Every mortgage in Canada falls into one of three categories: insured, uninsured, or insurable. Your category is determined by your down payment, purchase price, and the property itself. It affects your mortgage rate, your lender options, and how much you pay over the life of your loan. Understanding the difference before you apply can save you thousands of dollars.

Table of Contents

ToggleWhy Mortgage Categories Matter in Canada

Most Canadian homebuyers focus on their mortgage rate without realizing that the category of mortgage they qualify for is what largely determines that rate in the first place.

Canadian mortgage lenders price their products based on risk. When a mortgage is backed by default insurance, the lender carries almost no risk of loss. That lower risk translates into better rates for borrowers. When a mortgage is not insured, lenders take on more exposure, and they price accordingly.

The three categories are insured mortgage, uninsured mortgage, and insurable mortgage. Each one has a specific definition under Canadian mortgage rules, and each one produces a different outcome for the borrower. Knowing which category you fall into, especially the mortgage insurance category, and why, is one of the most important things you can do before you start shopping for a home.

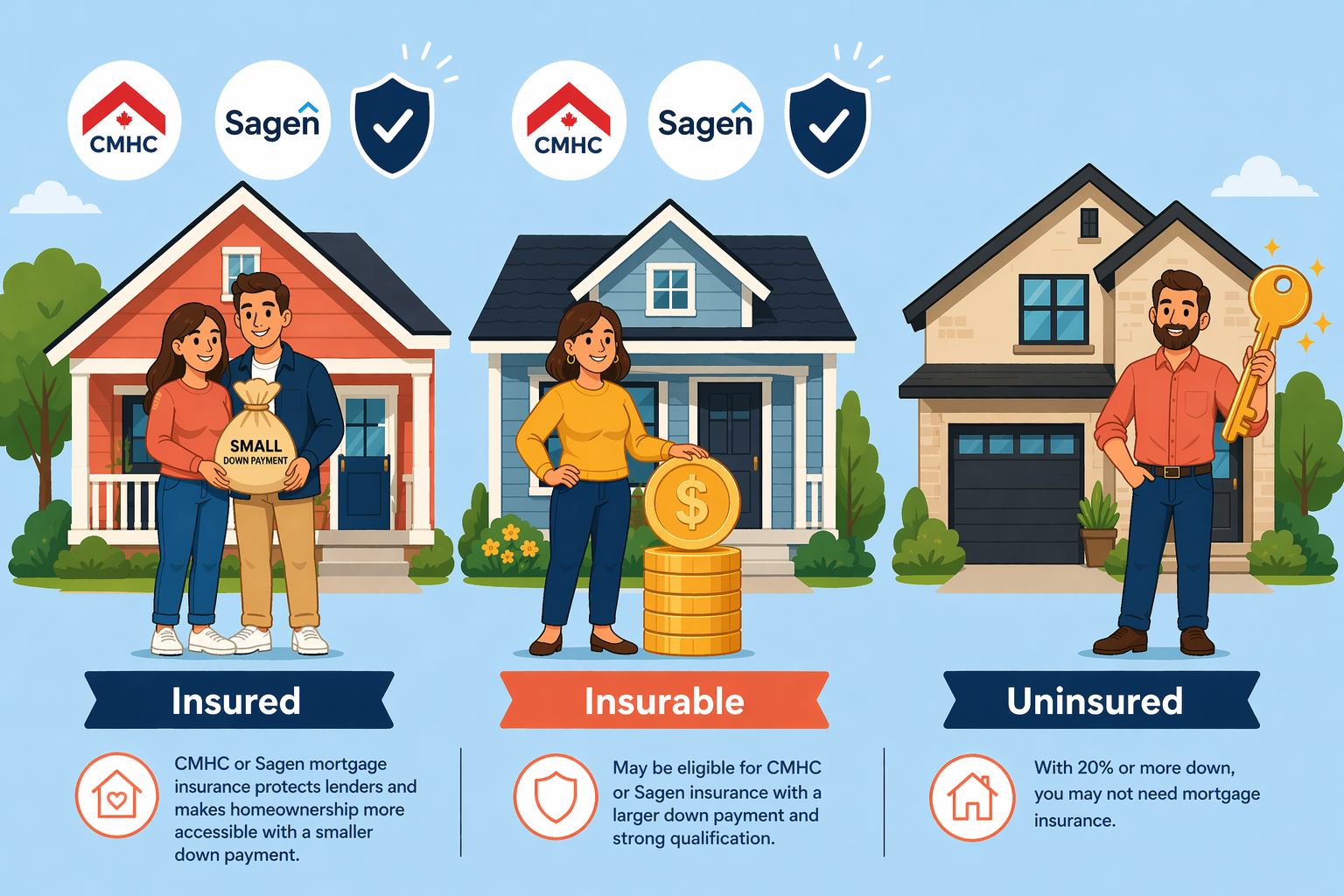

What Is an Insured Mortgage?

