Mortgage Stress Test in 2025: What Changed?

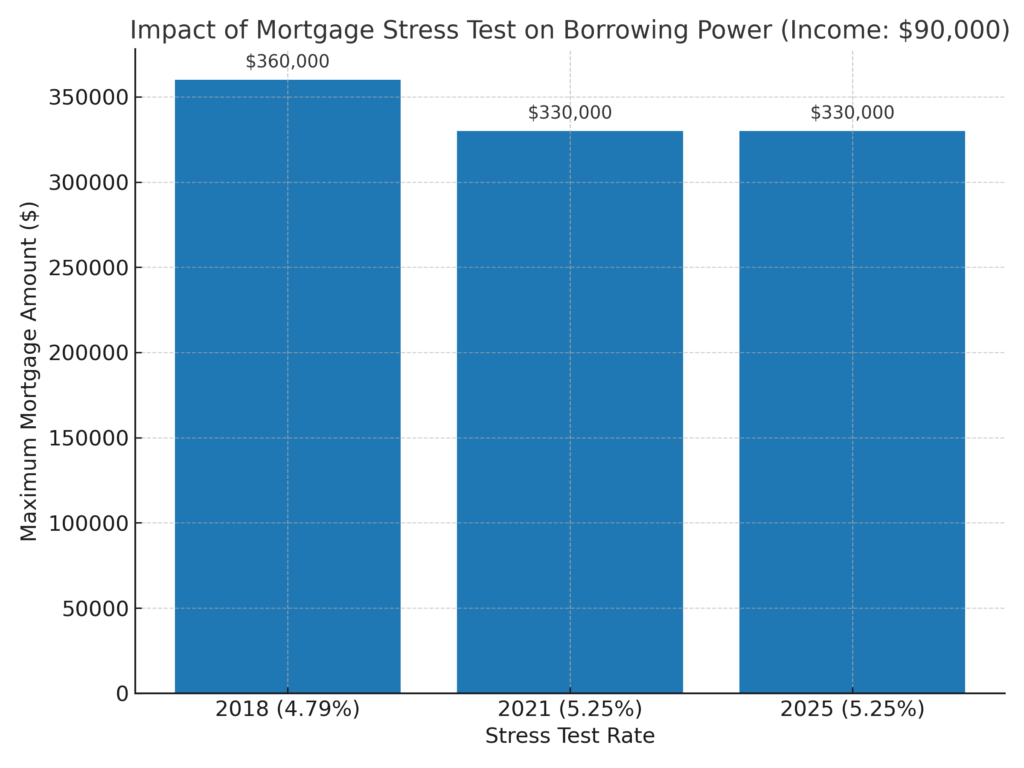

Back in January 2018, the Canadian government introduced the mortgage stress test to ensure borrowers could still afford their homes even if interest rates rose in the future.

-

In 2018, the qualifying rate was 4.79%.

-

In June 2021, it increased to 5.25%.

-

As of 2025, the benchmark remains at 5.25%.

That means even if your lender offers you a 4.5% mortgage, you must prove you can afford payments at 5.25% (or your contract rate + 2%, whichever is higher).

How the Mortgage Stress Test Works

The test requires you to qualify for your mortgage at the greater of:

-

The Bank of Canada’s benchmark qualifying rate (currently 5.25%).

-

Your contract rate + 2%.

For example:

| Mortgage Rate Offered | Stress Test Applied | Rate You Must Qualify At |

|---|---|---|

| 4.59% fixed | Higher of 5.25% or 6.59% | 6.59% |

| 5.39% fixed | Higher of 5.25% or 7.39% | 7.39% |

| 6.10% fixed | Higher of 5.25% or 8.10% | 8.10% |

This reduces how much you can borrow. If you were hoping to qualify for a $500,000 mortgage, the stress test might cut that to around $330,000–$350,000, depending on your income and debt ratios.

