Buying a Home in Ontario? Here’s What You Need to Know

Buying a home is one of the most significant financial decisions you’ll make, especially in Ontario’s competitive housing market. Whether you’re a first-time buyer or upgrading, getting your mortgage application right is essential. A strong home purchase strategy means knowing what documents you need, how to qualify, when to get pre-approved, and how to avoid costly mistakes.

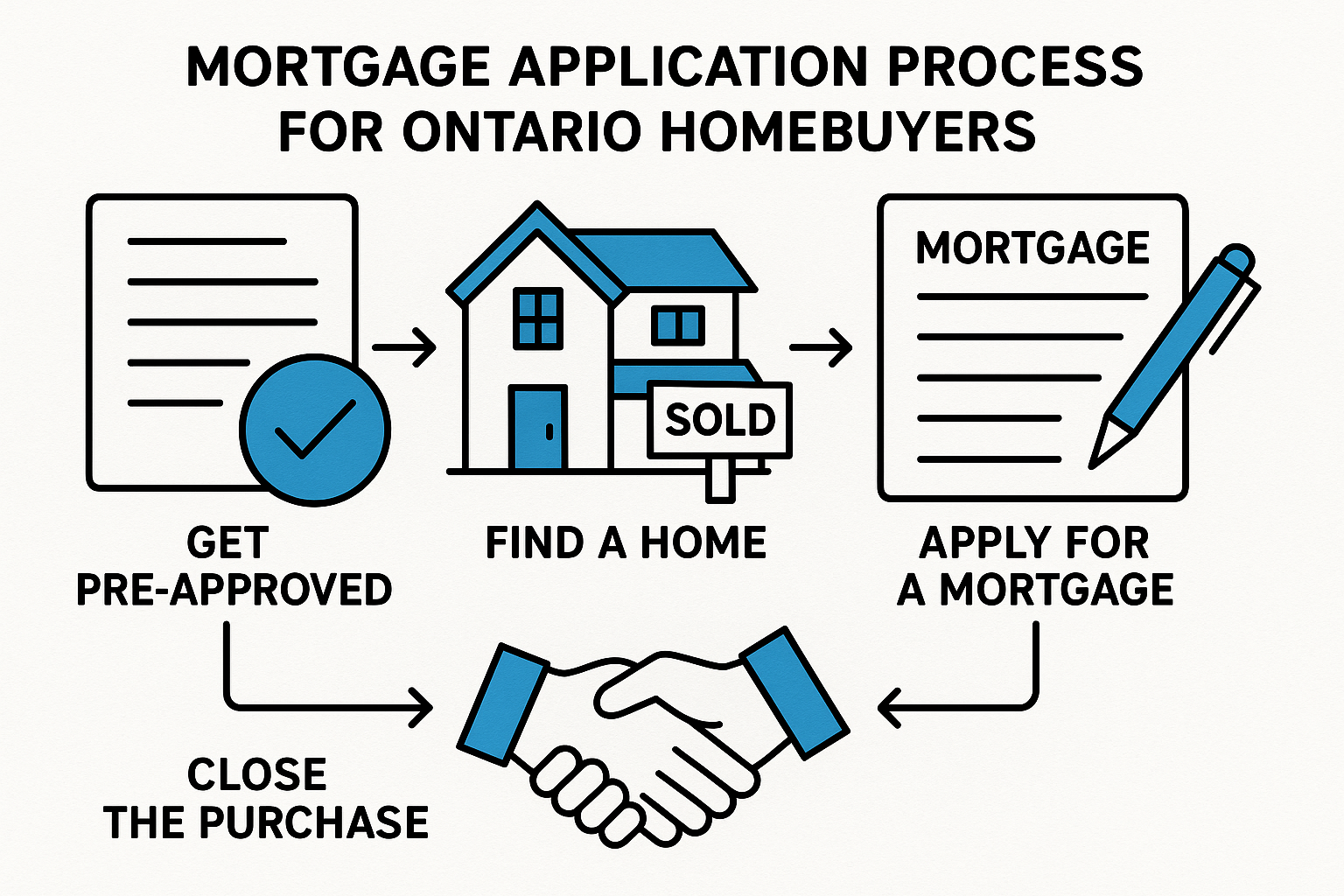

This guide walks you through everything you need to successfully apply for a mortgage—from organizing your paperwork to working with the right professionals. Let’s dive into the best practices for a smooth, stress-free home purchase.

Step 1 – Understand the Mortgage Application Process in Ontario

What Is a Mortgage Application?