An insured mortgage is critical for many homebuyers as it allows access to better interest rates and more favourable terms. When you apply for default insurance, you are taking a smart step towards financial stability.

A default insured mortgage is a mortgage that is backed by mortgage default insurance. In Canada, this insurance is provided by one of three approved insurers: CMHC (Canada Mortgage and Housing Corporation), Sagen, or Canada Guaranty.

An insured mortgage is required any time a borrower puts down less than 20% of the purchase price. This is sometimes called a high-ratio mortgage, because the loan amount is high relative to the value of the property.

The insurance does not protect the borrower. It protects the mortgage lender. If the borrower defaults, the insurer pays out the lender’s loss. Because that protection is in place, lenders can confidently offer lower interest rates on insured mortgages.

As a borrower, understanding the nuances of an insured mortgage can lead to significant savings. An insured mortgage not only provides peace of mind but also helps you secure a competitive loan.

Important to note: insured mortgages are only available on owner-occupied properties with a purchase price under $1.5 million (as of 2024 rule changes). You cannot get an insured mortgage on a rental property, a commercial property, or a second home.

For first-time buyers, choosing mortgage insurance can often unlock the door to homeownership. With an insured mortgage, you are empowered to make informed decisions.

Who Qualifies for an Insured Mortgage?

To qualify for mortgage insurance, you must meet the following conditions:

- Your down payment is between 5% and 19.99% of the purchase price

- The purchase price is under $1.5 million

- The property will be your primary residence

- You pass the federal mortgage stress test at the qualifying rate

- Your maximum amortization period is 25 years (30 years for first-time buyers purchasing new builds under current federal rules)

Key takeaway: the lower your down payment, the larger your insurance premium. The premium is calculated as a percentage of the loan amount and is typically added to your mortgage balance rather than paid up front.

An insured mortgage can also provide the borrower with the ability to negotiate better terms and conditions. Being aware of your options for mortgage insurance can make a significant difference in your financial journey.

The Cost of Mortgage Default Insurance

The mortgage default insurance premium is tiered based on your loan-to-value ratio. As of the most recent CMHC schedule:

| Down Payment | LTV Ratio | Insurance Premium |

|---|---|---|

| 5% | 95% | 4.00% of loan amount |

| 10% | 90% | 3.10% of loan amount |

| 15% | 85% | 2.80% of loan amount |

| 20%+ | 80% or less | No premium required |

On a $600,000 home with a 5% down payment of $30,000, your insured mortgage would be $570,000. The 4% insurance premium would add $22,800 to your mortgage balance, bringing your total loan to $592,800. That premium is subject to provincial sales tax in some provinces, including Ontario.

Many homeowners find that an insured mortgage not only offers security but also enhances their chances of approval when applying for additional loans in the future. This is one of the benefits of opting for an insured mortgage.

Common mistake: many borrowers assume mortgage default insurance is optional. It is not. If your down payment is under 20%, an insured mortgage is the only option available to you.

What Is an Uninsured Mortgage?

An uninsured mortgage is a mortgage that is not backed by default insurance. This typically applies to borrowers who put down 20% or more of the purchase price, borrowers purchasing properties over $1.5 million, and borrowers who are refinancing their existing mortgage.

Unlike an insured mortgage, a regular conventional mortgage carries no premium. You are not paying for default coverage. However, because the mortgage lender is taking on the risk of the loan without any insurer backstop, lenders typically charge slightly higher rates on uninsured mortgages than on insured ones.

A conventional mortgage also allows for a longer amortization period. Borrowers may access amortizations up to 30 years or longer, depending on the lender, which reduces the monthly payment but increases total interest paid over time.

Who Gets an Uninsured Mortgage?

You will have an uninsured mortgage if any of the following apply:

- Your down payment is 20% or more

- Your purchase price exceeds $1.5 million (insurance is not available at this threshold, regardless of down payment)

- You are refinancing an existing mortgage

- You are purchasing a rental or investment property

- You are a borrower using a private lender or certain alternative financial institutions

Key takeaway: putting down 20% or more eliminates the insurance premium, but it does not automatically mean you get the lowest rate. Lenders still apply risk-based pricing to uninsured mortgages, and your credit profile, income, and property type all factor in.

