Table of Contents

ToggleCan I Port My Mortgage? The 2026 Guide to Moving Without Breaking the Bank

You’ve found it—the perfect next house. It has the extra bedroom you need, the backyard the kids want, and it’s in that quiet Bowmanville pocket you’ve been eyeing. But then you look at your current mortgage statement. You have three years left on a fixed rate of 2.74%.

You glance at today’s 2026 market rates and see numbers significantly higher. Your heart sinks. “If I sell my house, do I lose this rate? Do I have to pay a $15,000 penalty to the bank just to move?”

The answer likely lies in a powerful but often misunderstood feature: Mortgage Porting.

At Lendtoday.ca, we specialize in helping Ontario homeowners “pack up” their low rates and take them to their next destination. Here is the definitive 2026 guide to porting your mortgage.

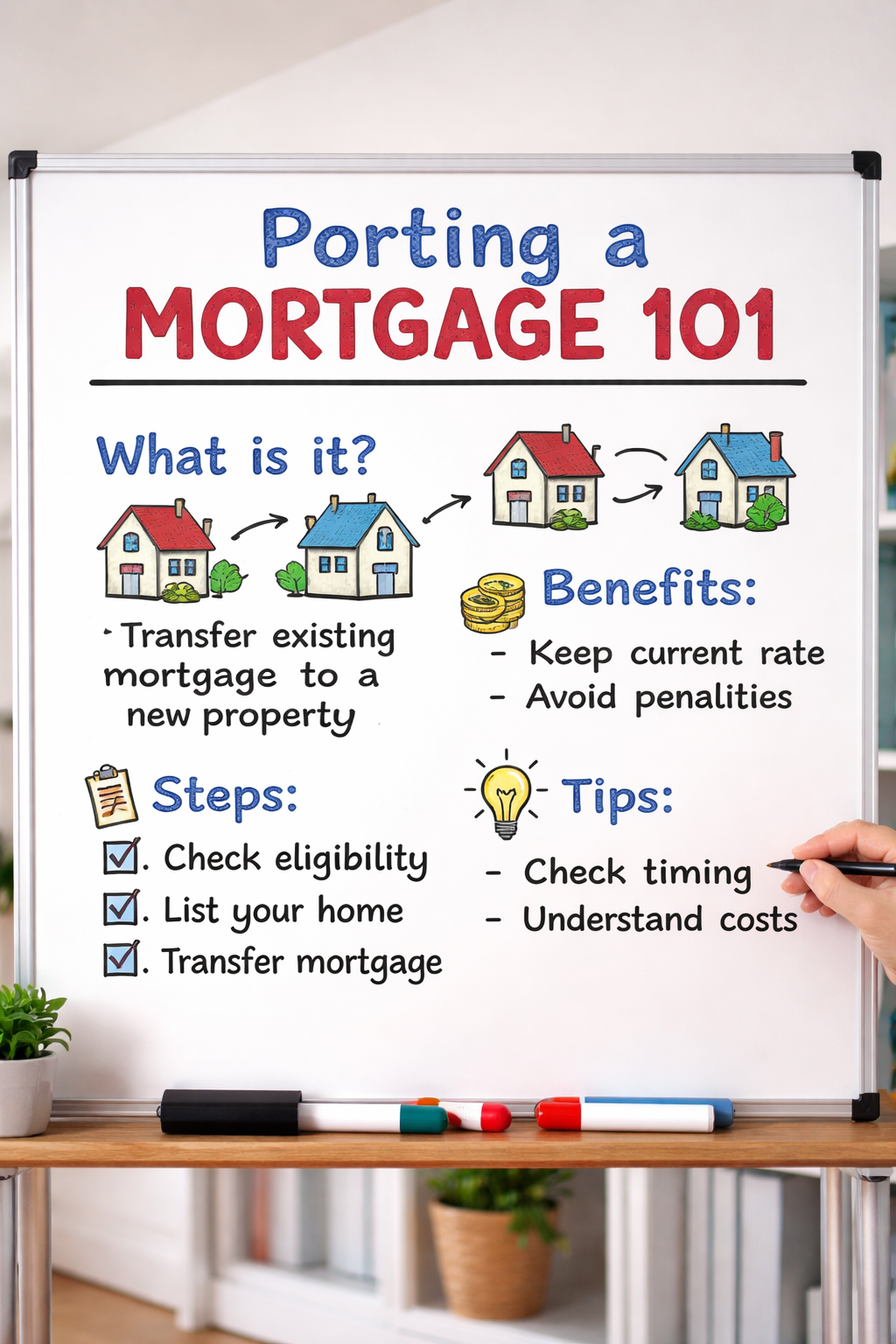

1. What is Mortgage Porting? (The Simple Definition)

Mortgage porting is the process of transferring your existing mortgage—including its current interest rate, remaining term, and terms and conditions—from your current property to a new one.