A mortgage application is your formal request to borrow money for a home purchase. In Ontario, it includes a review of your income, assets, debts, credit score, and the property details. Your lender—whether a bank, credit union, or mortgage broker—uses this to determine if you’re eligible and how much they’re willing to lend.

Why It Matters for a Home Purchase

Your mortgage application sets the tone for the entire transaction. Lenders assess your financial stability and the property’s value. A solid application can speed up your approval and help avoid delays that risk your home purchase falling through.

Step 2 – Get Pre-Approved Early

What a Pre-Approval Includes

A mortgage pre-approval is a preliminary assessment of your financial standing.

It includes:

-

Credit check

-

Income and employment review

-

Review of your down payment sources

-

Estimated maximum purchase price

Most pre-approvals are valid for 90 to 120 days.

Benefits of a Pre-Approval

-

Confidence: Know how much home you can afford.

-

Interest Rate Lock: Protect yourself from rising rates.

-

Stronger Offers: Sellers view you as a serious, qualified buyer.

Key takeaway: Pre-approval doesn’t guarantee funding, but it gives you a huge advantage in a fast-moving market.

Step 3 – Prepare Your Mortgage Application Documents

Must-Have Mortgage Documents Checklist

You’ll need to provide several documents for your mortgage application, including:

-

Government-issued photo ID (2 pieces of valid ID)

-

Pay stubs (most recent 2 within 30 days)

-

T4 slips and Notice of Assessment (last 2 years)

-

Employment letter (within 30 days)

-

Bank statements (last 90 days)

-

Down payment proof (gift letter if applicable)

-

Property MLS listing, purchase agreement and all schedules (once available)

-

Details on other properties (if applicable)

📋 Mortgage Application Document Checklist

| Document Type | Purpose | Notes |

|---|---|---|

| ID | Identity verification | Must be valid, unexpired |

| Income Proof | Show earnings | 2 years of stable income preferred |

| Bank Statements | Verify down payment | Must show full account history |

| Credit Report | Show creditworthiness | May be pulled by lender or broker |

🚩🚩🚩Common mistake: Sending incomplete documents or screenshots instead of full PDFs delays your approval and weakens your application.

Step 4 – Boost Your Mortgage Qualifying Power

Improve Your Credit Score

Lenders want to see a good repayment history. If your score is below 680, it might limit your mortgage options.

Improve your credit by:

-

Paying off outstanding balances

-

Reducing credit utilization to below 35% of the limit

-

Avoiding new credit applications

-

Checking for and fixing credit report errors on Equifax or TransUnion

Reduce Your Debt-to-Income Ratio

This ratio compares your monthly debt obligations to your income. A high ratio can hurt your ability to qualify.

-

Pay off high-interest loans

-

Avoid financing large purchases like cars before your mortgage closes

Increase Your Down Payment

Putting more money down lowers your loan-to-value ratio and reduces risk to the lender.

-

Use RRSPs under the First-Time Home Buyer’s Plan

-

Save aggressively for a few months

-

Consider gifted funds (with a proper gift letter)

Important to note: A larger down payment also reduces or eliminates CMHC insurance premiums.

Step 5 – Choose the Right Mortgage Option

Compare Interest Rates & Lenders

Every mortgage application should include comparison shopping. Look at:

-

Fixed vs Variable Interest Rates

-

Penalties for breaking the mortgage early

-

Portability and prepayment privileges

-

Lender flexibility on income types or bruised credit

You can choose between:

-

A Lenders (Banks & Credit Unions): Best for strong credit/income

-

B Lenders (Alternative Lenders): Higher risk tolerance, higher rates

-

Private Lenders: Focused on equity and home value more than income

Common myth: The lowest rate is always the best deal. Not true—read the fine print.

While a low interest rate may look appealing at first glance, it often comes with restrictions that can cost you more in the long run. Many ultra-low-rate mortgages limit your flexibility when it comes to important features such as:

-

Prepayment privileges: The ability to make lump-sum payments or increase your regular payment amount without penalty.

-

Portability: Whether you can transfer your mortgage to a new home without breaking the contract (which can save you thousands in penalties).

-

Penalty structure: The cost of breaking your mortgage early—some low-rate products have significantly higher penalties.

-

Blend and extend options: Flexibility to change your mortgage mid-term if interest rates drop.

Know Your Term and Amortization Options

Most Ontario buyers go with:

-

5-year fixed term

-

25-year amortization

But your situation might call for a variable rate or a shorter/longer term. Work with a broker to weigh your options and develop a plan.