Rates and Lender Risk on Uninsured Mortgages

Because an uninsured mortgage is not backed by CMHC, Sagen, or Canada Guaranty, the mortgage lender absorbs 100% of the default risk. Lenders account for this by applying a modest rate premium relative to insured mortgage pricing.

The rate difference between an insured mortgage and an uninsured mortgage from the same financial institution is typically 10 to 30 basis points, though this varies by lender and market conditions. That gap may seem small on paper, but on a $700,000 mortgage over a five-year term, it can represent several thousand dollars in additional interest.

The insured mortgage process can vary between lenders, but understanding what to expect can make it easier to navigate. Engaging with your lender about your insured mortgage options is essential.

Common myth: “Putting 20% down always gets you a better deal.” The elimination of the insurance premium is a real benefit, but borrowers with exactly 20% down sometimes pay enough in rate premium to partially offset the savings. A mortgage broker can run the numbers for your specific scenario.

What Is an Insurable Mortgage?

An insurable mortgage sits between the two categories above. It is a mortgage that the borrower does not pay to insure, but which the mortgage lender chooses to insure on the back end using what is called portfolio insurance or bulk insurance.

From the borrower’s perspective, an insurable mortgage looks like an uninsured mortgage. You put down 20% or more. You pay no mortgage default insurance premium. But behind the scenes, the lender purchases insurance on a pool of these mortgages through CMHC, Sagen, or Canada Guaranty. The cost is absorbed by the lender, not passed on to you directly.

Ultimately, whether you choose an insured mortgage or another type, being well-informed will guide your decisions. An insured mortgage can be a pivotal factor in your financial planning.

How Insurable Differs from Insured

The key distinction is who pays and when. With mortgage insurance, the borrower pays the premium at origination, and it is added to the loan. In an insurable mortgage, the borrower pays nothing for the insurance, and the lender takes care of it as a risk management tool on their end.

For a mortgage to be insurable, it must still meet certain criteria:

- The purchase price or property value must be under $1.5 million

- The amortization period must be 25 years or less

- The property must be owner-occupied

- The mortgage must be a purchase transaction, not a refinance

Important to note: refinances are never insurable. If you are refinancing your mortgage, you will always have an uninsured mortgage, regardless of how much equity you have in your home.

Why Lenders Use Portfolio Insurance

When a lender insures a pool of mortgages through CMHC, Sagen, or Canada Guaranty, they reduce the regulatory capital they are required to hold against those loans. That frees up capital to issue more mortgages at competitive rates.

This is why some financial institutions and monoline lenders can offer rates on insurable mortgages that are close to, or even match, insured mortgage rates. The lender’s cost of funding drops because the default risk is covered. That saving is sometimes passed through to the borrower in the form of a lower rate.

Key takeaway: if you are putting down exactly 20% on an owner-occupied property under $1.5 million with a 25-year amortization, you may qualify for an insurable mortgage without even knowing it. Your mortgage broker should be checking this on your behalf.

Your experience with an insured mortgage will set the tone for your future financial endeavours, highlighting the importance of this mortgage type in your financial strategy.

Insured vs. Uninsured vs. Insurable: Side-by-Side Comparison

| Feature | Insured Mortgage | Insurable Mortgage | Uninsured Mortgage |

|---|---|---|---|

| Down payment | Less than 20% | 20% or more | 20% or more |

| Max purchase price | Under $1.5M | Under $1.5M (*lender varies) | No limit |

| Borrower pays premium? | Yes | No | No |

| Max amortization | 25 years (30 for eligible FTBs) | 25 years | 30+ years (lender dependent) |

| Available on refinances? | No | No | Yes |

| Available on rentals? | No | No | Yes |

| Typical rate vs. insured | Lowest | Near-lowest | Slightly higher |

| Insurer involved | CMHC / Sagen / Canada Guaranty | CMHC / Sagen / Canada Guaranty | None |

How Your Mortgage Category Affects Your Rate

Your mortgage category is one of the most direct inputs into the rate a mortgage lender will offer you. Lenders in Canada price their mortgage books based on the cost of funding each loan. Insured and insurable mortgages are cheaper for lenders to fund because the default risk is backstopped by an insurer.

As a general pattern, default insured mortgages carry the lowest rates, insurable mortgages are close behind, and uninsured mortgages are priced slightly higher. This is true across most Schedule A banks, credit unions, and monoline lenders.

There is a practical implication here for borrowers on the fence about their down payment. If you are debating whether to put down 18% versus 20%, the rate difference between an insured mortgage and a conventional mortgage, combined with the elimination of the premium at 20%, should be calculated carefully rather than assumed. A qualified mortgage broker can model both scenarios and show you the true cost over your term.

