Emergency funds for home expenses are not a nice-to-have for Canadian homeowners. They are the difference between a manageable setback and a financial crisis. Without emergency savings, a single furnace failure, job loss, or stretch of reduced income can trigger missed bills, NSFs, collections, mortgage arrears, and, in the worst cases, power of sale. This guide covers how much to save, what qualifies as a real emergency, and what Ontario homeowners can do when emergency savings have already run out.

Why Most Canadian Homeowners Are One Emergency Away From Financial Trouble

Most Canadian homeowners believe their finances are stable until they are not. The mortgage is current, the bills are getting paid, and things feel manageable. What does not get factored in is the gap between “getting by” and “financially resilient.”

Emergency savings are what fill that gap. Without them, the moment something goes wrong, whether that is a job loss, a major repair, or a period of reduced income, the entire household budget is at risk. According to the Financial Consumer Agency of Canada, nearly half of Canadians would struggle to cover an unexpected $2,000 expense without borrowing. For homeowners, unexpected expenses regularly exceed that amount before the repair crew even leaves the driveway.

The problem is not always overspending. It is underprepared. Emergency funds for home expenses are rarely discussed when people are signing mortgage documents, and by the time they become necessary, it is often too late to build them from scratch.

The Real Cost of Not Being Prepared

When emergency savings are not in place, a small financial shock quickly becomes a large one. Here is how the sequence typically unfolds.

A homeowner experiences a job loss or reduced income. They begin prioritizing which bills to pay and which to defer. NSFs start appearing on the account, each one costing $45 or more at major Canadian banks. Credit card balances grow. Some bills go to collections. A collections entry on a credit report stays for six years and significantly damages the credit score. At some point, the mortgage payment gets missed. Once that happens, the lender takes notice, and if arrears accumulate, power of sale proceedings in Ontario can begin. At that stage, options narrow quickly and costs compound.

Key takeaway: the damage is not caused by one bad decision. It is caused by a chain reaction that starts the moment emergency savings run out.

What Counts as a Home Emergency Expense?

Not every home expense is an emergency, but many homeowners only find this out when they are trying to decide which bill to pay first. Understanding the difference between true emergency expenses and planned maintenance costs is essential to building emergency funds for home expenses that actually work.

A genuine home emergency is unexpected, unavoidable, and requires immediate attention. A furnace that fails in January. A burst pipe that floods the basement. A water heater that stops working with no warning. These are not situations where you can delay action or shop around for weeks. They require money right away, and they do not care whether your savings account is ready.

Planned maintenance, on the other hand, is predictable. Roofs age. Driveways crack. Eavestroughs need cleaning every year. These are legitimate home expenses, but they are not emergencies. They belong in a separate maintenance budget, not your emergency savings.

| Expense Type | Emergency | Planned / Predictable |

|---|---|---|

| Furnace failure | Yes | No |

| Roof replacement (aging) | Sometimes | Yes |

| Burst pipe | Yes | No |

| Annual property taxes | No | Yes |

| HVAC breakdown | Yes | No |

| Driveway sealing | No | Yes |

| Water heater failure | Yes | No |

| Condo special assessment | Sometimes | Often predictable |

| Electrical panel failure | Yes | No |

| Seasonal maintenance | No | Yes |

Important to note: home insurance does not always cover these situations. Deductibles commonly range from $1,000 to $5,000, and many mechanical failures are excluded from standard policies entirely. Do not assume coverage exists until you have verified it with your broker.

The Expenses Homeowners Always Forget to Plan For

Beyond major repairs, there is a category of recurring home expenses that consistently catch homeowners off guard. Property tax installments come due on a schedule that does not align with most household budgets. Condo fees can increase without much notice, and special assessments for building repairs can arrive as large lump-sum bills. Utility costs spike significantly in Canadian winters and summers. These are not emergencies in the traditional sense, but they become emergency expenses when there is no budget allocated for them.

Emergency funds for home expenses need to account for this grey zone. A true financial buffer covers both the unpredictable furnace and the property tax bill that arrived at the worst possible time.

How Much Should You Have in Emergency Savings as a Homeowner?

The standard advice is three to six months of living expenses in emergency savings. For renters, that calculation is relatively straightforward. For homeowners, it is more complicated.