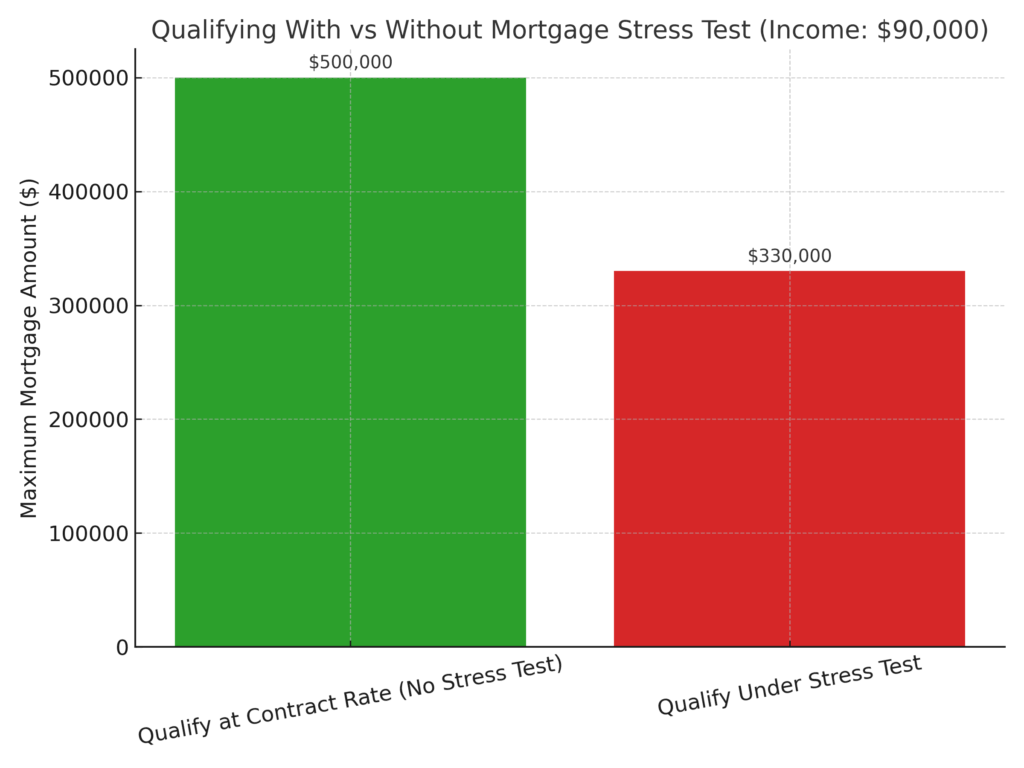

Qualifying Under the Stress Test vs. Qualifying Outside of It

When you qualify under the mortgage stress test, lenders don’t just look at the rate you are being offered. Instead, they use the higher benchmark rate (currently 5.25%, or your contract rate + 2%). This means your borrowing power is lower, but you are protected if rates rise in the future.

Example:

-

Offered rate: 4.89%

-

Stress test qualifying rate: 6.89%

-

Result: You qualify for about 15–20% less mortgage than expected.

On the other hand, qualifying outside of the stress test (which is sometimes the case with certain private lenders or credit unions) means lenders assess you based on the actual contract rate you’ll pay. This allows you to borrow more money up front, but it comes with added risk — if rates increase or your financial situation changes, you may struggle to keep up with payments.

Key takeaway: Qualifying under the stress test = safer but smaller mortgage. Qualifying outside of it = more borrowing power but higher risk.

Types of Lenders That Qualify Borrowers Using the Stress Test

Not every lender in Canada applies the mortgage stress test in the same way. The rules vary depending on the type of lender and the kind of mortgage you’re applying for:

-

Big Banks (A Lenders):

The “Big Six” banks and other federally regulated lenders must apply the stress test to every mortgage, whether insured or uninsured. If you’re working with a major bank, expect to qualify at 5.25% or your contract rate + 2%. -

Credit Unions:

Credit unions fall under provincial regulation, so they are not legally required to apply the stress test in all cases. However, many do so voluntarily to stay competitive and responsible. This makes them slightly more flexible than banks, but still fairly strict. -

Monoline Lenders (Non-Bank Lenders):

These are mortgage finance companies that don’t take deposits but specialize in mortgages. Since they are federally regulated, they must also apply the stress test. -

Private Lenders:

Private mortgage lenders, including individuals and mortgage investment corporations (MICs), are not bound by the stress test. Instead, they set their own criteria, usually focusing on property equity and loan-to-value (LTV) ratios rather than income. This can provide more borrowing power, but typically at higher interest rates.

Key Point: If you go to a bank, monoline lender, or most credit unions, you’ll need to pass the stress test. If you work with a private lender, you may avoid it—but you’ll face different trade-offs like higher costs.

What Homeowners Can Do

✅ Borrow within 4x your income – if you earn $90,000, aim for ~$360,000 mortgage.

✅ Pay down debt – reduces your total debt service ratio (TDS).

✅ Build savings – a larger down payment helps offset stress test limits.

✅ Consider alternatives – HELOCs, second mortgages, or private lending can provide flexibility. (See our post: A Second Mortgage or HELOC: Which is Right for You?)

FAQs: Mortgage Stress Test 2025

Q1: Do all lenders apply the stress test?

A: Banks and most traditional lenders must. Private lenders and some credit unions may not.

Q2: Can I avoid the stress test?

A: Only if you work with certain credit unions or private lenders, but you’ll likely pay higher rates.

Q3: How much less can I borrow in 2025?

A: On average, 15–20% less than before. For example, $500,000 in 2021 might only be $420,000 in 2025.

Q4: Does bad credit affect the stress test?

A: Yes. Even if you pass the stress test, a low score may limit lender options. See: Mortgage Renewal Options for Homeowners with Bad Credit.

Q5: What’s the future outlook?

A: Economists expect rate cuts in late 2025, which may ease affordability. But the stress test benchmark will remain until regulators adjust.

- Hard Money Lender Alberta: Guide for Homeowners in 2026 - February 26, 2026

- How Many Paystubs Are Required for a Mortgage in Canada? Helpful Guide - February 19, 2026

- Home Insurance Requirements for a Mortgage in Canada - February 13, 2026