Common Myths About Mortgage Insurance in Canada

Myth 1: Mortgage insurance protects me if I lose my job. It does not. Mortgage default insurance (provided by CMHC, Sagen, or Canada Guaranty) protects the mortgage lender, not the borrower. Separate mortgage life or disability insurance products exist to protect borrowers, but they are a different product entirely.

Myth 2: Only small down payments require mortgage insurance. Insurable mortgages show that lenders can insure mortgages even when the borrower puts down 20% or more. The borrower just does not pay for it or see it happening.

Myth 3: Getting a conventional mortgage means you are a stronger borrower. Not necessarily. An uninsured mortgage simply means your loan does not meet the criteria for insurance, or that you chose a larger down payment. It is a category, not a credit judgment.

Myth 4: All mortgage lenders offer all three categories. Not true. Some lenders specialize in insured mortgage products and do not hold uninsured mortgages on their books. Others focus exclusively on the conventional market. A mortgage broker has access to the full range of lenders and can match your situation to the right product.

How a Mortgage Broker Can Help You Navigate All Three Categories

Most borrowers do not know which mortgage category they fall into until they speak with someone who understands how lenders price and categorize loans. This is where working with a mortgage broker becomes genuinely valuable.

A mortgage broker does not work for a single financial institution. They have access to dozens of mortgage lenders, including banks, credit unions, monoline lenders, and private lenders. When you apply, a good broker will identify whether your mortgage is insured, insurable, or uninsured, and will shop your file accordingly to find the lender offering the best rate and terms in that specific category.

At LendToday.ca, we work with borrowers across Ontario who are navigating all three mortgage categories, including those dealing with power of sale, equity-based lending, and situations where traditional lenders have said no. If you are not sure which category you fall into, that is exactly the kind of question we are here to answer.

Frequently Asked Questions

Q: What is the difference between an insured mortgage and mortgage life insurance?

A: An insured mortgage refers to mortgage default insurance, which is provided by CMHC, Sagen, or Canada Guaranty. It protects the mortgage lender if the borrower stops making payments. Mortgage life insurance is a separate product that pays off your mortgage balance if you pass away. The two are completely different and should not be confused.

Q: Can I switch from an uninsured mortgage to an insured mortgage?

A: No. Once your mortgage is categorized as uninsured, it cannot become an insured mortgage. However, if you are purchasing a new property and your down payment will be under 20%, your new mortgage will be insured. Each mortgage is categorized at origination based on the specific transaction details.

Q: Do all three insurers (CMHC, Sagen, Canada Guaranty) offer the same rates and premiums?

A: The premium rates charged to borrowers are standardized across all three insurers and are set based on loan-to-value ratios. The difference between CMHC, Sagen, and Canada Guaranty lies more in their underwriting guidelines and the types of properties or borrowers they will consider. Your mortgage lender or mortgage broker typically selects which insurer to use based on your specific file.

Q: I am putting down exactly 20%. Am I automatically getting an insurable mortgage?

A: Not automatically, but you may be. For your mortgage to be insurable, it must meet specific criteria: purchase price under $1.5 million, owner-occupied property, amortization of 25 years or less, and a purchase transaction (not a refinance). If your file meets those criteria, your mortgage lender may choose to insure it on the back end. Ask your mortgage broker to confirm.

Q: Does an insurable mortgage mean I pay a hidden premium?

A: No. With an insurable mortgage, the mortgage lender pays the premium to CMHC, Sagen, or Canada Guaranty. That cost is not directly passed to you in a line-item charge. You benefit from the lower rate that lenders can offer when their funding costs are reduced, without paying the premium yourself.

Q: Can I get an insured mortgage on a rental property?

A: No. Mortgage default insurance through CMHC, Sagen, or Canada Guaranty is only available on owner-occupied properties. Rental and investment properties do not qualify, meaning any mortgage on a rental property will be a conventional mortgage (uninsured) by definition.

Conclusion

Whether you end up with an insured mortgage, an uninsured mortgage, or an insurable mortgage, the category you fall into will shape your rate, your lender options, and your total cost of borrowing. These are not arbitrary labels; they are the framework that Canadian mortgage lenders and regulators use to price and manage risk across the entire housing market.

As you consider your options, remember that mortgage insurance can significantly affect your financial outcomes and overall satisfaction with your home purchase.

Understanding your category before you apply puts you in a much stronger position at the negotiating table. And working with a knowledgeable mortgage broker ensures that your file is matched to the lender and product that actually fits your situation.

In conclusion, pursuing mortgage insurance can provide stability, opportunities for growth and entry into the housing market.

Ready to find out which category you fall into? Contact LendToday.ca today.

Phone: 1-855-242-7732