On top of general living expenses, Canadian homeowners should set aside between 1% and 3% of their home’s value annually for maintenance and unexpected repairs. With the average Ontario home priced well above $700,000 in many markets, that means keeping between $7,000 and $21,000 specifically earmarked for home expenses each year. That number sounds large because it is, and it reflects the real financial responsibility that comes with owning property in Canada.

A practical starting point is a $5,000 dedicated emergency fund for home expenses, separate from your general emergency savings. From there, build toward a target of three months of all household bills plus $10,000 for home-specific emergencies. It will not happen overnight, but having a target matters.

Common mistake: keeping emergency savings in the same account as everyday spending. Money that is easy to access for daily purchases will not be there when a genuine emergency arrives. A dedicated high-interest savings account or TFSA creates both a barrier and a tax advantage.

Building Emergency Savings on a Tight Budget

Reduced income, high bills, and a tight monthly budget make saving feel impossible. It is not, but it requires a different approach.

Automating small weekly contributions, even $50 to $100, removes the decision from the equation. Redirecting annual tax refunds directly into emergency savings rather than spending them can build the fund faster than any other single habit. During higher-income months, increasing contributions even temporarily creates a buffer that carries through slower periods.

Self-employed Canadians and seasonal workers need to be especially deliberate. Income volatility is already built into the financial picture, which means the emergency savings target needs to be higher, not lower. A contractor who earns well in summer and slowly in winter needs emergency funds for home expenses that can cover the lean months without disrupting the mortgage.

When Emergency Savings Run Out: What Happens Next?

This is the part most articles skip. Emergency savings run out. It happens to careful homeowners, responsible budgeters, and people who did everything right until a job loss or health issue changed the math entirely. The question is not whether it can happen. It is what comes next when it does.

The sequence that follows depleted emergency savings is predictable. Bills get prioritized. Some get missed. NSFs appear. Collections calls begin. The mortgage becomes harder to cover. Arrears accumulate. Lenders send demand letters. In Ontario, power of sale proceedings can follow if arrears are not resolved.

Important to note: lenders are not legally required to offer payment deferrals or hardship accommodations. Some will work with borrowers proactively. Others will not. Waiting and hoping is not a strategy when mortgage arrears are involved.

Judgments are another outcome that homeowners do not always anticipate. When unsecured creditors pursue unpaid balances through the courts, the resulting judgment can be registered against your property as a lien. That lien affects your ability to refinance, sell, or access equity until it is resolved.