Think of it like a “financial carry-on.” Instead of “breaking” your mortgage, paying a massive prepayment penalty, and starting a brand-new loan at today’s higher rates, you simply move the existing contract to the new address.

2. The Three Types of Ports in the 2026 Market

Not every move is a “one-to-one” swap. Depending on whether you are upsizing or downsizing, your port will fall into one of these three categories:

A. The Straight Port

You are moving from one home to another, and the mortgage amount stays exactly the same.

-

The Result: No change to your rate. No change to your payment (other than potential property tax adjustments). This is the cleanest way to move.

B. Port and Increase (The “Blend and Extend”)

You are buying a more expensive home and need more money.

-

How it works: You keep your old $400,000 at 2.74%. You borrow an additional $200,000 at today’s market rate (e.g., 5.25%).

-

The Result: The lender “blends” the two rates together. You end up with a Weighted Average Rate (likely around 3.58% in this example). This is almost always cheaper than a full refinance.

C. Port and Decrease

You are downsizing to a cheaper home and need a smaller mortgage.

-

The Catch: While you can keep your low rate, you will likely have to pay a pro-rated prepayment penalty on the amount of the mortgage you are “giving back” to the bank.

3. The “Gotchas”: Why Porting Isn’t Always Automatic

Even if your contract says your mortgage is “portable,” there are three major 2026 hurdles you must clear:

I. You Must Re-Qualify (The Stress Test)

This is the biggest shock for homeowners. Even though you already have the mortgage, porting is treated as a new application. You must provide new pay stubs, T4s, and pass the 2026 Stress Test. If your income has changed or you’ve taken on a large car loan, the bank could actually say “No” to the port

II. The Porting Window (30 to 120 Days)

Lenders have a strict timeline. You usually must close on your new home within 30, 60, or 90 days of selling your old one. If your closing dates are further apart, the port “expires,” and you’re back to square one.

-

Lendtoday Tip: If your dates don’t align, we can often use Bridge Financing to bridge the gap and save your port.

III. Same Lender, Same Province

You cannot port a mortgage from RBC to TD. You must stay with your current lender. Furthermore, some lenders only operate in Ontario; if you are moving to Alberta or the Maritimes, your mortgage might not be able to follow you.

4. Is Porting Better Than Refinancing? (The 2026 Math)

To know if you should port, you have to do a “Break-Even” analysis.

| Feature | Porting | Refinancing |

| Prepayment Penalty | $0 (usually) | Can be $10k – $30k+ |

| Interest Rate | Your current “Legacy” rate | Today’s Market Rate |

| Lender Choice | Must stay with current bank | Can shop for the best deal |

| Approval | Must re-qualify | Must re-qualify |

The 2026 Rule of Thumb: If your current rate is more than 1% lower than market rates, porting is almost always the winner. The savings on interest and the avoided penalty are simply too large to ignore.

FAQ: Your Porting Questions Answered

Can I port my variable-rate mortgage?

It depends. Many “standard” variable mortgages are portable, but some “Basic” or “No-Frills” variable products are restricted. Some lenders require you to convert to a fixed rate before they allow the port.

What happens to my CMHC insurance when I port?

Great news: CMHC insurance is portable! If you bought your home with less than 20% down, you can move that insurance to the new home. If the new home is more expensive, you only pay a “top-up” premium on the increased amount, rather than paying for a whole new policy.

Can I port my mortgage if I have a second mortgage or a HELOC?

This is complex. Usually, a second mortgage must be paid off before a port can happen, as the primary lender needs to move to the new property in “first position.” If you have a HELOC (Home Equity Line of Credit), it is usually closed and re-opened at the new address.

Final Thoughts: Don’t Leave Your Rate Behind

Your low interest rate is one of your most valuable assets. Don’t let a bank representative tell you that “breaking and starting fresh” is your only option.

At Lendtoday.ca, we look at your porting options first. We run the numbers, talk to your lender, and ensure that if there is a way to keep your low rate, we find it. Moving is stressful enough—your mortgage shouldn’t make it harder.