What Is a Second Mortgage?

A second mortgage is an additional loan secured against the value of your home, on top of your existing (first) mortgage. It gives you access to the equity you’ve built up without having to refinance your original mortgage.

When you borrow money using a second mortgage, the lender registers a second charge on your property. This means the first lender gets priority if you default, and the second lender only gets repaid after the first lender is made whole.

Equity Stack: How The Second Mortgage Works

Understanding how does a second mortgage work? is crucial for homeowners looking to leverage their equity. Let’s take a look at the numbers to better understand how the equity in your home is utilized when you obtain a second mortgage.

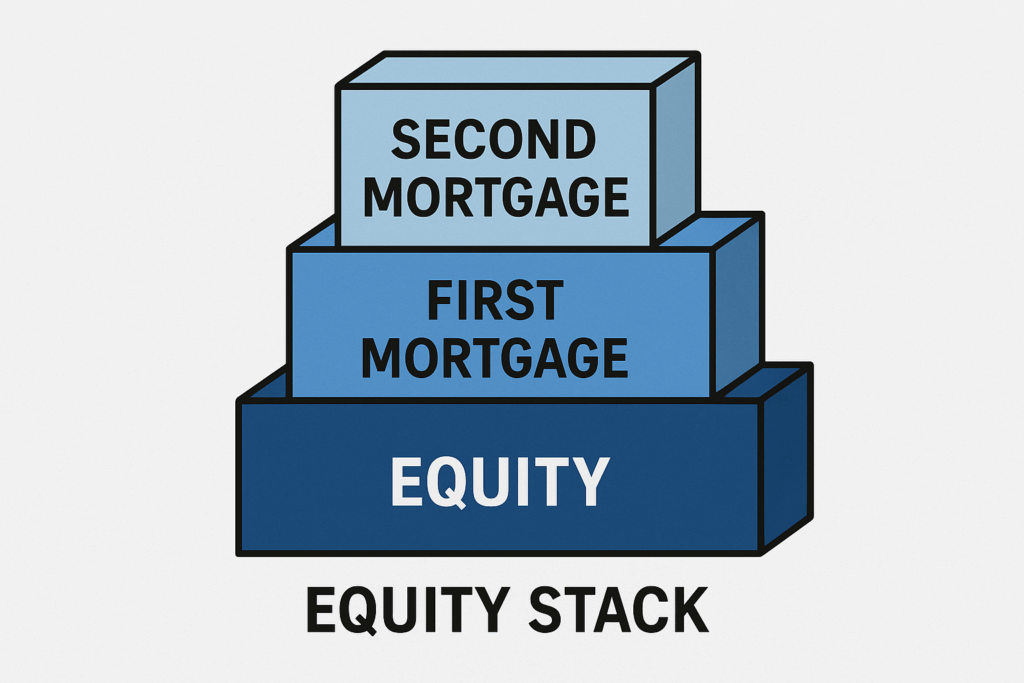

How a Second Mortgage Works: The Equity Stack

Think of your home equity as a stack. Your first mortgage takes the bottom layer, and the second mortgage sits on top. Here’s how it works inside the numbers:

| Current Market Value | $500,000 |

| Maximum Lending (80% LTV) | $400,000 |

| 1st Mortgage Balance | $300,000 |

| Available for 2nd Mortgage | $100,000 |

- Your home value sets the ceiling for borrowing.

- Most lenders cap total mortgages around 80% LTV.

- The first mortgage gets priority if the home is sold or foreclosed.

- The second mortgage uses the “room” left in your equity.

This “equity stack” shows how second mortgages sit behind the first mortgage but allow you to unlock extra funds.

Why Do Homeowners Take Out a Second Mortgage?

Canadian homeowners use second mortgages for many reasons, including:

| Common Uses of a Second Mortgage | Example |

|---|---|

| Debt consolidation | Replacing $50,000 of high-interest credit card debt with one lower-rate payment. |

| Home renovations | Funding a $40,000 kitchen or basement upgrade. |

| Business investment | Using $75,000 in equity to launch or expand a small business. |

| Paying off arrears | Settling overdue property taxes, mortgage arrears or CRA debts. |

| Emergency expenses | Covering unexpected medical or family costs. |

How Payments Work on a Second Mortgage

Unlike your first mortgage, which usually blends principal and interest, most second mortgages are interest-only payments during the term.

| Payment Feature | First Mortgage | Second Mortgage |

|---|---|---|

| Term | 1–5 years (or longer) | 1–2 years (short-term) |

| Payments | Principal + Interest | Interest-only (monthly) |

| Renewal | Common, at maturity | Often refinanced or repaid at term end |

| Risk | Lower (first charge) | Higher (second charge) |

👉 At the end of your second mortgage term, you must either:

-

Pay off the balance in full,

-

Refinance into a new mortgage, or

-

Extend the second mortgage with your lender.

It’s important to think about your exit strategy from day one. Whether your plan is to pay off the balance, refinance, or extend, knowing your path ahead of time helps you stay on track. Since circumstances can change, checking in with your mortgage professional regularly ensures you understand how things are trending and what adjustments may be needed along the way.

Why Are Interest Rates Higher?

Second mortgages carry higher interest rates because the lender is in a riskier position. If you default, the first mortgage lender is repaid first, and the second lender may recover less—or nothing.

Still, second mortgage rates are usually lower than unsecured loans or credit cards, making them attractive for debt consolidation.

Can You Get a Second Mortgage With Poor Credit?

Yes. One of the key benefits of a second mortgage is that lenders often care more about your equity than your credit score.

