How Credit Report Delinquencies Affect Your Mortgage Approval in Canada

Introduction

For many Canadians, owning a home is one of the most significant financial goals in their lifetime. But the road to homeownership is rarely a straight line — especially when your credit report carries the weight of past financial struggles. Whether it was a missed credit card payment during a difficult stretch, a medical emergency that derailed your finances, or a period of unemployment that left a few accounts unpaid, credit report delinquencies can feel like a permanent barrier standing between you and your dream home.

The good news? They are not always as final as they seem.

Understanding how delinquencies work, what lenders actually look for, and what options are available to you — especially in Canada’s layered lending landscape — can make all the difference between getting approved and continuing to rent. At LendToday.ca, we work every day with Canadians who have been turned away by their banks and credit unions, and we know firsthand that a delinquency on your credit report is not the end of the story.

This guide will walk you through everything you need to know about credit report delinquencies and obtaining a mortgage in Canada — including what counts as a delinquency, how long it lingers on your file, and what your real options are when the big banks say no.

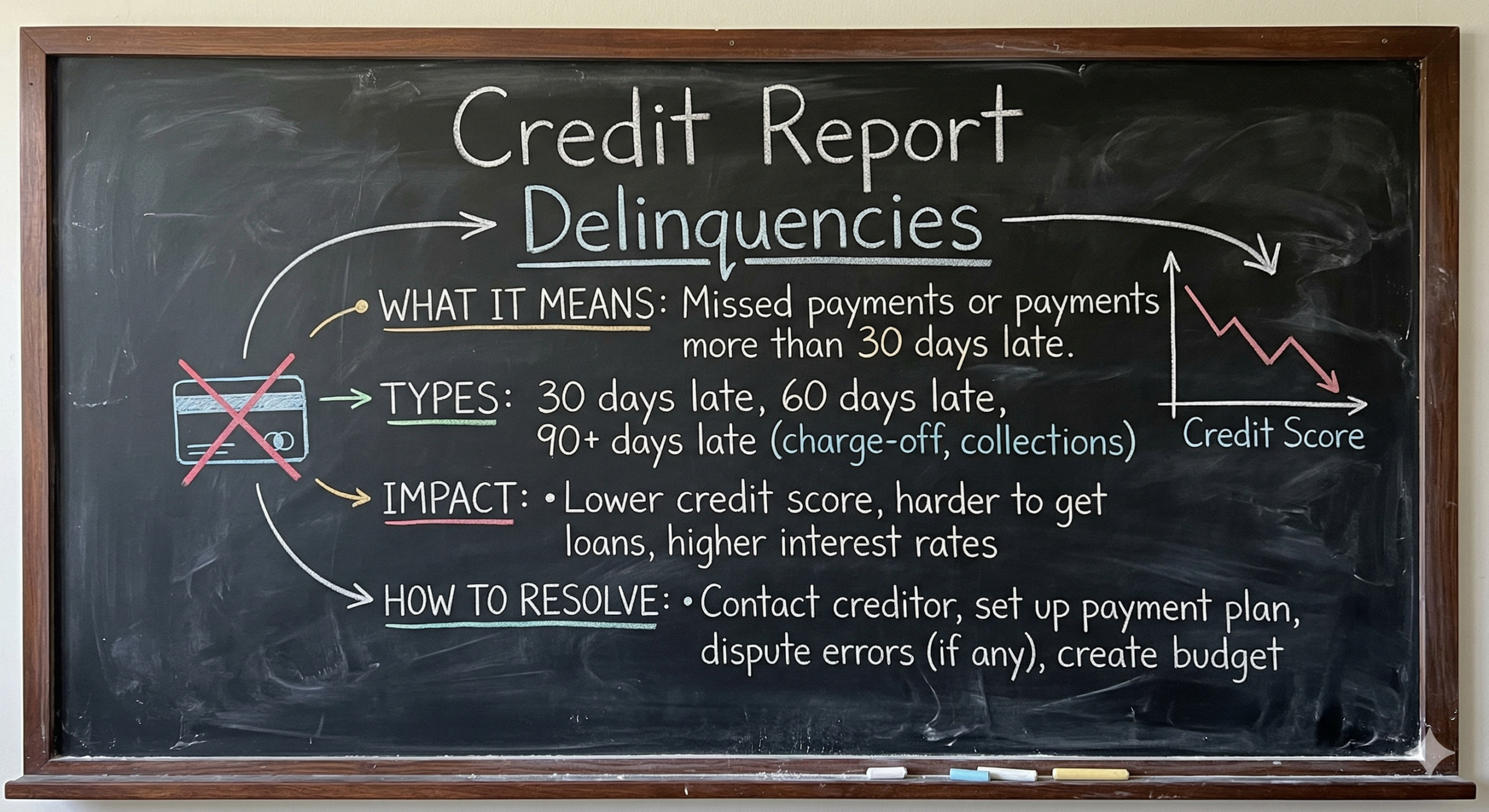

What Is a Credit Report Delinquency?

A credit report delinquency occurs when you miss a payment on a credit obligation — whether that is a credit card, car loan, personal line of credit, utility account, or any other debt — and that missed payment is reported to one or both of Canada’s major credit bureaus: Equifax and TransUnion.

Delinquencies are typically recorded in stages:

- 30 days past due — A soft warning. One late payment at this stage may cause a minor dip in your credit score but is generally not catastrophic on its own.

- 60 days past due — Lenders begin to take notice. Multiple accounts at this stage signal cash flow problems to underwriters.

- 90 days or more past due — This is considered a serious delinquency. At this stage, lenders may send the account to collections or write it off entirely.

- Collections or charge-offs — The most damaging entries. Once an account has been sent to a third-party collection agency or written off by the original lender, it leaves a significant mark on your credit file.

It is important to note that even a single serious delinquency — especially one involving a previous mortgage — can dramatically affect your ability to secure new financing through a traditional lender.

How Delinquencies Affect Your Credit Score

In Canada, your credit score is calculated on a scale from 300 to 900. Most major chartered banks (referred to as “A lenders”) require a minimum score of 680 to 720 for standard mortgage products. Even a single missed payment reported to the credit bureaus can drop your score by 50 to 100 points or more, depending on your overall credit profile and how recently the event occurred.

