Life happens. Sometimes unexpected expenses, job changes, or financial challenges leave you wondering if you can skip a mortgage payment. In Canada, some lenders allow this through special features, but skipping a payment comes with important consequences. Your balance grows, interest is capitalized, and renewal can become more complicated.

You may be able to skip a mortgage payment if your lender allows it, but interest still accrues, your outstanding balance increases, and your credit or renewal options may be impacted. Always understand the fine print and explore alternatives before making this decision.

Understanding Mortgage Payment Structures in Canada

To appreciate what happens when you skip a mortgage payment, it helps to understand how mortgage payments are structured.

Principal vs. Interest Breakdown

Every monthly payment covers two main parts:

-

Principal: This reduces your outstanding loan balance.

-

Interest: This is the cost of borrowing.

When you skip a mortgage payment, none of your principal is reduced, but the interest is still charged. That interest is often capitalized, meaning it gets added to your balance.

Why Skipping Affects Your Balance Differently

Mortgage amortization assumes regular payments. Skipping just one month can change your repayment schedule. That small pause can compound over the years, leaving you paying more interest in the long run.

Key takeaway: Skipping is not “free money.” It only delays repayment while increasing your balance.

Can You Skip a Mortgage Payment in Canada?

Maybe, but only in certain circumstances. Some banks, credit unions, and monoline lenders offer a “skip a payment” feature built into specific mortgage products.

-

Banks: The Big Five often advertise skip features as part of flexible mortgages.

-

Credit Unions: Regional lenders may allow this, but terms vary widely.

-

Monoline Lenders: These non-bank lenders sometimes offer flexible repayment structures that include skip options.

-

Private Lenders: Rarely allow skipping, as payments are more rigid.

Important to note: Skipping a mortgage payment is different from missing one. If you miss without approval, you risk arrears, late fees, and credit damage.

Mortgage Deferrals vs. Skip a Mortgage Payment: What’s the Difference?

Many Canadians confuse the government-backed mortgage deferrals offered during COVID-19 with contractual skip-a-payment options. While both provide short-term relief, they are not the same.

| Feature | Mortgage Deferral (Government-Backed) | Skip a Mortgage Payment (Contractual Option) |

|---|---|---|

| Origin | Introduced during COVID-19 as emergency relief | Part of certain mortgage contracts from banks, credit unions, and monoline lenders |

| Approval | Broadly available with government support | Must be pre-approved by your lender and included in your mortgage terms |

| Interest | Accrued during the deferral and added to the balance | Continues to be capitalized and added to the balance |

| Duration | Temporary, usually 3–6 months | Typically, once or twice per year, depending on your lender |

| Purpose | National financial relief program | Built-in flexibility for personal financial challenges |

| Availability | Applied across Canada during a crisis | Ongoing option only if your mortgage product allows |

Important to note: Mortgage deferrals were temporary, government-supported measures during extraordinary times.

For more insights, explore:

-

Mortgage Renewal Options for Homeowners with Bad Credit: renewal considerations after skipped or deferred payments.

-

Emergency Loans Canada: options if you need short-term relief beyond your mortgage.

-

How To Get Out of Power of Sale in Ontario: what can happen if skipped or missed payments spiral into legal action?

What Happens Financially When You Skip a Mortgage Payment

Skipping a payment doesn’t erase your obligation. Instead, it shifts it forward and grows your balance.

