Understanding the Basics

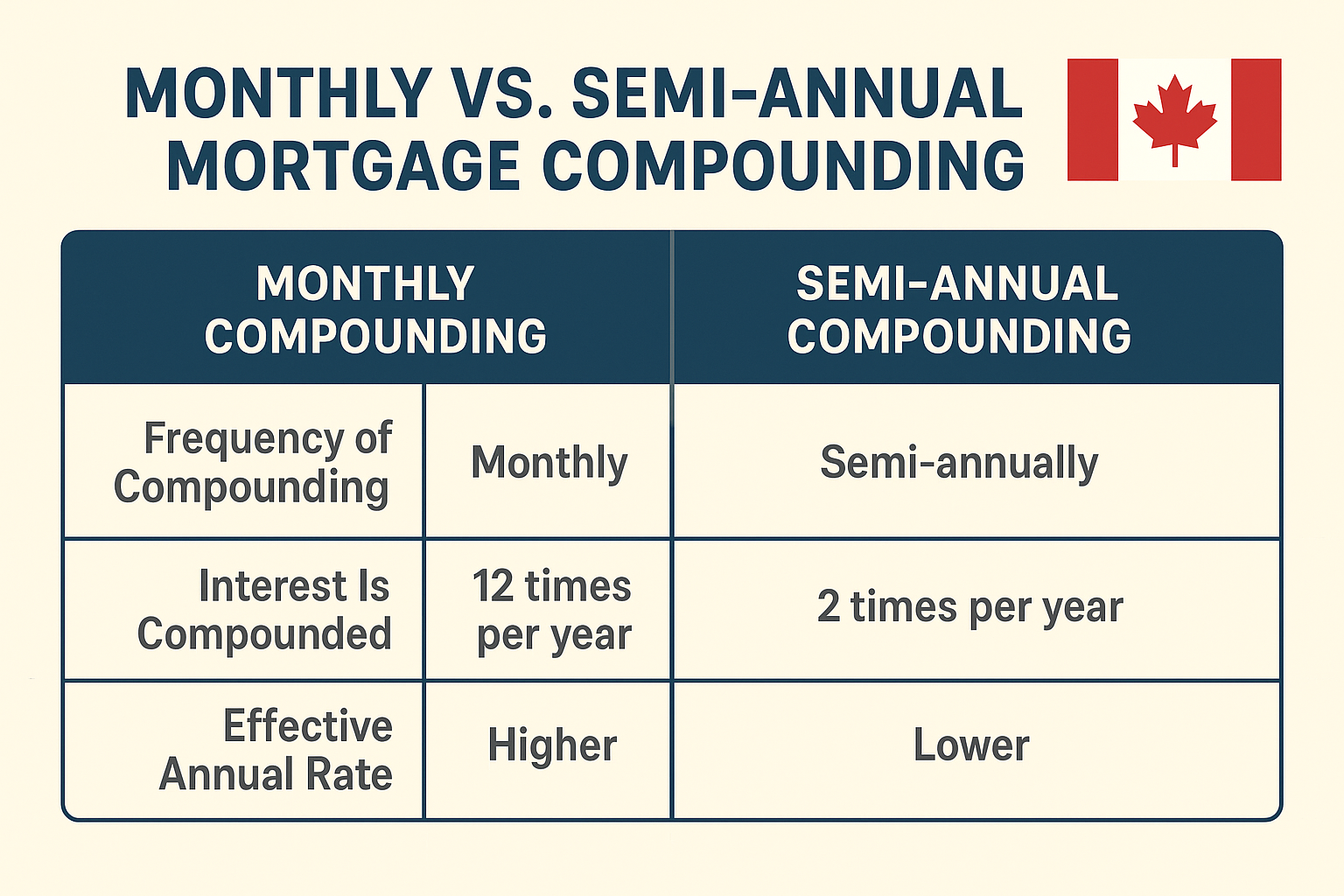

When it comes to mortgage payments in Canada, one factor many borrowers overlook is how often their interest is compounded. Most Canadian fixed-rate mortgages are compounded semi-annually, meaning interest is added to the loan twice per year. However, some mortgages—especially variable-rate or private ones—may be compounded monthly.

This difference affects how much total interest you pay over time. Even if the mortgage rate looks the same, how it’s compounded can significantly impact your bottom line. In this article, we’ll break down what monthly and semi-annual compounding mean, how they work in Canada, and what homeowners need to watch out for.

What Does “Compounded” Mean in Mortgage Payments?

Understanding Compound Interest

Compound interest means you’re being charged interest on your interest. Unlike simple interest, which only applies to the principal, compound interest accumulates based on your balance, including previously accrued interest.

-

If a mortgage is compounded monthly, interest is calculated and added 12 times a year.

-

If it’s compounded semi-annually, it’s calculated twice a year, leading to a slower accumulation.

Common Myth: More Frequent Compounding Always Saves Money

Many borrowers assume that more frequent compounding (like monthly) is always better. That’s not always true. While frequent compounding can lead to smaller incremental interest additions, it can also result in higher overall interest depending on your mortgage type, term, and rate.

Monthly Compounding Explained

How Monthly Compounding Works

When your interest is compounded monthly, your mortgage balance increases every month based on the interest accrued. For example, if you have a mortgage rate of 6.00% compounded monthly, the effective annual rate (EAR) ends up slightly higher than 6.00% due to monthly compounding.

Lenders That Offer Monthly Compounding

-

Monthly compounding is rare in Canada for fixed mortgages.