Here is a general breakdown of how delinquency-related entries affect your credit score:

Payment history accounts for the largest share of your credit score — roughly 35% in most scoring models used in Canada. This means that the moment a lender reports a missed payment, your score takes an immediate hit. The severity of that hit depends on:

- Recency — A missed payment from six months ago hurts more than one from five years ago.

- Frequency — Multiple late payments across different accounts compound the damage.

- Severity — A 90-day delinquency or a charge-off is far more damaging than a single 30-day late mark.

- Amount owed — Larger delinquent balances send a stronger negative signal to lenders.

Collections entries, judgments, and consumer proposals all carry their own unique weight and remain visible to mortgage underwriters even when they no longer actively factor into your numerical credit score.

How Long Do Delinquencies Stay on Your Credit Report in Canada?

This is one of the most common questions we hear from clients. Under Canadian credit reporting rules, most negative entries remain on your file for a set period of time, depending on your province and the type of entry. Here is a general overview:

- Late payments (30–90 days): Remain on file for approximately 6 years from the date of the last activity.

- Collections accounts: Remain on file for approximately 6 years from the date of last activity (in most provinces).

- Judgments: Typically remain for 6 years or until the judgment is satisfied, whichever is longer.

- Consumer proposals: Remain for 3 years after the proposal is completed, or 6 years from the date it was filed, whichever comes first.

- Bankruptcy: A first bankruptcy remains on file for 6 years after discharge in most provinces. A second bankruptcy stays for 14 years.

The key takeaway here is that time does not immediately erase these entries — but it does reduce their impact. As delinquencies age, lenders place progressively less weight on them, particularly if your credit behaviour has improved significantly in the years since.

What Mortgage Lenders Actually Look for When They See Delinquencies

Not all lenders treat delinquencies the same way. In Canada, the lending landscape is structured in tiers, and your options depend heavily on where you fall within that structure.

A Lenders (Major Banks and Credit Unions)

Canada’s major chartered banks — RBC, TD, CIBC, BMO, Scotiabank — and most credit unions operate under strict federal lending guidelines. They use automated underwriting systems that are sensitive to credit blemishes and typically require:

- A minimum credit score of 680 or higher

- No collections or delinquencies within the past two to three years

- A clean mortgage payment history if you have had a previous mortgage

- A total debt service (TDS) ratio generally below 44%

If your credit report shows recent delinquencies, an A lender will almost always decline your application — regardless of your income or equity position.