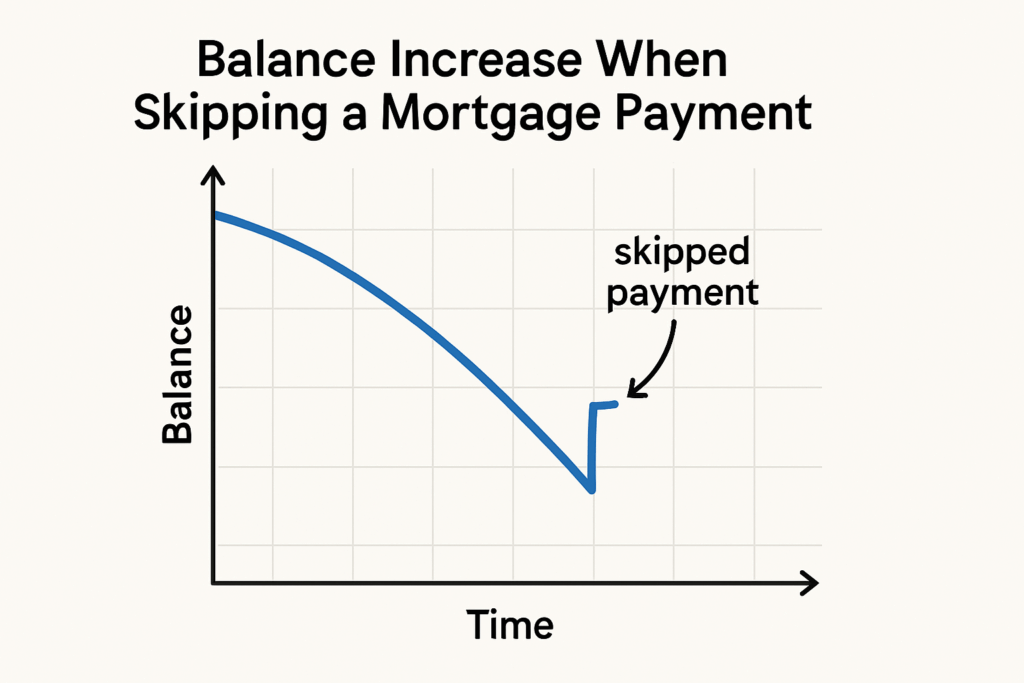

Interest Accumulation and Capitalization

When you skip a mortgage payment, the unpaid interest is capitalized onto your balance. Next month, you’re paying interest on a higher balance, creating a snowball effect.

How Your Balance Grows Over Time

Example:

-

$400,000 mortgage at 5% interest

-

Skipping one monthly payment adds $1,666 (est) in interest to your balance

-

That $1,666 (est) now accrues interest until the mortgage is renewed or paid down

Common mistake: Believing the lender “covers” your payment. In reality, you cover it later, with extra interest.

Credit Score and Legal Impacts

Skipping a mortgage payment with approval is different than defaulting.

-

Approved Skip: Usually does not harm your credit score.

-

Missed Payment: Lender reports to credit bureaus after 30 days, damaging your score.

-

Multiple Missed Payments: Risk of mortgage arrears, legal notices, and even power of sale or foreclosure.

Key takeaway: Always confirm with your lender before skipping. An unauthorized skip is treated as delinquency.

Common Myths About Skipping a Mortgage Payment

❌ Myth 1: It doesn’t affect interest.

Interest continues to grow, and your balance increases.

❌ Myth 2: Banks will always allow it.

Not true. Only specific mortgage products have skip features.

❌ Myth 3: It has no impact on renewal.

Skipped or missed payments can raise certain red flags when negotiating at renewal.

Important to note: Renewal time is when your lender reassesses risk. A history of skipped payments may push you toward higher-rate lenders.

Renewal and Refinancing Concerns

Your ability to renew or refinance can be impacted if you frequently skip a mortgage payment.

-

Banks: May decline renewal or avoid any interest rate negotiations.

-

Credit Unions: More flexible but still cautious about skipped payments.

-

Private Lenders: Will consider your request for renewal, but at slightly higher rates or decline to renew altogether.

Example

A homeowner with two skipped payments approaches renewal. The bank declines, citing affordability concerns. The borrower turns to a private lender, securing financing but at 2%+ higher interest.

Key takeaway: Even approved skips can affect your options later.

Alternatives to Skipping a Mortgage Payment

Before you skip, consider other ways to manage cash flow:

-

Refinancing: Extends amortization, lowering payments.

-

HELOC: Allows you to borrow against equity with flexible repayment.

-

Prepaid second mortgage: Lets you reduce or eliminate payments temporarily.

