affects your monthly commitment. Longer periods result in lower payments, but extended repayment may lead to higher interest costs over time.

At LendToday, we expertly recognize these factors to tailor offers and methods that match your unique financial circumstance.

How to Pay Off Your Mortgage Faster

Paying off your mortgage faster has compelling advantages, such as reducing interest payments and gaining financial independence sooner.

There are three effective strategies to expedite your mortgage pay-down, each offering distinct benefits:

1. Make Lump-Sum Payments

Consider making lump-sum payments to your mortgage principal. Open mortgages allow unlimited prepayments, while closed mortgages often permit an annual additional payment of 10-20% of your original balance.

2. Increase Monthly Payments

Explore increasing your monthly payments to steadily diminish your outstanding mortgage balance. Be mindful of the yearly percentage limit set by lenders to avoid penalties.

3. Opt for More Frequent Payments

Choosing smaller, more frequent payments can expedite your mortgage balance reduction. This approach can effectively translate to an extra payment annually.

Consider these payment scenarios for a $500,000 mortgage with a 25-year term and 5% interest:

- Monthly: $2,989 payment, $382,835 total interest.

- Bi-weekly: $1,378 payment, $381,841 total interest.

- Semi-monthly: $1,493 payment, $381,912 total interest.

- Weekly: $689 payment, $381,416 total interest.

To delve into personalized payoff strategies and explore your best options, consult with LendToday. Their expertise can guide you towards achieving mortgage freedom sooner, saving you both time and money.

Ways to Reduce Your Monthly Mortgage Payment

When seeking avenues to alleviate the weight of your monthly mortgage payment, a range of effective strategies is at your disposal.

Key tactics to consider include:

1. Rate Comparison Among Lenders

The variance in interest rates across lenders can significantly impact on your monthly payment. By meticulously comparing rates, even a fractional difference can yield substantial savings over your mortgage term.

2. Amplify Your Down Payment

Bolstering your initial down payment reduces your borrowing amount, translating to decreased interest payments and potential opportunities for a better interest rate. Elevating your equity position positions you as a more favorable prospect for lenders, paving the way for lower payments.

3. Extend Amortization Period

Opting for a lengthier amortization period translates to smaller monthly payments, although it might accrue more interest over the mortgage’s lifespan. This approach can benefit homeowners on a tight budget, offering financial flexibility without compromising homeownership.

4. Refinancing Insights

Refinancing can be invaluable for established homeowners with robust credit histories and consistent mortgage payments. LendToday facilitates the refinancing process, effectively commencing a new mortgage that could secure a reduced interest rate and fresh payment structure—potentially alleviating the monthly financial load.

Does the Mortgage Stress Test Affect My Monthly Mortgage Payment?

The mortgage stress test is crucial in determining your feasible mortgage amount, consequently influencing your monthly payment size. Guided by specific regulations, this test mandates that you qualify for a mortgage at 5.25% or the rate offered to you plus 2%, whichever is higher.

For instance, if offered a 5% rate, you must demonstrate the ability to handle the mortgage at 7% for approval. When the stress test isn’t met, lenders adjust the mortgage amount until compliance is achieved.

How Does My Salary Impact My Mortgage Payment?

The size of your mortgage offer hinges on your income, a critical element shaping your borrowing capacity. Lenders gauge your capability to manage a substantial monthly mortgage payment by evaluating whether your income adequately covers essential expenses and debts, leaving a surplus.

A higher salary instills lender confidence in managing larger mortgage payments. Conversely, a smaller income might lead to a reduced mortgage offer and consequently smaller monthly payments, aligning your financial capacity with your mortgage commitment.

How Does Adjusting Your Amortization Period Impact Your Calculation and Budget

Commonly spanning 20 to 30 years, the standard amortization period molds mortgage terms to your budget. The flexibility of adjusting this period within a mortgage payment calculator unveils its substantial impact on monthly payments and the cumulative interest outlay throughout the loan’s duration.

While recalibrating, matching your budget with your financial aspirations is vital to ensure an informed choice aligned with your overarching goals.

Can First-time Home Buyers Get Help with their Mortgage Payments?

First-time home buyers in Canada can access various programs to enhance their down payment savings. Initiatives such as the Home Buyers’ Plan and the First Home Savings Account facilitate accumulating a larger down payment.

Leveraging these programs can prove instrumental in realizing homeownership aspirations and optimizing affordability throughout the mortgage term.

Are Closing Costs Part of a Mortgage Payment?

A comprehensive comprehension of mortgage payments necessitates discerning the distinct elements they encompass. While a mortgage payment ordinarily factors in the principal, interest, and mortgage default insurance, ancillary expenses like:

- Commissions

- Land transfer taxes

- Legal fees

Demand separate disbursement. These costs, intrinsic to property transactions, remain outside the purview of regular mortgage payments, requiring distinct attention in your financial planning.

Empower Yourself with The Knowledge to Make Informed Financial Decisions

A mortgage is a significant financial commitment, and understanding how your monthly payments are calculated is crucial for effective financial planning.

LendToday is ready to provide expert guidance, ensuring your mortgage decisions align seamlessly with your financial goals. Empower yourself with knowledge and embark on your homeownership journey confidently.