-

With bad credit, lenders may still approve you if your loan-to-value (LTV) is 80% or less.

-

Private lenders in particular are more flexible than banks.

-

Mortgage brokers can match you with lenders open to borrowers with bruised credit or even past bankruptcies.

Pros and Cons of Second Mortgages

| Pros | Cons |

|---|---|

| Access to equity without breaking your first mortgage | Higher interest rates than first mortgages |

| Interest-only payments improve cash flow | Risk of foreclosure if payments are missed |

| Flexible approval (equity matters more than credit) | Short terms (often 1–2 years) require refinancing |

| Useful for debt consolidation or past due expenses | Closing costs (legal, appraisal, lender and broker fees) |

How Does a Second Mortgage Work? Considerations

A second mortgage is most useful when you have sufficient equity and a clear plan. Here’s how does a second mortgage work for different situations:

1) Homeowners consolidating high-interest debt

If you’re juggling multiple credit cards or personal loans at double-digit rates, a second mortgage can roll them into one payment—often at a lower rate than unsecured debt. How does a second mortgage work here? You borrow against equity, pay off balances in full, and replace scattered bills with one predictable payment.

2) Borrowers who can’t or don’t want to refinance the first mortgage

If your first mortgage has a great fixed rate (or large prepayment penalties), refinancing might be costly. How does a second mortgage work instead? It leaves your first mortgage untouched and adds a second, smaller loan on top—keeping your cheap rate intact.

3) Self-employed or non-traditional income earners

Banks can be strict about income verification. With a second mortgage, lenders often prioritize equity and property over rigid income metrics. How does a second mortgage work in this case? You leverage equity while your broker finds a lender comfortable with bank statements, NOAs, or stated income.

4) Homeowners tackling time-sensitive expenses

From property-tax arrears to urgent repairs, you may need funds fast. How does a second mortgage work under time pressure? Private lenders can move quickly (days, not weeks), and interest-only payments can ease cash flow while you stabilize.

5) Renovators and value-add investors

Planning a basement suite or kitchen upgrade? How does a second mortgage work for renovations? You unlock a chunk of equity now, invest into improvements that may boost value, then refinance or renew once the project is complete.

6) Borrowers rebuilding credit

If you’re recovering from missed payments, proposals, or prior bankruptcy, banks may say no. How does a second mortgage work during a rebuild? It acts as a bridge—access to funds while you repair credit, with a plan to return to A-lender financing later.

7) Business owners needing growth capital

Instead of high-cost merchant cash advances, consider your home equity. How does a second mortgage work for entrepreneurs? You draw against equity at (typically) lower cost, invest in inventory or marketing, and set a defined payoff strategy.

Final Thoughts: How Does A Second Mortgage Work in Real Life?

How does a second mortgage work when you put it all together? It’s a short-term, equity-backed loan that sits behind your first mortgage, commonly with interest-only payments and a 1–2 year term. The big wins are speed, flexibility, and cash-flow relief—especially for debt consolidation, renovations, or urgent expenses. The trade-offs are higher rates than a first mortgage, short terms, and the need for a clear exit plan.

If you’re weighing options, talk to a mortgage professional who understands how does a second mortgage work with your specific equity, LTV, property type, and credit profile. We’ll map your numbers, compare lender options, and show you how to get from “short-term solution” back to traditional A-lender financing when the time is right.

Frequently Asked Questions: How Does a Second Mortgage Work?

Q1: How does a second mortgage work in Canada?

A second mortgage works by letting you borrow against the equity in your home without changing your first mortgage. The first mortgage remains in priority, while the second mortgage is registered as a second charge on your property. Most second mortgages are short-term, interest-only, and require a clear repayment or refinance plan at the end of the term. To see real examples of how this applies, visit our guide on Second Mortgage in Alberta.

Q2: What is the difference between a first mortgage and a second mortgage?

The first mortgage is your primary home loan and has priority if the property is sold or foreclosed. A second mortgage is an additional loan secured against your home equity but ranks behind the first mortgage. Because the second lender takes on more risk, the interest rates are usually higher. Learn more about second mortgage options in our article on Second Mortgage with Bad Credit.

Q3: Can I get a second mortgage with bad credit?

Yes, many Canadian homeowners qualify for a second mortgage even with bruised or bad credit. Lenders typically focus on your home equity and loan-to-value (LTV) ratio rather than just your credit score. Private lenders are especially flexible, although interest rates may be higher. For strategies that work if your credit isn’t perfect, explore our full article on Second Mortgage with Bad Credit.

Q4: What can I use a second mortgage for?

Homeowners use second mortgages for debt consolidation, home renovations, paying off property tax or CRA arrears, business investments, or covering major expenses. Since funds are secured against your property, the rates are often lower than unsecured personal loans or credit cards. If you’re thinking of consolidating debt, you may also want to review our dedicated guide on Mortgage Broker For Bad Credit Home Loans in Ontario.

Q5: What happens at the end of a second mortgage term?

At the end of the term, you must either pay off the balance in full, refinance into a new mortgage, or extend the second mortgage with your lender. It’s important to plan your exit strategy from day one and keep in regular contact with your mortgage professional. For homeowners facing renewal challenges, check out our article on Mortgage Renewal Options for Homeowners with Bad Credit.

Key Takeaway

How Does A Second Mortgage Work? It unlocks home equity without breaking your first mortgage—ideal for debt consolidation, renovations, or urgent needs. It’s short-term, usually interest-only, and requires a clear exit plan.

Start My Application