B Lenders (Alternative Institutional Lenders)

B lenders, which include trust companies and alternative mortgage lenders such as Home Trust, Equitable Bank, and others, operate with more flexibility. They are still regulated but are willing to look at borrowers who do not fit the perfect A lender profile.

B lenders typically accept:

- Credit scores as low as 550 to 600

- Some history of missed payments, provided recent payment behaviour has improved

- Higher debt ratios in some cases

- Larger down payments (typically 20% or more) to offset higher risk

The trade-off is that B lender mortgage rates are higher than A lender rates — often by 1% to 2% or more. However, for many Canadians recovering from past credit challenges, a B lender mortgage can be the first step back toward mainstream financing.

Private Mortgage Lenders

Private mortgage lenders are individuals or companies that lend their own capital. They are primarily asset-based lenders, meaning they focus on the value of the property and your available equity rather than your credit score or employment history.

Private lenders are often the most accessible option for Canadians with serious delinquencies, recent bankruptcies, or consumer proposals on their credit reports. They typically offer:

- Short-term mortgages (6 months to 2 years)

- Approval based primarily on property value and loan-to-value ratio

- Faster funding timelines

- Higher interest rates to reflect the increased risk

While private lending is not a long-term solution for most borrowers, it can be an important bridge — giving you time to stabilize your finances, repair your credit, and work toward qualifying with a B or A lender at renewal.

Can You Get a Mortgage in Canada with Delinquencies on Your Credit Report?

The short answer is: yes, in many cases you can — but the pathway depends on the type and severity of the delinquency, how recent it is, the property you are financing, and how much equity or down payment you have available.

Here are some common scenarios and what they typically mean for your mortgage options:

Scenario 1: One or two late payments from two or more years ago This is generally manageable. If you have otherwise maintained good credit since the late payments occurred and your score is above 620, many B lenders and some credit unions will still work with you. An experienced mortgage broker can often find a solution without needing to go the private lending route.

Scenario 2: A collections account that has been settled A settled collections account is viewed more favourably than an outstanding one. If the collection is older than two years and your recent credit behaviour has been clean, a B lender approval is often achievable — particularly with a 20% or larger down payment.

Scenario 3: Multiple recent delinquencies or active collections This is more challenging from an institutional perspective, but private mortgage lenders remain an option — particularly if you own a property with significant equity. Private financing allows you to buy time to address the delinquencies, settle outstanding collections, and begin rebuilding your credit profile.

Scenario 4: A previous mortgage delinquency This is one of the most serious scenarios in the eyes of lenders. A mortgage delinquency — especially one that resulted in power of sale or foreclosure — raises immediate flags for any underwriter. This typically requires private lending initially, with a clear plan toward B lending at renewal.

Steps You Can Take to Improve Your Chances of Mortgage Approval

If you have delinquencies on your credit report, there are concrete steps you can take right now to strengthen your position — whether you are planning to apply for a mortgage in three months or three years.

1. Pull your own credit report and review it carefully. Errors and outdated entries on credit reports are more common than most people realize. Under Canadian law, you are entitled to a free copy of your credit report from both Equifax and TransUnion. Review every entry for accuracy. If you find an error — a payment reported as missed when it was made on time, or an account that belongs to someone else — dispute it directly with the bureau. Removing an erroneous entry can produce an immediate score improvement.

2. Settle outstanding collections — but do it strategically. Paying off a collections account can be beneficial, but timing matters. If a collection is very close to falling off your report due to age, paying it now may reset the reporting timeline in some cases. Consult with a mortgage broker before making payments on old delinquencies to ensure you are taking the most effective approach.

3. Bring your current accounts current and keep them that way. Payment history is the single biggest factor in your credit score. Even if your past is messy, a consistent record of on-time payments going forward begins to shift the narrative. Lenders want to see that the period of financial difficulty is behind you, not continuing.

4. Reduce your credit utilization. Credit utilization — the percentage of your available credit that you are using — is the second most important factor in your credit score. Paying down revolving credit card balances below 35% of your limit (and ideally below 10%) can produce meaningful score improvements relatively quickly.