-

Some private lenders or alternative lenders (B lenders) will use it.

-

Variable-rate mortgages may also feature monthly compounding.

Pros and Cons

Pros:

-

Interest calculation aligns with payment frequency.

-

Easier to track interest accrual.

Cons:

-

Higher effective interest rate.

-

Can lead to more total interest paid compared to semi-annual compounding.

Semi-Annual Compounding Explained

How It Works in Canada

In Canada, it is standard practice for fixed-rate mortgages to be compounded semi-annually, meaning interest is added to the mortgage twice per year. This structure is dictated by federal regulations for financial institutions.

Key Takeaway: This is the Default in Canada

According to the Bank Act, Canadian lenders must compound interest twice a year for fixed mortgages, even if payments are made monthly. This distinction often confuses borrowers who assume monthly payments mean monthly compounding.

Pros and Cons

Pros:

-

Lower effective annual interest rate compared to monthly compounding.

-

Easier to compare fixed rates across Canadian lenders.

Cons:

-

Not aligned with monthly payments, which can confuse borrowers.

-

Still results in compounding, just less frequently.

Key Differences Between Monthly and Semi-Annual Compounding

Effective Annual Rate (EAR) Impact

Let’s look at a side-by-side example.

| Details | Compounded Monthly | Compounded Semi-Annually |

|---|---|---|

| Mortgage Amount | $500,000 | $500,000 |

| Interest Rate | 5.99% | 5.99% |

| Amortization | 25 Years | 25 Years |

| Monthly Payment | $3,168 | $3,143 |

| Total Interest (Over 25 Yrs) | $450,479 | $442,786 |

| Difference | +$7,693 | — |

Key takeaway: A small difference in compounding can result in thousands of dollars in added interest over time.

Long-Term Cost Comparison

-

Monthly compounding may seem better due to more frequent calculation, but often results in a higher overall cost.

-

Semi-annual compounding is often more cost-effective under the same nominal rate.

-

Always ask your lender: “What is the compounding frequency?”

Which Compounding Method Is Better for You?

Common Mistake: Focusing Only on the Rate

Many Canadians focus solely on the advertised mortgage rate and ignore how that rate is compounded. That’s a mistake. A mortgage at 6.00% compounded monthly is not the same as 6.00% compounded semi-annually.

Questions to Ask Your Broker or Lender

-

Is this mortgage compounded monthly or semi-annually?

-

What’s the effective interest rate (APR)?

-

Are there prepayment penalties or conversion restrictions?

-

What’s the total cost over the term?

How to Calculate Compounded Interest on Your Mortgage

The Formula (Simplified)

To estimate your total interest with compounding:

A = P(1 + r/n)^(nt)

Where:

-

A = amount owed (including interest)

-

P = principal

-

r = annual interest rate (decimal)

-

n = number of compounding periods/year

-

t = total years

Example:

$500,000 at 5.99% compounded monthly over 1 year

A = 500,000(1 + 0.0599/12)^(12×1)

A = ~$530,757.55

Important to note: Online mortgage calculators can do this automatically. Use a Canadian-specific calculator for accurate results.

Title Insurers & Compounding Schedules

While title insurance typically focuses on legal ownership and fraud protection, some title insurers or lawyers may flag mismatches in interest structures (e.g., monthly vs semi-annually compounded loans) during a mortgage refinance or transfer.

Important to note: You may be required to show government-issued ID when finalizing such transactions.

Example: Sarah & Tom’s Mortgage Journey

Scenario:

-

Sarah and Tom from Guelph, ON took out a $500,000 mortgage at 5.49%, compounded semi-annually.

-

A private lender offered them a similar rate—5.49%—but compounded monthly.

At first glance, they thought both offers were equal. But after reviewing total cost over a 5-year term, the monthly compounded option cost them over $3,100 more in interest.

Key takeaway: Even the same rate can cost more based on how it’s compounded.

Frequently Asked Questions (FAQ)

Q: What does “compounded semi-annually” mean in a Canadian mortgage?

A: It means the lender calculates and adds interest to your mortgage twice a year. This is standard for most fixed-rate mortgages in Canada due to regulatory requirements.

Q: Can I choose how my mortgage interest is compounded?

A: Usually not. Canadian regulations dictate that fixed-rate mortgages be compounded semi-annually. However, some variable-rate or private loans may offer different compounding structures.

Q: Does monthly compounding save more money in the long run?

A: Not always. Although it seems more frequent is better, it can actually result in higher effective interest and cost more over time.

Q: Why is semi-annual compounding standard in Canada?

A: It’s required by the Bank Act for consumer protection and consistency across lenders.

Q: Is compounding the same as how often I make payments?

A: No. You might make monthly payments while still having semi-annual compounding, which is common in Canada.

Final Thoughts: Compounded Interest Matters More Than You Think

When comparing mortgage payments, Canadian homeowners must look beyond the interest rate. The compounding frequency—whether monthly or semi-annually—has a direct impact on how much interest you pay over time.

Key takeaway: Ask your mortgage broker or lender about the compounding method used, and request an amortization schedule to see the numbers in action. What seems like a small difference could cost thousands over the life of your mortgage.

Learn More About Payments & Compounding

- Hard Money Lender Alberta: Guide for Homeowners in 2026 - February 26, 2026

- How Many Paystubs Are Required for a Mortgage in Canada? Helpful Guide - February 19, 2026

- Home Insurance Requirements for a Mortgage in Canada - February 13, 2026