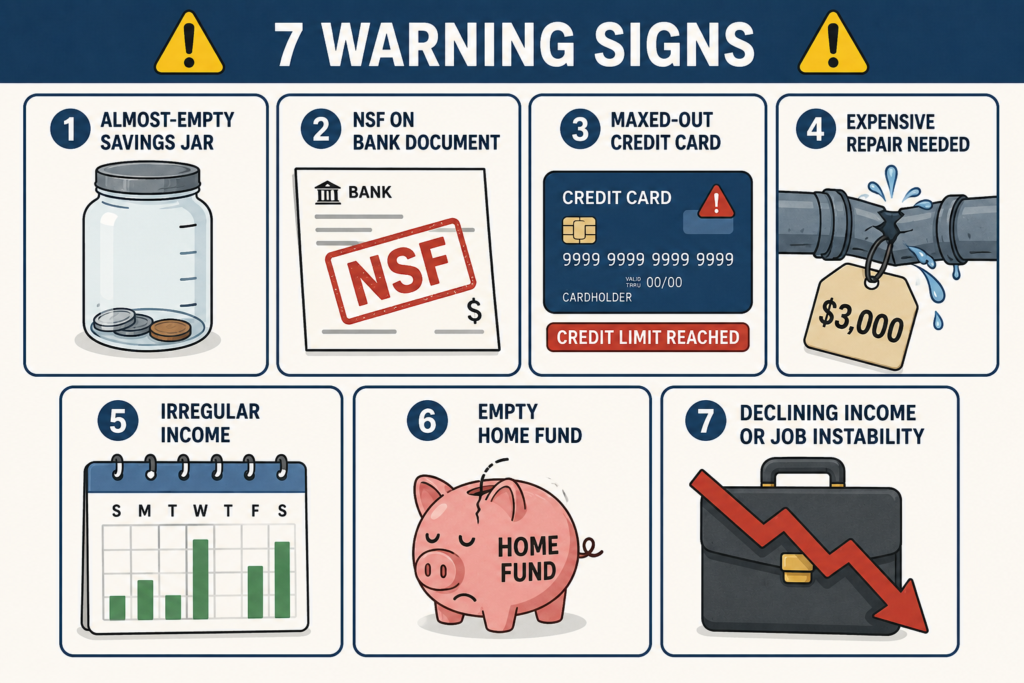

The Warning Signs You Cannot Ignore

Some warning signs appear well before a full financial crisis develops. Recognizing them early creates more options.

- You have less than one month of household expenses saved

- You have had at least one NSF in the past 90 days

- You are carrying a growing credit card balance to cover monthly bills

- You could not cover a $3,000 home repair without borrowing

- Your income is variable, seasonal, or commission-based

- You have no savings designated specifically for emergency home expenses

- You have experienced a recent job loss or reduction in income

If two or more of these apply, building or rebuilding emergency funds for home expenses needs to become an immediate financial priority, not a future goal.

How Home Equity Can Replace Emergency Savings You No Longer Have

For Ontario homeowners who have built equity in their property, that equity becomes the most accessible financial resource when emergency savings are gone. It is not a substitute for having savings in the first place, but it is a meaningful option when options are limited.

A home equity loan or second mortgage allows homeowners to borrow against the value built up in their property. Unlike traditional bank loans, private and equity-based lenders evaluate applications primarily on the equity available in the home, not solely on credit scores, employment status, or income documentation. That distinction matters enormously for homeowners dealing with collections, NSFs, reduced income, or recent job loss.

A home equity loan used strategically can clear mortgage arrears, pay off collections accounts, eliminate NSF cycles by consolidating outstanding bills into a single manageable payment, and stop power of sale proceedings before they advance further. This is not a solution that fixes the underlying savings gap, but it can stop the immediate damage and restore enough financial stability to begin rebuilding.

Common myth: if you have bad credit or collections on file, no lender will help you. This is not true for homeowners with equity. Private lenders operating in Ontario assess risk differently than chartered banks. The equity in your home carries significant weight in that evaluation.

Important to note: using home equity to resolve a financial crisis is a serious decision. The goal is stabilization, not a new cycle of borrowing. Anyone pursuing this option should understand the terms clearly and have a plan for rebuilding emergency savings once cash flow is restored.

What LendToday Can Do When the Banks Cannot Help

LendToday specializes in equity-based lending for Ontario homeowners in exactly these situations. If you are facing mortgage arrears, power of sale, active collections, judgments on title, or a period of job loss or reduced income that has put your household finances under pressure, there may be more options available than you realize.

A second mortgage Ontario can bring mortgage arrears current and stop power of sale proceedings. Debt consolidation using home equity can roll multiple bills, NSFs, and collections balances into a single payment with manageable terms. Approvals are based on the equity in your home, and timelines are designed for situations where urgency is real.

If you have already tried the bank and been declined, equity-based lending through a private lender may be the step that changes the outcome. You can stop power of sale in Ontario if you act before the process goes too far.

Rebuilding Emergency Savings After a Financial Crisis

Surviving a financial crisis, whether through equity lending, debt consolidation, or simply grinding through a difficult stretch, is not the finish line. It is the starting point for building the emergency savings that prevent the same situation from recurring.

The first step is stabilizing cash flow. If a consolidation loan has cleared the collections and brought the mortgage current, the monthly payment burden should be lower than it was before. That difference needs to go directly into emergency savings, not back into spending.

A dedicated account, separate from everyday banking, is essential. Automate a fixed contribution every pay period. Even $75 per week adds up to nearly $4,000 in a year. The goal during the rebuilding phase is consistency, not speed. Slow and steady accumulation of emergency funds for home expenses creates a buffer that holds through the next unexpected event.

Key takeaway: a debt consolidation loan is a tool for stability, not a permanent solution. Emergency savings are what make stability permanent.