Step 6 – Finalize the Purchase & Close Your Mortgage

Conditional Offer and Financing Approval

When submitting an offer on a home, it’s strongly recommended to include a financing condition—even if you’re already pre-approved.

Why? A pre-approval only verifies your financial situation; it doesn’t guarantee that the lender will approve the specific property or provide final mortgage funding. A financing condition gives you the time and legal right to back out of the deal if something doesn’t line up.

What the financing condition allows you to do:

-

Finalize your mortgage application

-

Get the lender’s approval on the property

-

Complete any required appraisal, title review, or documentation

-

Make adjustments if interest rates, qualifying terms, or income validation change unexpectedly

Industry standard is 5 business days for a financing condition, but that’s often not enough.

Important to note:

Lenders and mortgage brokers may be managing high volumes of applications, especially in peak seasons. Processing delays can happen due to appraisals, document verification, or legal requirements. Try to negotiate for a longer financing condition period if possible—as long as the seller is willing to accept it.

Key takeaway: A financing condition protects you. Don’t waive it unless you’re fully confident your mortgage is approved and unconditional.

Work With a Real Estate Lawyer (Not Just Any Lawyer)

When buying a home in Ontario, it’s important to hire a real estate lawyer, not just any general practice lawyer.

Why it matters:

Real estate law is highly specialized. A lawyer who doesn’t regularly deal with property transactions may miss key details or misunderstand compliance issues tied to your mortgage application or property title. Mistakes can cause delays, missed deadlines, or even legal disputes post-closing.

A real estate lawyer will:

-

Review the purchase agreement to ensure it protects your interests

-

Confirm the title and property boundaries, checking for liens, easements, or encroachments

-

Register your mortgage properly with the provincial land registry

-

Set up title insurance, which is required by all lenders and protects against fraud or title defects

Important to note: Many law firms specialize only in family, corporate, or civil law. Be sure to confirm that the lawyer you hire handles real estate closings regularly and is insured for real estate transactions.

Appraisal and Final Approval

Your lender might order a home appraisal to confirm value. If the home appraises low, you may need to come up with the difference out of pocket; this is known as a shortfall.

Important to note: The appraisal must be conducted by a third-party accredited appraiser or appraisal firm. Most lenders in Ontario have a pre-approved list of residential and commercial appraisers they accept reports from. A realtor’s opinion of value or CMA (Comparative Market Analysis) will not be accepted by the lender under any circumstances.

Once all conditions are satisfied, and the lender approves both your application and the property:

-

The lender works with your real estate lawyer to release the mortgage funds for closing.

-

Your mortgage professional does not handle or disburse funds—that responsibility lies with your lawyer, who manages the transaction through their trust account on closing day.

FAQ: Home Purchase Mortgage Application in Ontario

Q: What credit score do I need to qualify for a mortgage in Ontario?

A: Typically, lenders look for a credit score of 680+ for prime rates. But some lenders work with clients who have bruised credit and consider other factors like equity or income.

Q: How long does a mortgage application take?

A: A pre-approval can be issued within 1–3 days. Once you have a signed offer, final approval usually takes 5–10 business days, depending on the complexity and responsiveness of the borrower.

Q: Do I need a pre-approval to buy a home?

A: It’s not required, but it’s strongly recommended. A pre-approval shows sellers you’re serious and qualified, and it helps you shop within your actual budget.

Q: What happens if I’m self-employed?

A: You’ll need to provide 2 years of Notice of Assessments, financial statements, and potentially 6–12 months of bank statements. Some lenders offer stated income products, especially for incorporated individuals.

Q: Can I include a co-signer on my application?

A: Yes. A co-signer with strong credit and income can help strengthen your mortgage application if your income or credit alone is not sufficient to qualify.

Q: Should I put a financing condition in my offer to purchase?

A: Yes, you should. A financing condition protects you as the buyer in case your final mortgage approval falls through. It gives you the right to back out of the deal without penalty if your financing isn’t confirmed.

Final Thoughts: Secure Your Home Purchase With a Smart Mortgage Application

A strong mortgage application is the foundation of a successful home purchase. In Ontario’s fast-paced market, preparation is key. Get pre-approved, organize your documents, improve your financial profile, and work with professionals who understand your unique situation.

Key takeaway: Don’t wait until you’ve found the perfect home to start your mortgage process. Plan ahead, stay informed, and give yourself the best chance of approval.

- Hard Money Lender Alberta: Guide for Homeowners in 2026 - February 26, 2026

- How Many Paystubs Are Required for a Mortgage in Canada? Helpful Guide - February 19, 2026

- Home Insurance Requirements for a Mortgage in Canada - February 13, 2026