5. Avoid applying for new credit unnecessarily. Every hard credit inquiry from a new application temporarily reduces your score. If you know you will be applying for a mortgage in the near future, hold off on new credit cards, car loans, or other applications in the months leading up to your mortgage application.

6. Work with a mortgage broker who specializes in challenging credit situations. This is perhaps the most important step of all. The right mortgage broker does not simply submit your application to the first lender on their list. They assess your complete financial picture, identify the lenders most likely to approve you at the best available rate, and structure your application to present your story in the strongest possible light.

How Equity Can Work in Your Favour

One of the most powerful tools available to Canadian homeowners and buyers with credit challenges is equity. Equity — whether built up in an existing property or provided through a significant down payment — dramatically reduces the lender’s risk exposure, which in turn opens doors that would otherwise remain closed.

For homeowners looking to refinance despite having delinquencies on their credit report, a strong equity position (typically 25% or more) often makes the difference between a denial and an approval. Private and B lenders place significant weight on loan-to-value ratios, and lower LTVs can offset even serious credit blemishes.

For first-time buyers, a larger down payment — beyond the minimum 5% required under CMHC’s insured mortgage program — signals financial discipline and reduces lender risk. Buyers who can put down 20% or more have access to conventional (uninsured) mortgages, which opens up both B and private lending options that are not available on insured files.

The Role of a Mortgage Broker in Navigating Delinquencies

Navigating Canada’s mortgage market with credit challenges is not something you should have to do alone — or without expert guidance. When a bank’s automated approval system declines your application, it does not mean no lender in the country will finance your purchase or refinancing. It means that particular lender, with those particular guidelines, at that particular moment, could not accommodate your file.

A mortgage broker with experience in alternative and private lending understands the full spectrum of options available — and more importantly, they understand how to position your application to give it the best possible chance of success. They have relationships with dozens of lenders, including A lenders, B lenders, and private lending sources, and they can assess in advance which path makes the most sense for your specific situation.

At LendToday.ca, our team works with clients across Canada who are dealing with credit challenges of all kinds — from a single missed payment years ago to more complex situations involving collections, consumer proposals, and everything in between. We do not just submit applications; we work alongside our clients to build a roadmap toward the financing they need, and the financial future they deserve.

Frequently Asked Questions

Can I get a mortgage with a 500 credit score in Canada? A score in the 500 range effectively closes the door on A and most B lenders. However, private mortgage lenders focus primarily on equity and property value rather than credit score, making approval possible for borrowers with sufficient equity or a substantial down payment.

Does a consumer proposal disqualify me from getting a mortgage? Not permanently. During an active consumer proposal, A lender approval is generally not possible. However, B lenders and private lenders will often work with borrowers who are in or have completed a consumer proposal, depending on the overall file strength. After a proposal is completed and has been discharged from your credit report, A lender options typically reopen.

How long after a bankruptcy can I get a mortgage in Canada? Most A lenders require two years after a discharge before they will consider your application, combined with a minimum credit score rebuild to at least 680. B lenders may work with you sooner — sometimes within one to two years of discharge — depending on the file. Private lenders may work with you even during bankruptcy in cases involving significant property equity.

Will paying off collections immediately fix my credit score? Not necessarily immediately, and not always as dramatically as you might expect. The entry remains on your report even after it is settled, though the status changes from “unpaid” to “paid.” Over time, this improvement in status — combined with continued positive payment behaviour — contributes to a gradual score recovery.

Conclusion: A Delinquency Is Not a Destination

A credit report delinquency is a record of a difficult moment in your financial life — but it does not have to define your financial future. Canada’s mortgage market offers far more options than most people realize, and with the right guidance, many Canadians who have been turned away by their bank find a path to the financing they need.

The key is understanding where you stand, knowing what options are available at each stage of your credit recovery journey, and working with professionals who take the time to understand your situation rather than simply running it through a system.

If you have delinquencies on your credit report and you are ready to explore what your mortgage options might look like today, reach out to the team at LendToday.ca. We have helped thousands of Canadians navigate complex credit situations — and we are here to help you too.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Mortgage approvals are subject to lender guidelines and individual circumstances. Please speak with a qualified mortgage professional before making any financial decisions.