-

Budget adjustments: Cutting expenses or restructuring debts may solve the issue without touching your mortgage or equity in your home.

Common mistake: Assuming skipping is the only option. Often, alternatives can be safer and cheaper.

Rebounding After Skipping a Mortgage Payment

Emergencies happen, and sometimes skipping a mortgage payment is unavoidable. The good news is there are ways to get back on track and counteract the interest that was capitalized onto your principal balance. By planning ahead, you can soften the long-term impact and restore your financial footing.

-

Make a prepayment when you’re financially stable again – Even a small extra contribution can help offset the interest that was added to your balance.

-

Increase your regular payments when possible – If your budget allows, raising your monthly payment by even $50 can reduce your balance faster.

-

Use a lump sum at renewal – Renewal is a natural time to pay down the principal balance. A bonus, tax refund, or savings contribution can help reduce your balance significantly.

-

Consider an early renewal to a lower rate – If market conditions shift, locking into a lower rate can decrease your monthly obligation. Always consult a mortgage specialist to run the numbers and confirm if this strategy makes sense.

-

Generate extra income through a rental unit – If your property permits, adding a basement suite or secondary unit can ease affordability pressures while helping you catch up on your mortgage.

Key takeaway: Skipping a mortgage payment doesn’t have to create lasting damage. With proactive steps, you can regain control, shorten your amortization, and put yourself back on track financially.

Checklist: Steps to Take Before Skipping a Mortgage Payment

-

Contact your lender immediately.

-

Review your mortgage agreement for skip provisions.

-

Understand how principal and interest are affected.

-

Confirm how this will impact your renewal.

-

Explore refinancing, HELOCs, or prepaid second mortgages as alternatives.

Important to note: Lenders prefer proactive communication. Silence can harm your options later.

Skip a Mortgage Payment Comparison

| Option | Impact on Balance | Impact on Renewal | Availability |

|---|---|---|---|

| Skip a mortgage payment | Balance increases, interest capitalized | Renewal may be harder | Major banks, credit unions, and monoline lenders |

| HELOC | Flexible payments | Neutral if managed well | Depends on equity |

| Prepaid second mortgage | Payments reduced or removed for a set term | Renewal can be structured around it | Private lenders |

Important Fact:

A prepaid mortgage affords borrowers the ability to reduce or remove payments for a certain period of time during the mortgage term. Sometimes this can help avoid financial disasters and give a family the breathing room they need until things are financially sound again.

FAQ: Skipping a Mortgage Payment in Canada

Q1: Does skipping a mortgage payment hurt my credit in Canada?

A: If it’s part of an approved skip program, your credit is not affected. However, missing a payment without approval will damage your credit score.

Q2: How many times can I skip a mortgage payment?

A: It depends on your lender. Most allow once or twice a year, but private lenders rarely offer this.

Q3: What’s the difference between a deferral and skip a mortgage payment?

A: Deferrals (like during COVID-19) were temporary government-backed programs. Skips are contractual privileges built into your mortgage. Both capitalize interest.

Q4: What happens at mortgage renewal if I skipped payments?

A: Skipped payments may limit your renewal options with banks. You may need to turn to alternative lenders at higher rates.

Q5: Can I make partial payments instead of skipping?

A: Some lenders allow partial or interest-only payments, but you must arrange this in advance.

Final Thoughts: Skipping a Mortgage Payment in Canada

Skipping a mortgage payment can provide short-term relief, but it comes with long-term costs. Interest is capitalized, your balance increases, and your renewal may be affected. Always read your contract carefully and explore alternatives like refinancing, HELOCs, or prepaid second mortgages.

It’s equally important to create and stick to a budget that keeps your household on track. Be diligent during financially difficult times and take proactive steps to manage your obligations. Communicate openly with the parties that matter most: your mortgage lender, financial advisor, mortgage professional, and most importantly, your family. With the right support and planning, you can navigate financial challenges and keep your home secure.

Need Mortgage Advice Before Skipping a Payment?

Speak with one of our mortgage professionals today to understand how skipping a mortgage payment could affect your balance, interest, and renewal options.