Tools and Habits That Help Canadian Homeowners Stay Ahead

Building long-term resilience as a homeowner is less about any single product or decision and more about consistent habits applied over time.

A monthly home expense audit takes 20 minutes and shows exactly where the budget stands relative to upcoming bills, seasonal expenses, and savings targets. A seasonal maintenance calendar with estimated costs attached removes the surprise element from planned expenses. An annual insurance policy review ensures coverage levels still match the property’s current value and that deductible amounts are factored into the emergency savings target.

For homeowners recovering from a financial setback, tracking emergency savings progress visibly, whether in a spreadsheet or a budgeting app, reinforces the habit and makes the growing balance feel real.

Frequently Asked Questions About Emergency Funds for Home Expenses

Q: How much should I have in emergency funds for home expenses in Canada? A: Most financial advisors recommend three to six months of all household expenses, plus a separate home maintenance reserve equal to 1% to 3% of your home’s value annually. For a home worth $700,000, that means keeping between $7,000 and $21,000 set aside specifically for home-related emergency expenses.

Start with a $5,000 target dedicated to home expenses and build from there alongside your general emergency savings. Having even a partial emergency fund in place dramatically reduces the risk of a single event triggering mortgage arrears or collections.

Q: What happens if I miss a mortgage payment because of a job loss? A: A single missed payment will typically trigger a notice from your lender. If the situation is not resolved, it can escalate to mortgage arrears and potentially power of sale proceedings in Ontario.

Lenders are not legally required to offer deferrals, so acting early and speaking with a mortgage broker is critical. The sooner you explore options, including equity-based solutions, the more choices you will have and the lower the cost of resolving the situation.

Q: Can NSFs and collections stop me from getting a loan? A: NSFs and collections entries damage your credit score and make traditional bank lending difficult. However, private and equity-based lenders like LendToday assess applications primarily on the equity in your home, not just your credit history.

Homeowners with significant equity may still qualify for a second mortgage or home equity loan even with active collections or judgments on file. The earlier you act, the more equity you typically have available to work with.

Q: Is a HELOC a good substitute for emergency savings? A: A HELOC can provide access to funds in an emergency, but it carries risks that a dedicated savings account does not. Lenders can reduce or freeze a HELOC at any time, particularly if your income drops or property values decline.

Emergency savings held in a TFSA or high-interest savings account are always more reliable as a first line of defence. A HELOC can serve as a secondary backup, but it should never be your only emergency plan.

Q: What is power of sale in Ontario, and how can I avoid it? A: Power of sale is a legal process that allows a mortgage lender in Ontario to sell your home to recover unpaid mortgage debt. It can begin within a relatively short window after missed payments, and it becomes significantly harder to stop once proceedings advance.

If you have equity in your home, a private lender may be able to help you pay off the arrears and bring your mortgage current before the process goes too far. Acting at the first sign of arrears gives you the best chance of preserving your home and your equity.

Q: Can I use a home equity loan to rebuild emergency savings? A: A home equity loan is best used to resolve immediate financial emergencies, such as stopping power of sale, paying off collections, or clearing mortgage arrears, rather than to directly fund a savings account.

Once your cash flow is stabilized through equity-based debt consolidation, you are in a much better position to rebuild emergency savings from income going forward. Using borrowed funds to create a savings account adds cost without addressing the root issue.

The Bottom Line on Emergency Funds for Home Expenses

Emergency funds for home expenses are not optional for Canadian homeowners in 2026. The cost of living is high, unexpected repairs are expensive, and the financial gap between stable and distressed is narrower than most people realize.

Job loss and reduced income remain the most common triggers for mortgage arrears, NSFs, and collections. A dedicated emergency savings account, sized appropriately for both general expenses and home-specific emergencies, is the single most effective protection against that outcome.

If emergency savings are already gone and you are facing arrears, collections, or the early stages of power of sale, home equity may be the tool that stops the damage and creates the space to recover. But the goal, always, is to build and maintain emergency funds for home expenses before you ever need to test what happens without them.

✅ Key Takeaway

In 2026, the cost of living is still elevated; having a financial plan isn’t optional — it’s essential.

Using your home equity for debt consolidation can lower your monthly payments, cut high-interest debt,

and give you the breathing room you need to stay ahead.